Weekly Gaming Reports Recap: April 29 - May 3 (2024)

Weekly Gaming Reports Recap: April 29 - May 3 (2024)

March 2023 US market results by Circana; Casual mobile games report by Litfoff; Q1'24 Investment market overview by InvestGame.

Reports of the week:

InvestGame: Gaming Investment Market in Q1’24

SJN Insights: Analysis of the UK Gaming Market in 2023

Game Sales Round-up (17.04.24 - 30.04.24)

Omdia: 19.3 million handhelds were sold in 2023

AppMagic: Top Mobile Games by Revenue and Downloads in April 2024

Circana: The US gaming market in March 2024 grew by 4%

Liftoff & GameRefinery: Casual Games in 2024

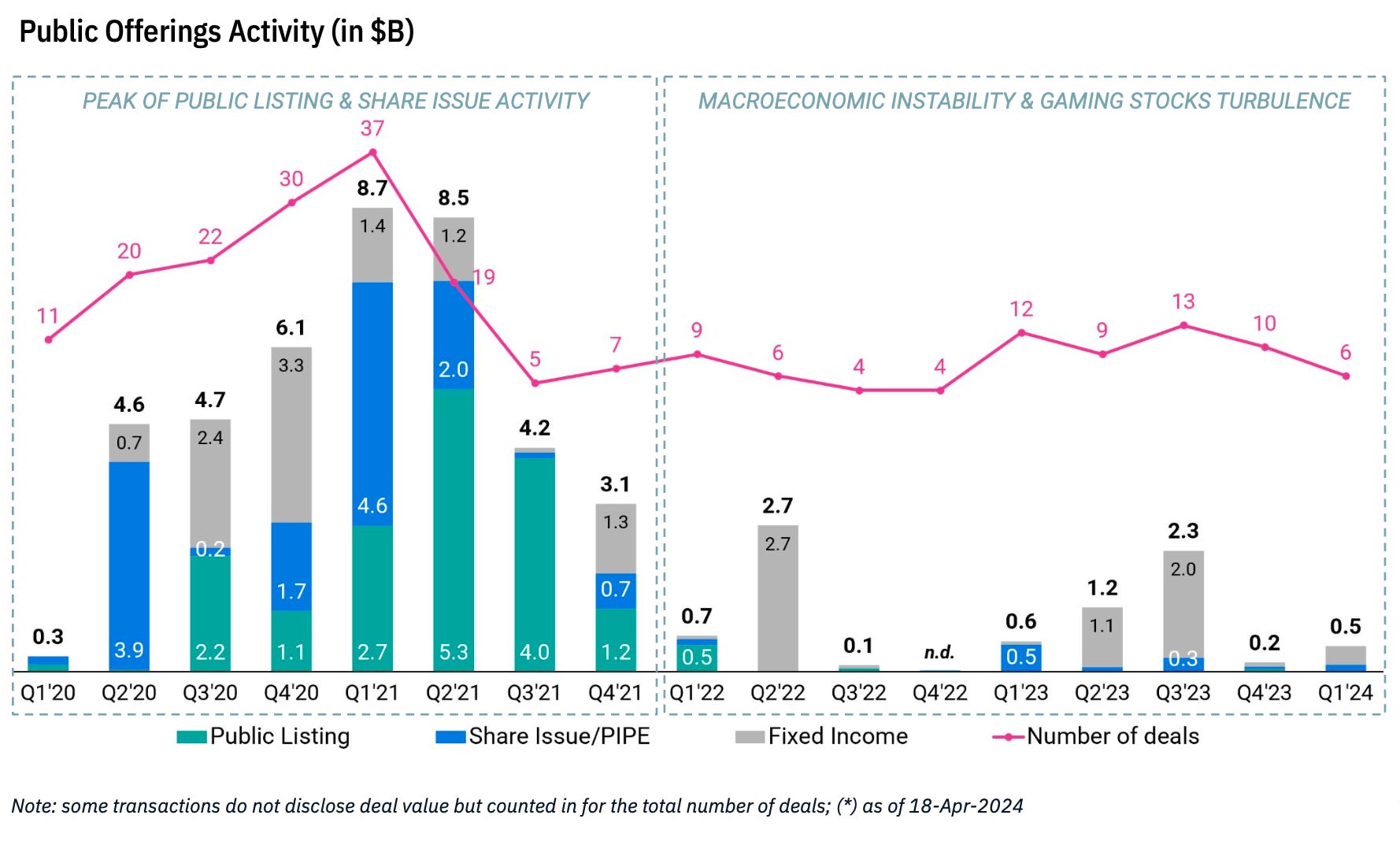

InvestGame: Gaming Investment Market in Q1’24

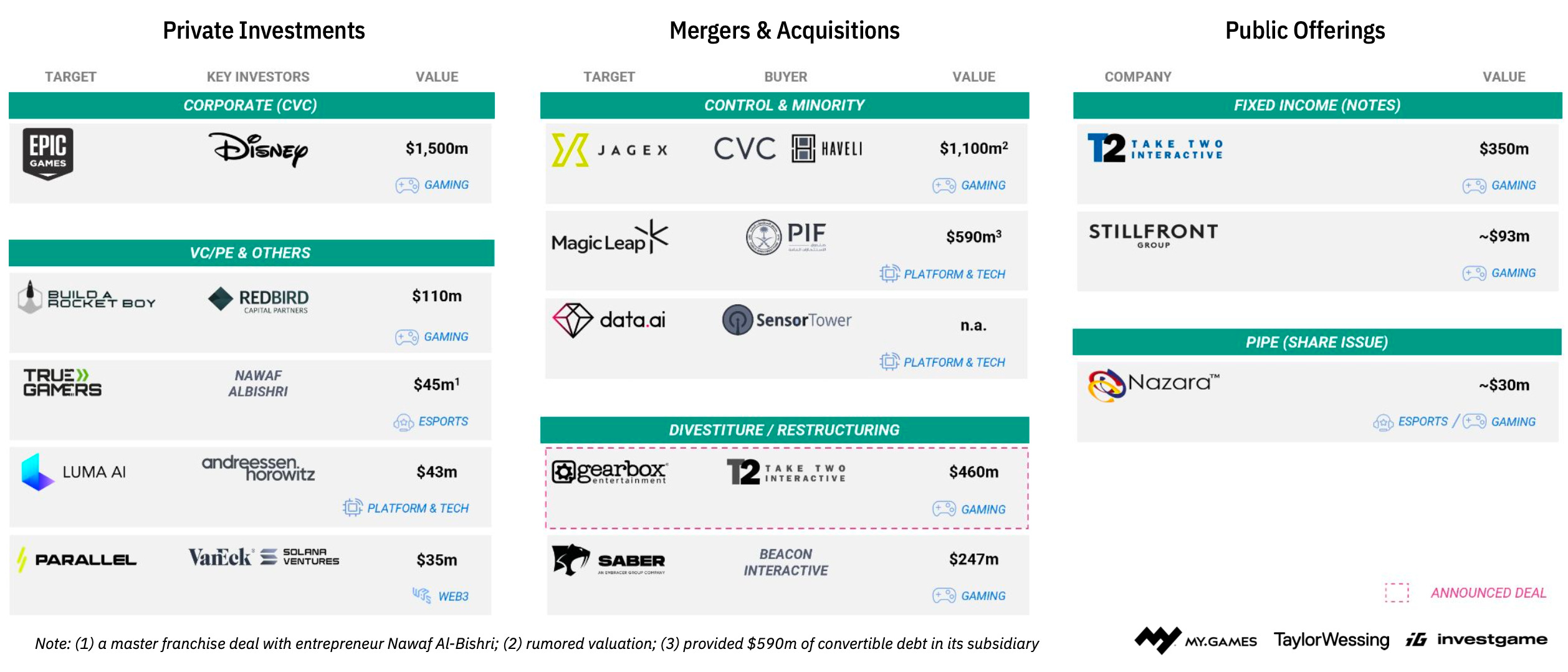

Private Investments

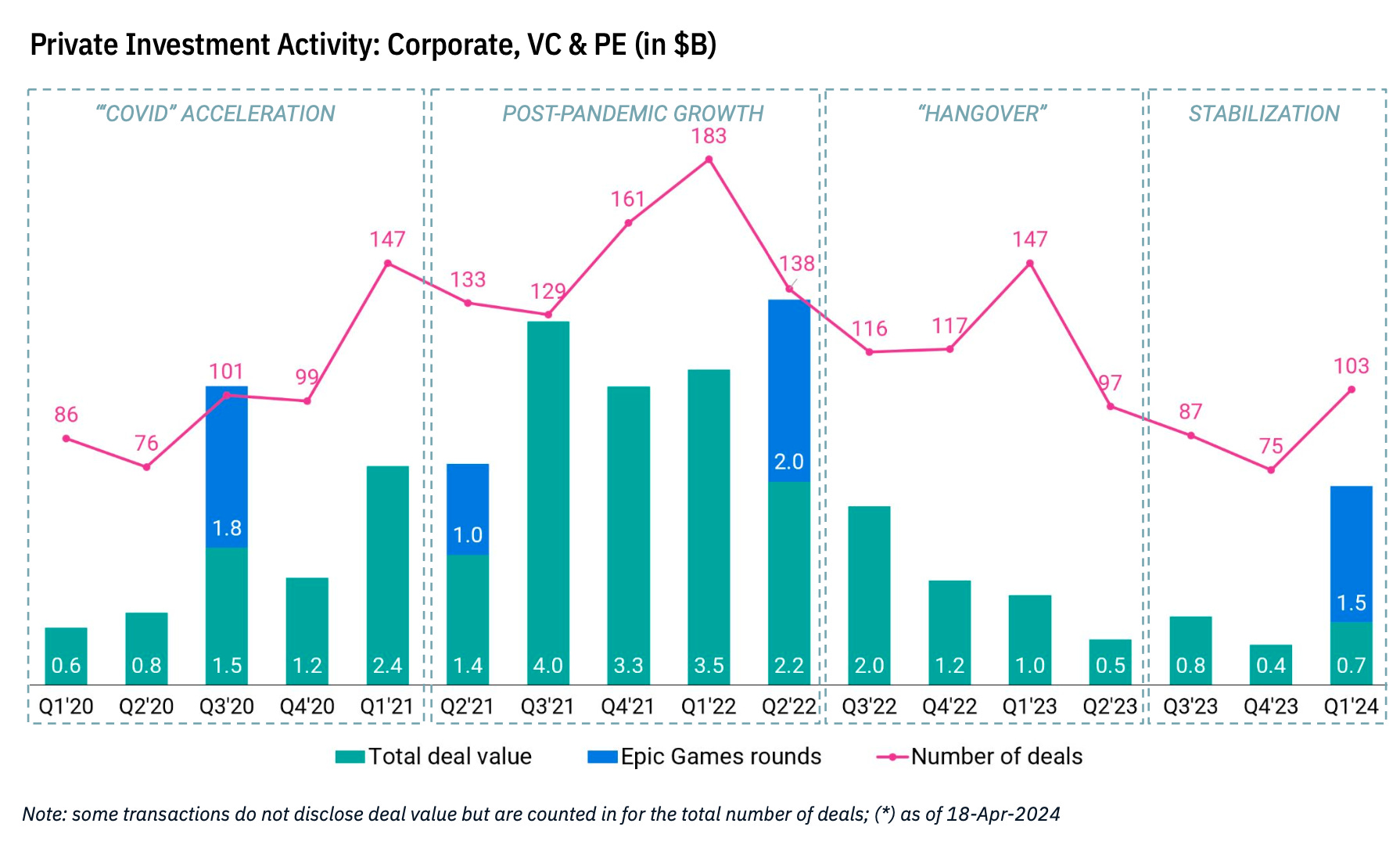

Private investment volume in Q1’24 reached its peak since Q3’22 - $2.2 billion. However, it's important to note that $1.5 billion is attributed to the deal between Disney and Epic Games.

In the first quarter of 2024, 103 deals were made. This is fewer than in the first quarter of 2023 (147 deals) but more than in the past 3 quarters.

InvestGame vividly illustrates the market's development stages on a graph - showing how investment activity has changed at different stages.

The InvestGame team expresses cautious optimism about the market situation and notes the growth of pre-Seed and Seed deals. However, the market situation remains far from optimal.

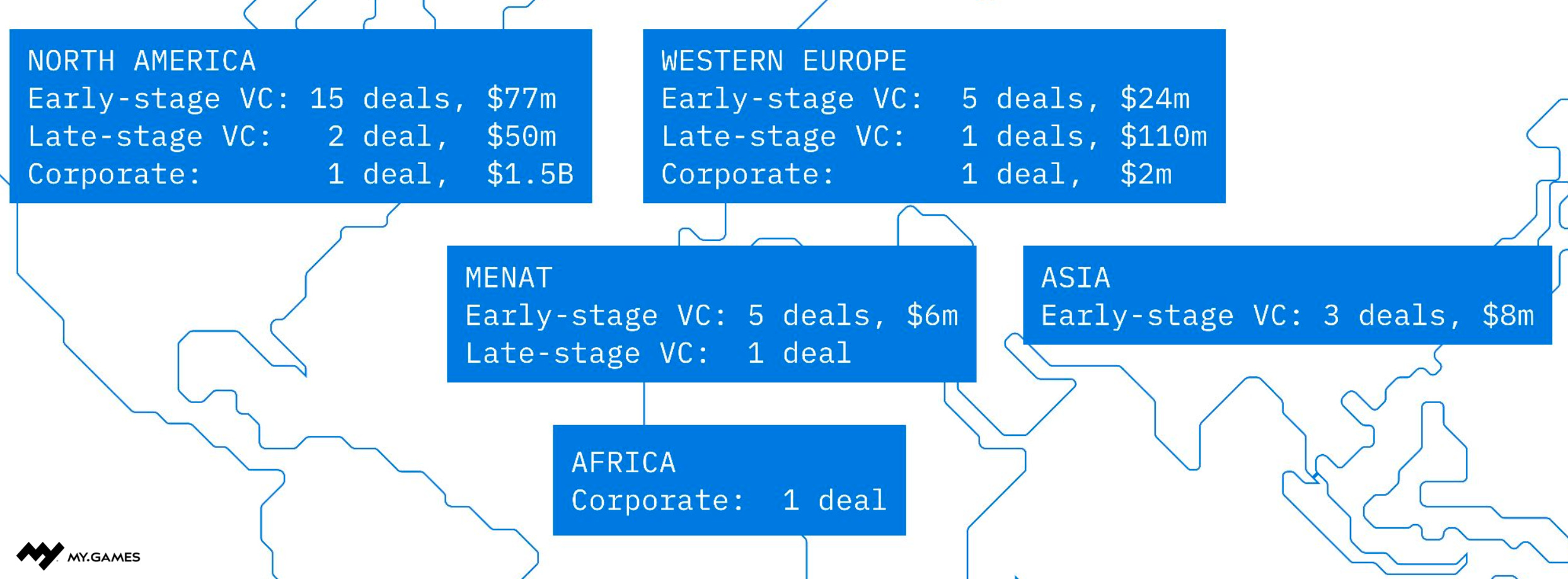

Private Investments - Gaming Companies (Developers or Publishers)

If we consider only investments in gaming companies at stages prior to Series A, then in Q1’24, 28 deals were made totaling $115 million.

The situation with VC deals in later rounds is less positive. In Q1’24, 4 deals were closed totaling $160 million. Three of them were less than $100 million; one was larger.

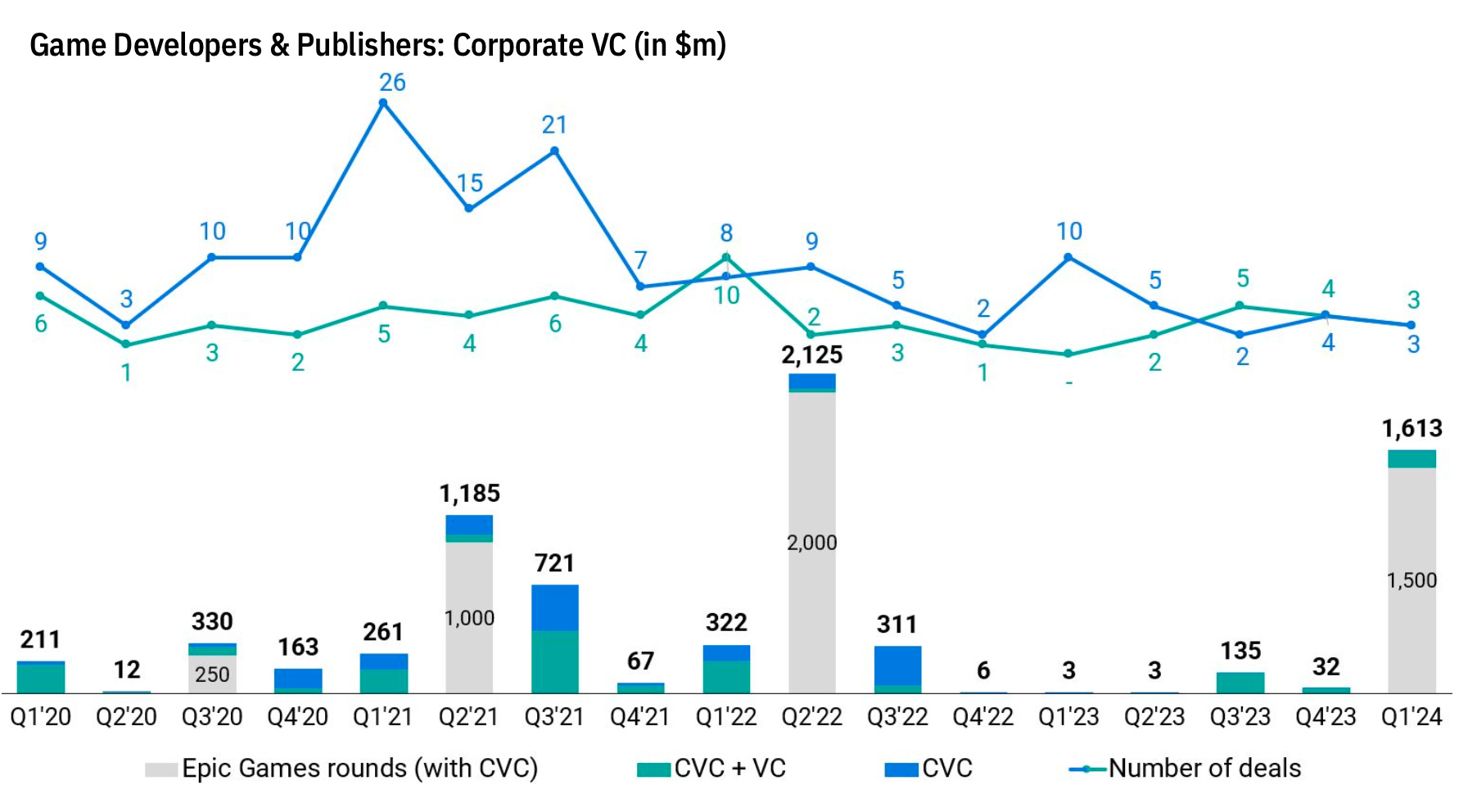

Corporate investors in Q1’24 made 6 deals totaling $1.613 billion (including the Disney deal with Epic Games). The InvestGame team notes that corporate funds are increasingly behaving like VC funds, investing at early stages. Tencent, NetEase, Krafton, Kakao, Sony are particularly active (25 such deals since 2022).

Since 2019, over 45 funds have emerged in the market. Twice as many as in the previous 10 years. They have attracted over $15 billion but have only reinvested $7 billion so far. Despite the challenging market situation, 10 funds were announced in Q1’24. Over 80% of all funds focus on early-stage investments.

1Up Ventures; BITKRAFT Ventures; Transcend Fund; The Games Fund; Ludus Ventures - the most active players in Seed stages in Q1’24.

The primary markets for investments remain the USA and Western Europe.

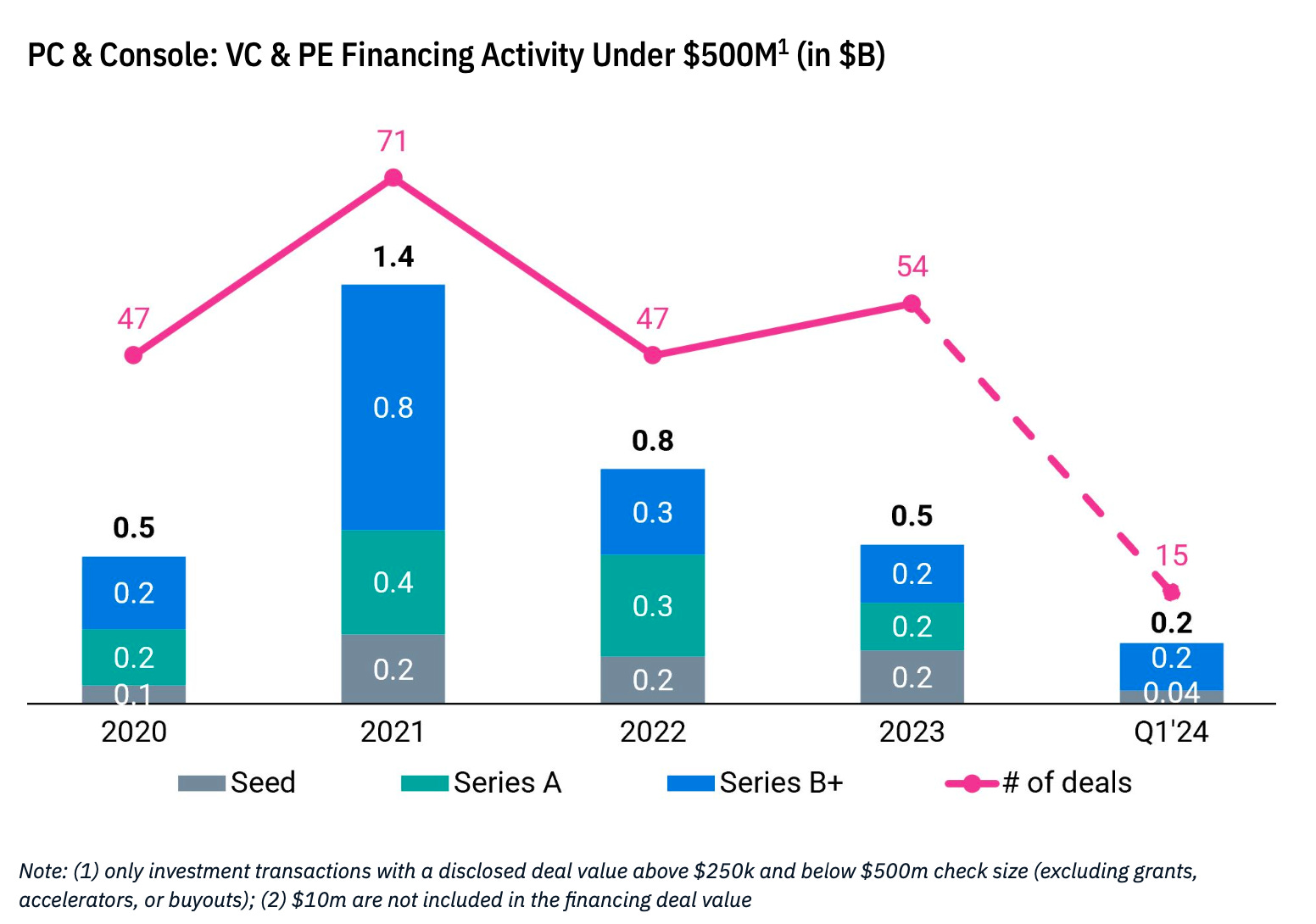

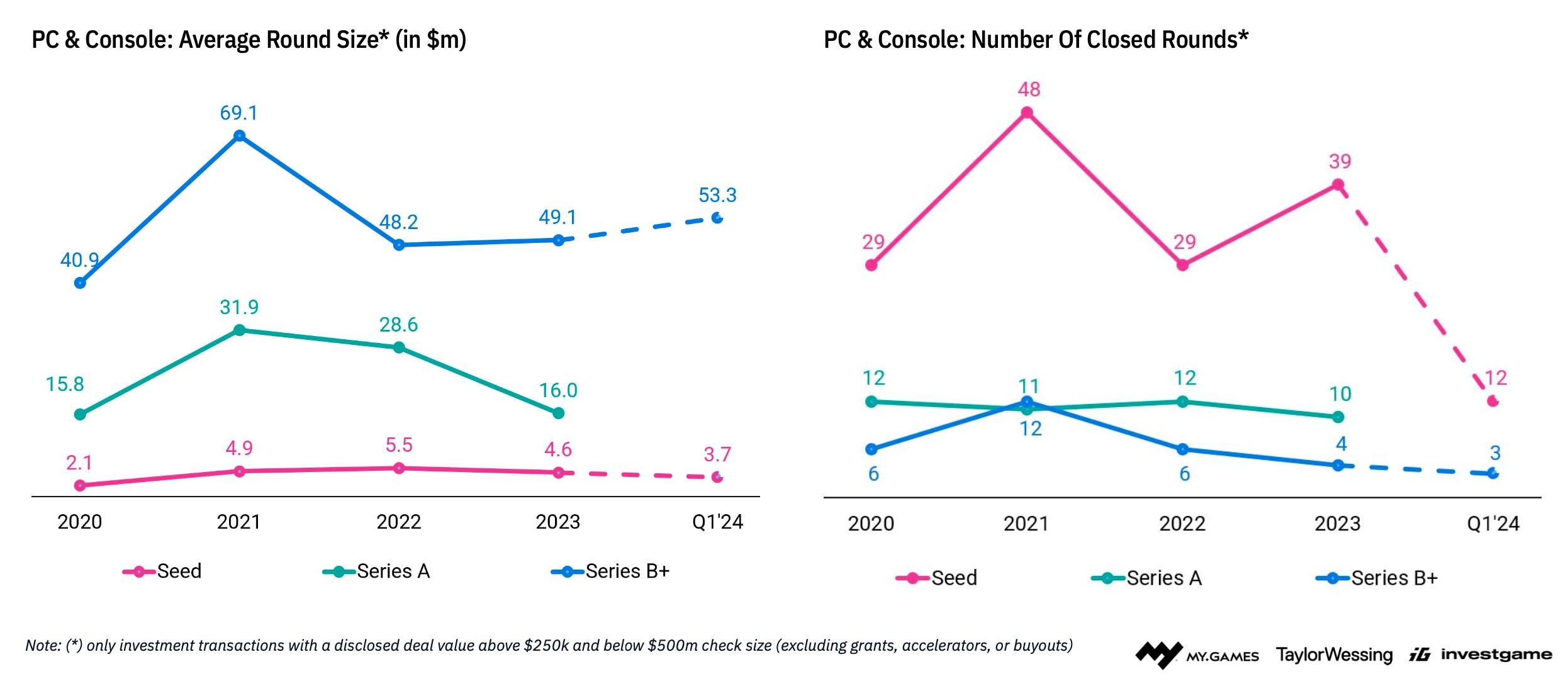

Private Investments - PC/Console Market

Since 2020, VC funds and PE firms have invested over $3.4 billion in PC/console companies. 50% of this amount was in Series B+ rounds. The majority of deals, both in terms of quantity and volume, occurred in 2021.

The number and volume of Seed rounds for PC/console developers have remained almost unchanged over the years, while Series A+ rounds have decreased both in volume and quantity.

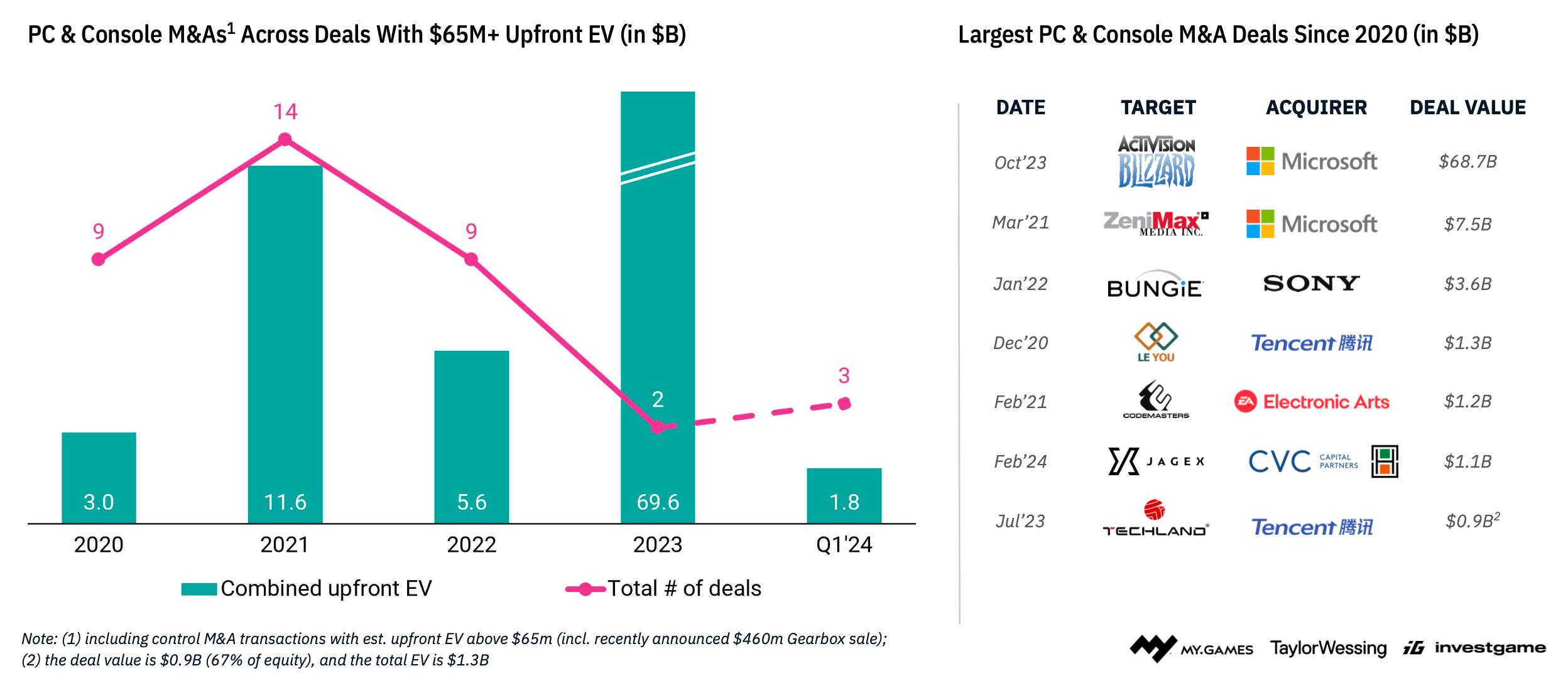

Meanwhile, there have been 37 deals totaling $91 billion for PC/console developers since 2020.

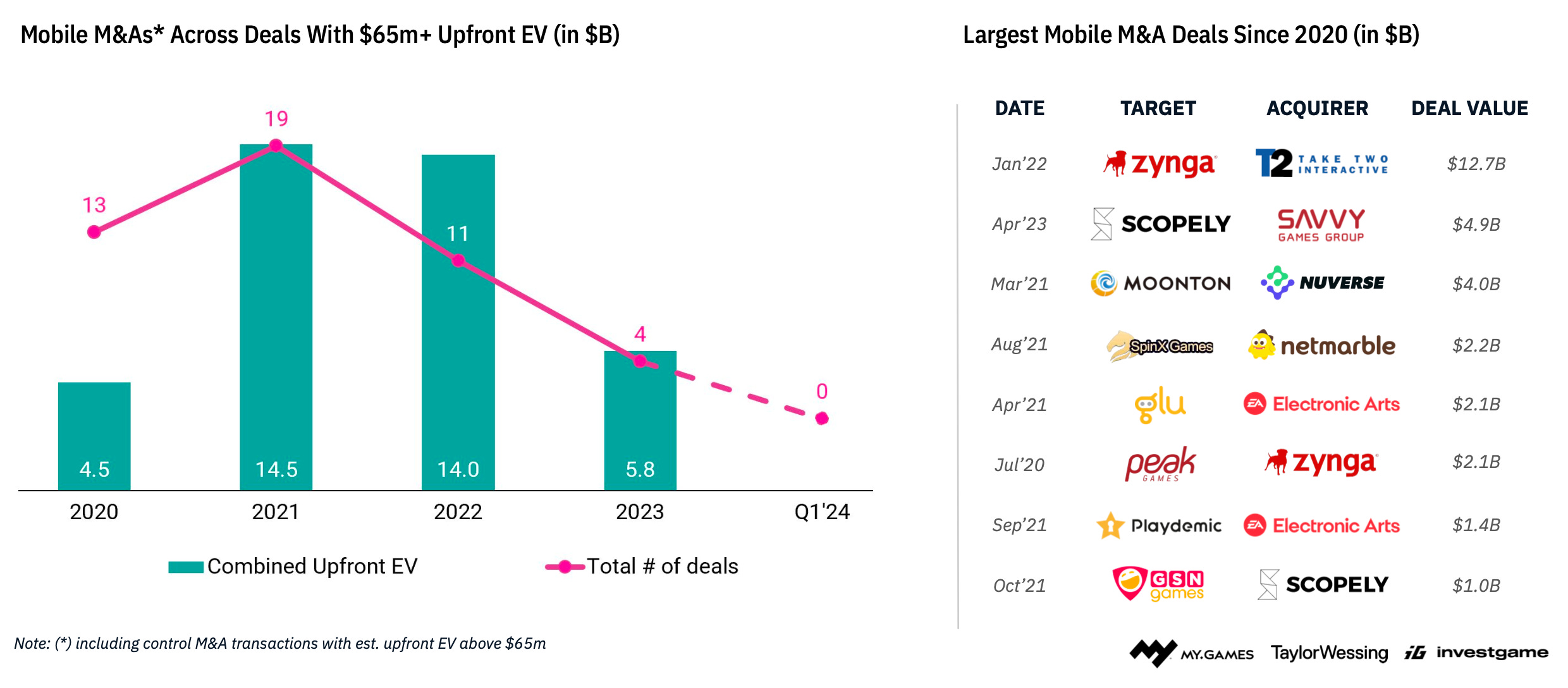

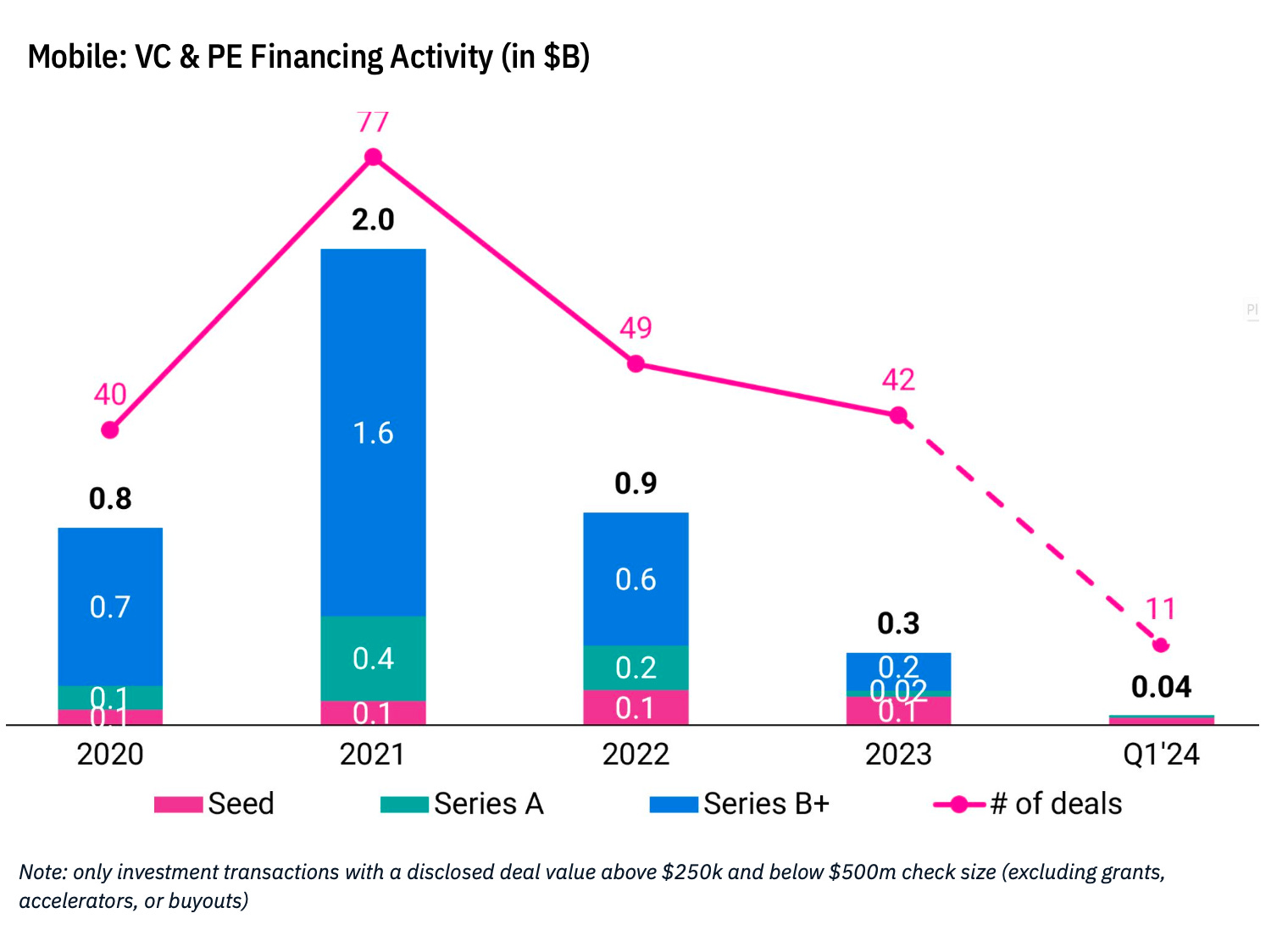

Private Investments - Mobile Market

The number of M&A deals with mobile developers has been decreasing since 2021 in terms of both volume and quantity of deals.

The popularity of mobile studios among VC and PE investors is also declining. In 2023, such studios attracted $0.3 billion in 42 deals.

The decline is most noticeable in later stages. The number and volume of Seed rounds are more stable.

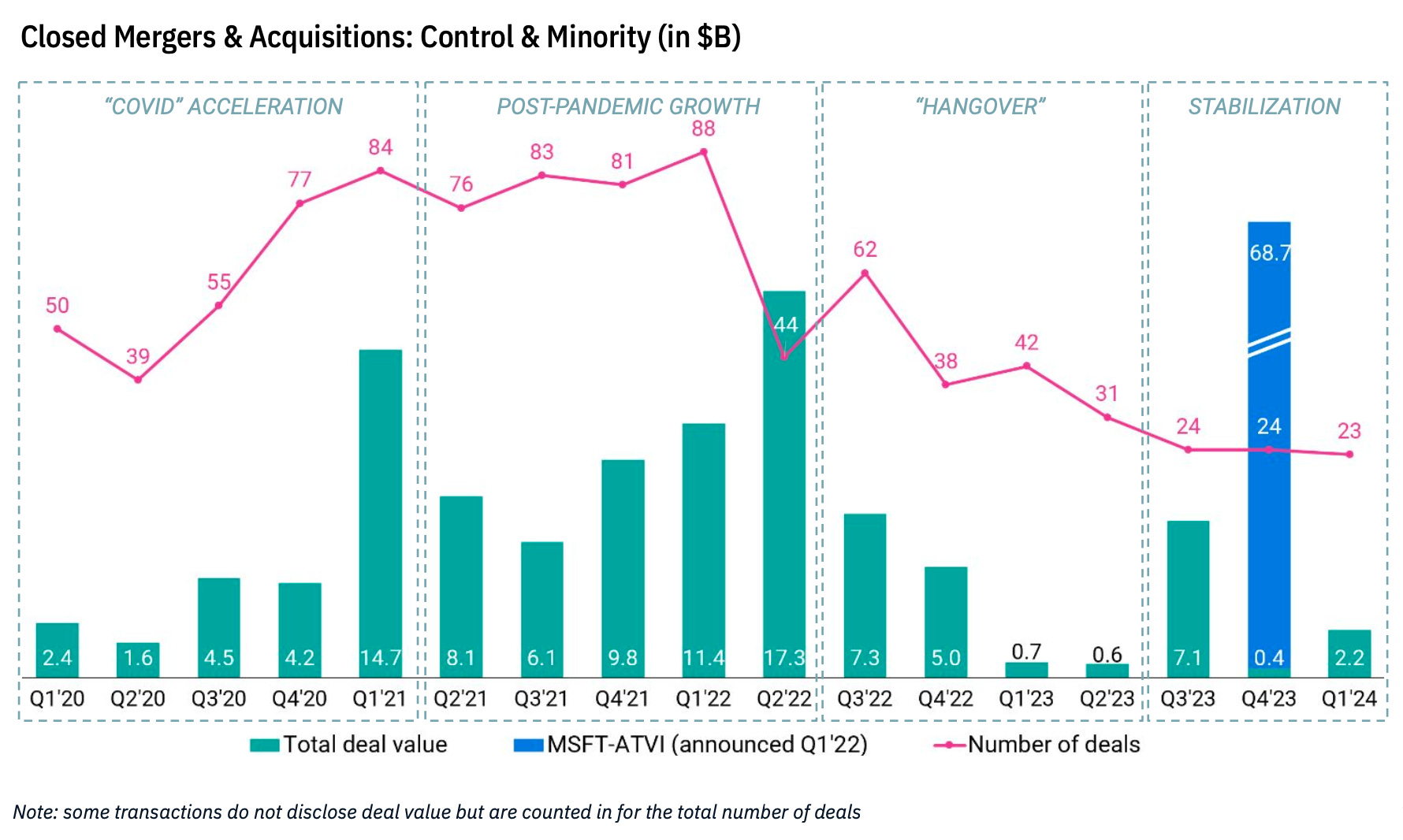

M&A

In Q1’24, 23 M&A deals totaling $2.2 billion were completed.

The most notable deal of the quarter was the acquisition of Jagex for $1.1 billion.

IPO

The situation with going public remains complex. High interest rates and poor performance of companies already on the market are putting pressure.

The largest upcoming IPO might be Shift Up. It is reported that they have already applied to the Korea Stock Exchange with a valuation of $2 billion.

Many public gaming companies are currently trading at a discount, so they are conducting buyback campaigns.

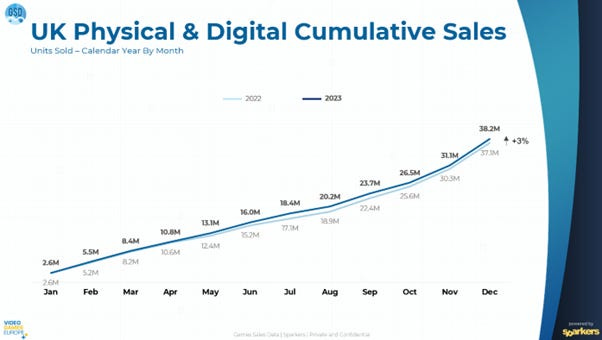

SJN Insights: Analysis of the UK Gaming Market in 2023

The analysis is based on data from GSD and GfK. It includes actual sales figures shared by publishers and stores.

The number of copies sold in 2023 increased by 3% compared to 2022. That's 38.3 million games.

Until May 2023, sales dynamics mirrored those of 2022. It was only from May onwards that the market surged, largely due to The Legend of Zelda: Tears of the Kingdom and Diablo IV.

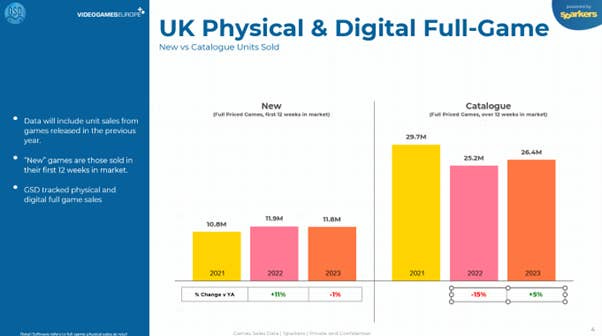

When comparing sales of new games (games less than 3 months on the market), 2023 unexpectedly turned out to be 1% worse than 2022 (11.8 million copies). However, back-catalog sales (games older than 3 months) grew by 5% compared to 2022.

❗️The calculation methodology used by GSD and GfK is somewhat atypical. In my opinion, the back-catalog should include projects released before the reporting year.

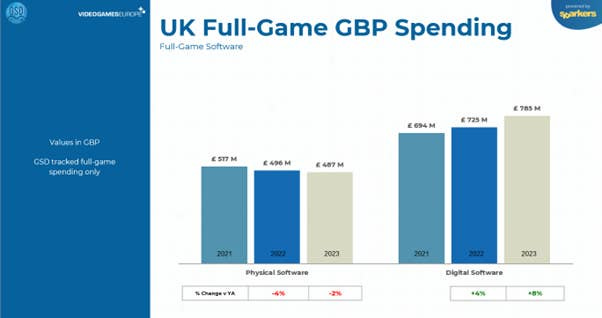

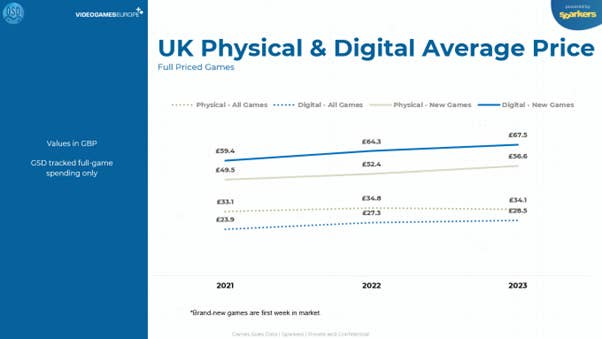

User spending on games increased by 4% - reaching £1.27 billion. Digital sales saw an 8% growth (£785 million), while physical copy sales decreased by 2% (£487 million).

The number of digital version sales is increasing, but the rate of replacing boxed versions of games has slowed down.

The average price of new physical format games increased by 14% in 2023 (£57), compared to 2021 (£50). A similar percentage growth is seen in digital versions - from £59 in 2021 to £68 in 2023.

The average price of all disc format games increased from £33 in 2021 to £34 in 2023. The growth is more noticeable in digital format - from £24 to £29.

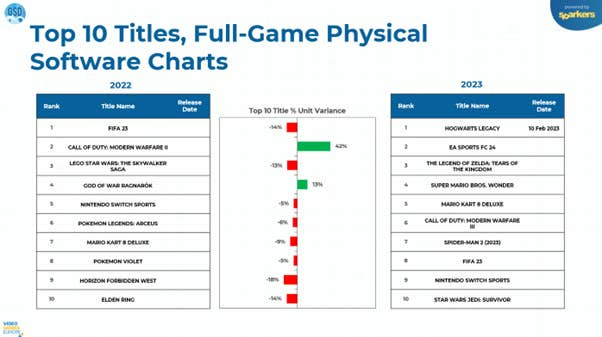

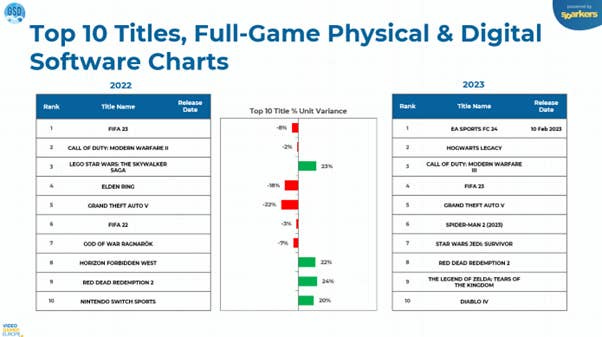

In 2023, games from the top 10 of the British chart sold 2% worse than the top 10 in 2022, considering only physical copies.

However, the situation is similar when considering digital versions.

❗️For some reason, British consumers were not very optimistic about new releases in 2023.

Game Sales Round-up (17.04.24 - 30.04.24)

Sea of Thieves has over 40 million users. The impressive milestone was announced a week before the release on PlayStation, and the player count has grown even more since then.

Buckshot Roulette reached over a million copies sold in 2 weeks. It's an indie horror game about "Russian roulette."

House Flipper 2 sold 13,088 copies on Xbox ($511.7k revenue) and 18,170 copies on PlayStation ($667k revenue) in the first 3 days on consoles. The results are four times worse than on PC, where the game was purchased 131 thousand times in a similar period in December 2023.

Frostpunk surpassed the great milestone of 5 million copies sold. An excellent achievement.

Consider subscribing to the GameDev Reports Premium tier to support the newsletter. Get access to the list of curated articles & archive of Gaming Reports that I’ve been collecting since 2020.

Users have spent over $8 billion on Pokémon GO since its release, according to AppMagic analysts. During the same period, the game was downloaded over 656 million times.

Capcom and Niantic reported 15 million downloads of Monster Hunter Now. AppMagic notes that during this time, the game has earned $164 million gross.

Manor Lords sold over 1 million copies within a day of its release. At the time of launch, the game had over 3.2 million wishlists. The project's peak CCU is 173 thousand people. One person made the game, Greg Styczeń (Slavic Magic); Hooded Horse published the project.

In the first 2 weeks, over 65 million people watched the Fallout TV series. The majority of viewers are aged between 18 and 34. The top countries for viewership are the United Kingdom, France, and Brazil.

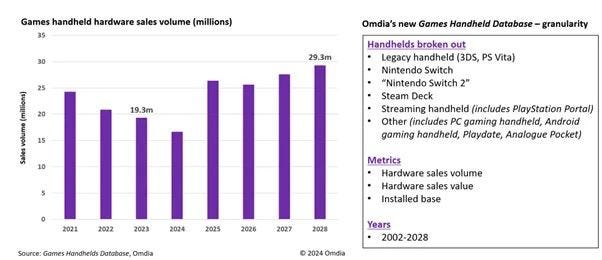

Omdia: 19.3 million handhelds were sold in 2023

This segment includes the Nintendo Switch; portable PC consoles (Steam Deck); streaming systems (PlayStation Portal); and historical portable consoles (Nintendo 3DS; PlayStation Vita).

Omdia notes that 19.3 million portable devices were sold in 2023, fewer than in 2021 and 2022.

❗️This is related to the end of the life cycle of the Nintendo Switch.

However, Omdia predicts rapid growth in the segment in 2025 - rumors suggest the release of the Nintendo Switch 2 then.

Omdia forecasts that in 2028, sales of portable gaming devices will reach 29.3 million units.

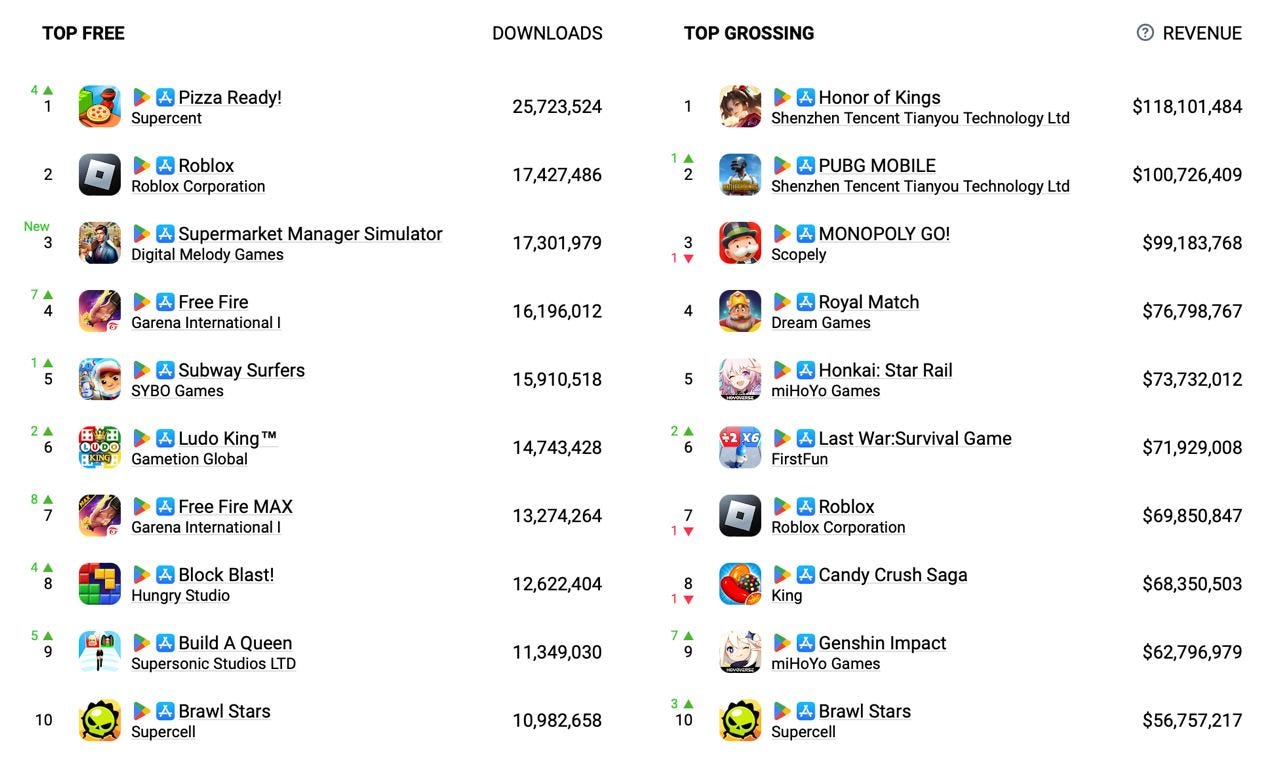

AppMagic: Top Mobile Games by Revenue and Downloads in April 2024

AppMagic provides revenue data net of store commissions and taxes.

Revenue

Honor of Kings is leading the chart with $118.1 million. I imagine writing this every month for the next decade…

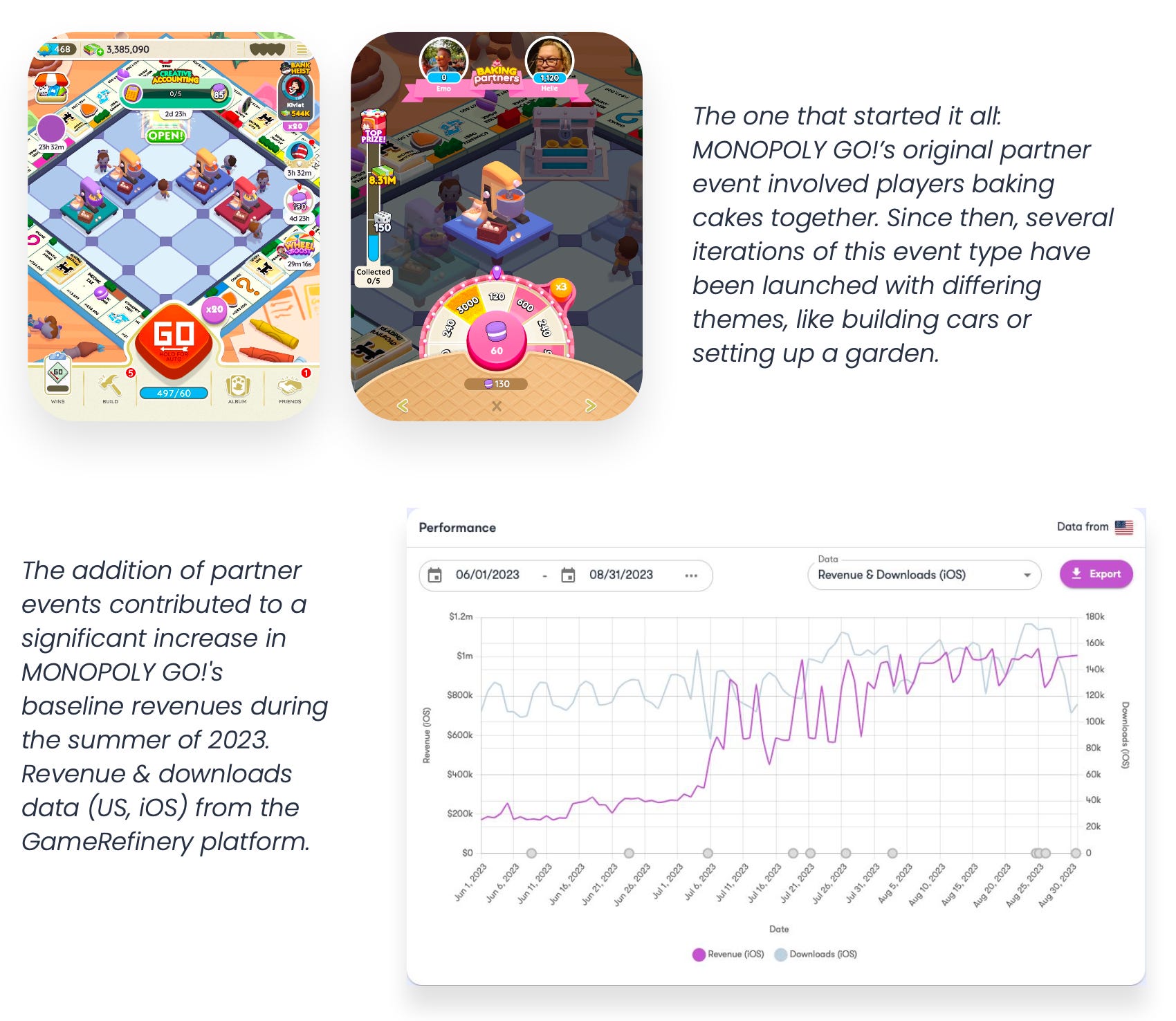

Monopoly GO! dropped to third place on the chart ($99.2 million). Its place was taken by PUBG Mobile ($100.7 million in April).

Last War: Survival Game is gaining in revenue; in April, the game earned $71.9 million.

Genshin Impact increased its revenue by half compared to the previous month. The game earned $62.8 million in April and jumped 7 positions in the rankings.

Brawl Stars continues its triumphant march. The game set a historical revenue record, earning $56.8 million in April.

Consider subscribing to the GameDev Reports Premium tier to support the newsletter. Get access to the list of curated articles & archive of Gaming Reports that I’ve been collecting since 2020.

Downloads

Pizza Ready! by Supercent topped the download chart. In April, the game was downloaded 25.7 million times.

Supermarket Manager Simulator - a newcomer in the download chart. In April, the project had 17.3M installs (3rd place). 28% of downloads from Brazil; 27% from the USA; 11% from the UK. You might’ve expected some idle title, but it’s a 3D simulation game.

The top 10 also includes two versions of Free Fire - Classic (16.2M downloads) and Max (13.3M downloads). Technically, if combined, Free Fire would be the most downloaded game of April.

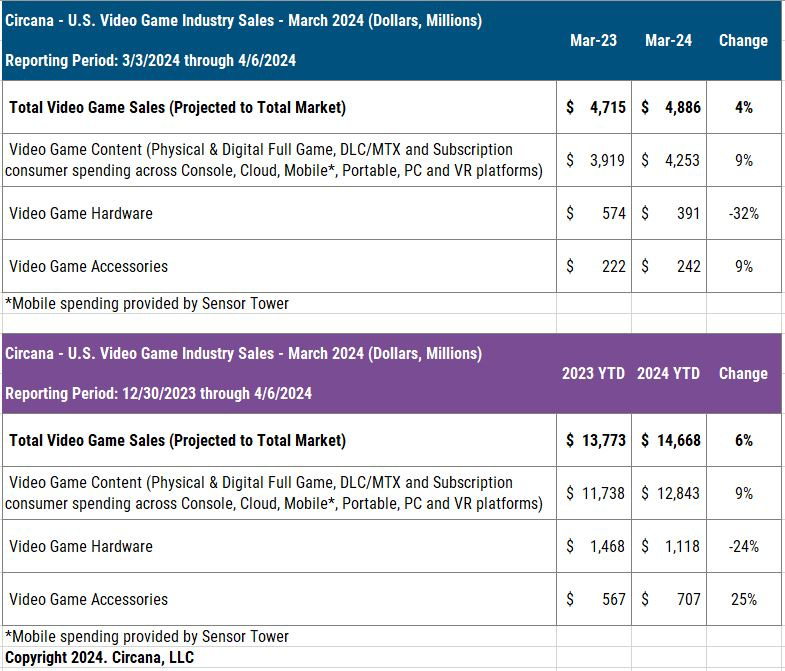

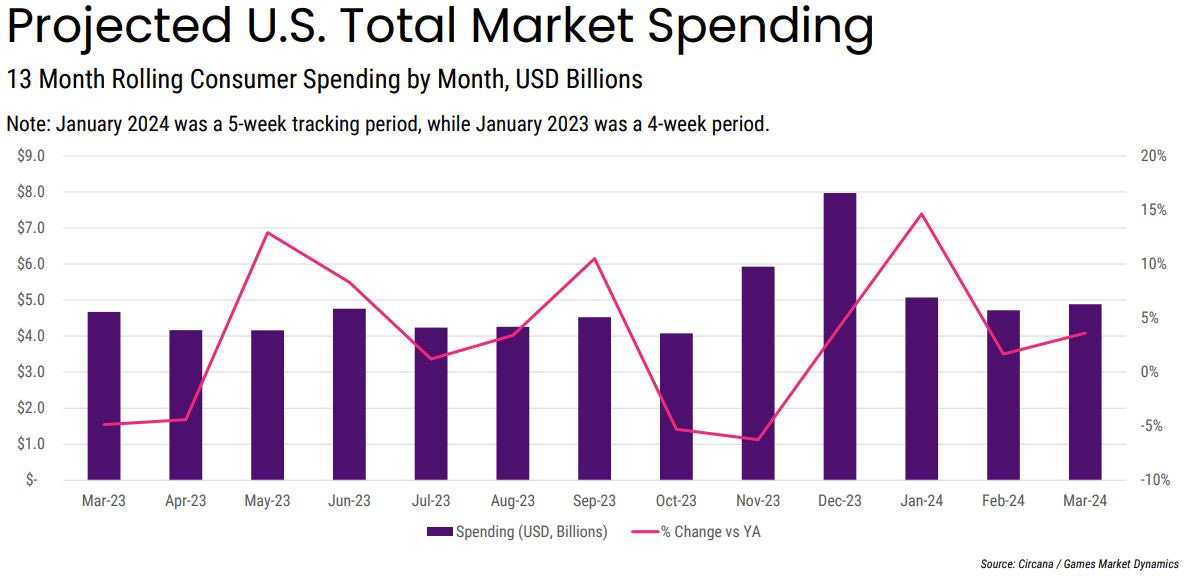

Circana: The US gaming market in March 2024 grew by 4%

General Numbers

In March 2024, the American gaming market reached $4.9 billion. This is 4% higher compared to the previous year.

Sales of gaming content grew by 9% compared to the previous year ($4.25 billion). Similar growth was shown in accessory sales ($242 million). However, sales of gaming devices fell by 32% to $391 million.

Comparing the first 3 months of 2024 to the first 3 months of 2023; the total revenue of the American market is 6% higher ($14.67 billion in 2024 versus $13.77 billion in 2023). Content sales are up by 9%; accessories by 25%. Gaming hardware sales are down by 24%.

DualSense Edge was the top-selling accessory in the USA in March 2024 and in the first quarter overall.

The mobile market in the USA grew by 3% in March. 89% of this month's growth was driven by the mobile market.

PC game sales, cloud services, and VR content outside of consoles grew by 2%.

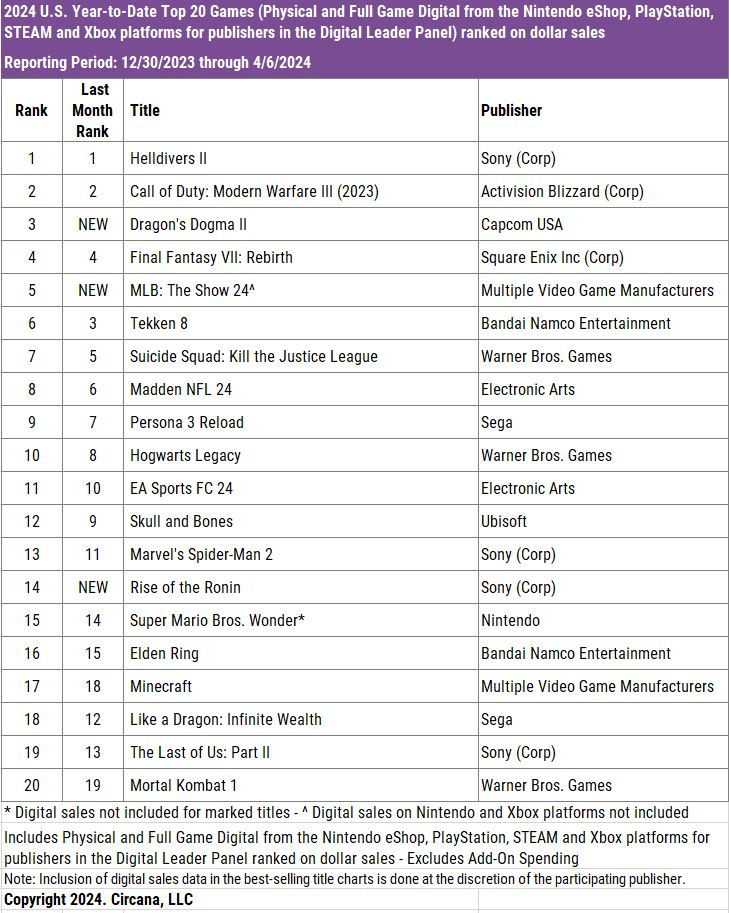

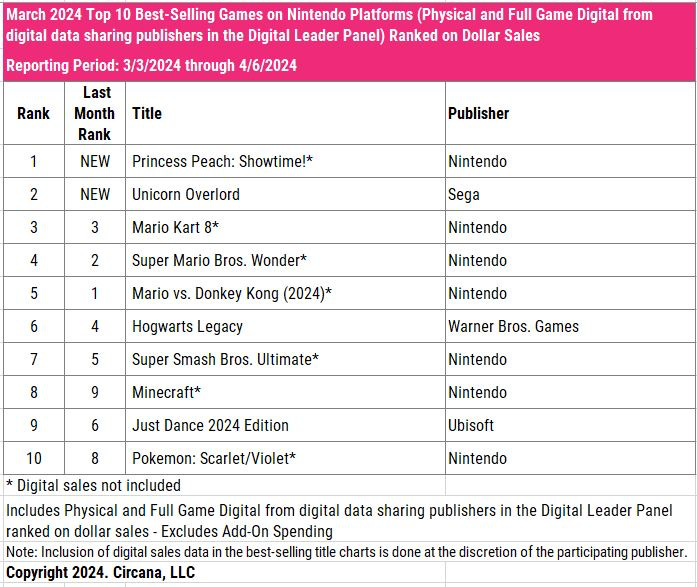

Bestselling Games

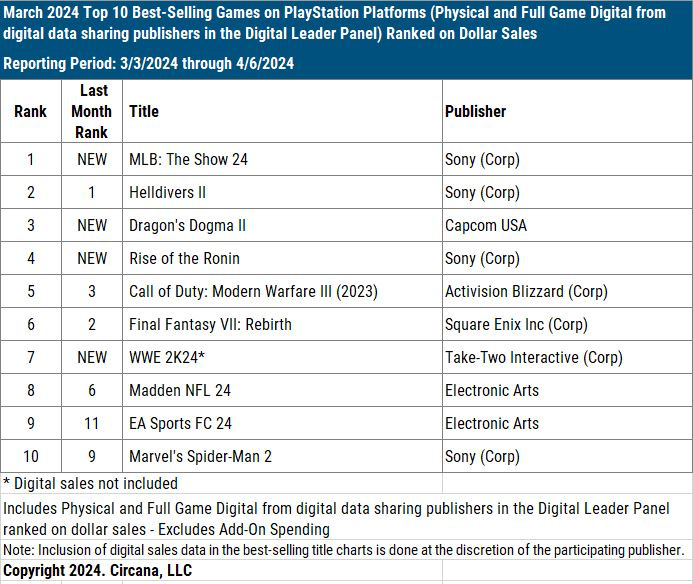

The best-selling game in March 2024 in the USA was Dragon’s Dogma II. Helldivers II dropped to second place.

March saw many new releases - MLB: The Show 24 (3rd place); Rise of the Ronin (5th place); Princess Peach: Showtime! (6th place - excluding digital versions); Unicorn Overlord (8th place), and WWE 2K24 (9th place - excluding digital versions).

For the first 3 months of 2024, Helldivers II is a solid leader. Call of Duty: Moder Warfare III took second place, and Dragon’s Dogma II claimed the third spot.

If only the PlayStation or PC versions of Helldivers II were considered in the ranking, the game would still be in first position. The release was that successful.

In just one month, Dragon’s Dogma II sales surpassed the combined sales of the original Dragon’s Dogma and Dragon’s Dogma: Dark Arisen.

Helldivers II is currently the 7th best-selling game in Sony's history in the American market. Without the PC version, it wouldn't even be in the top-20. Thus, the simultaneous release on PlayStation and PC was a huge success for Sony.

GameDev Reports Newsletter offers promotion opportunities to gaming companies. Reach out to learn more.

Final Fantasy VII: Rebirth is currently the 14th in the Final Fantasy series in terms of sales in the American market. Final Fantasy XV holds the top spot, followed by Final Fantasy VII: Remake and the original Final Fantasy VII.

The revenue leaders in the American mobile market were Monopoly GO!, Royal Match, and Roblox.

The fastest-growing game in the mobile market in March 2024 was Last War: Survival Game. The project grew by 40% in revenue compared to the previous month.

PC/Console Charts

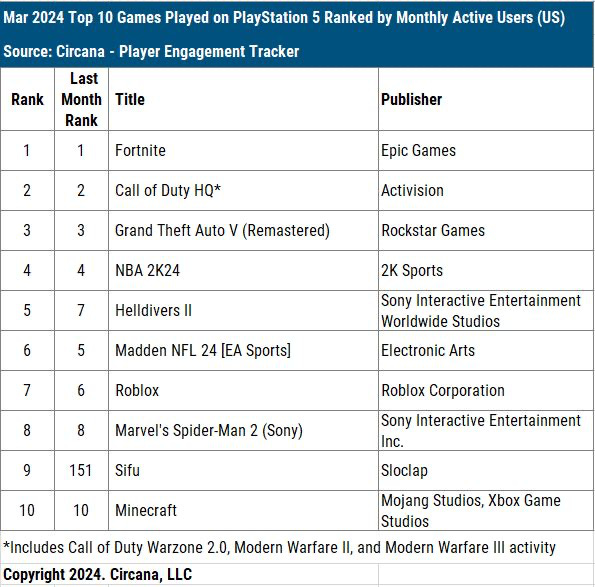

Fortnite, Call of Duty, and GTA V are the leaders in MAU (Monthly Active Users) on PlayStation. Helldivers II rose to the 5th position; Roblox finished at 7th place. Thanks to PS Plus, Sifu entered the chart at 9th place.

The best-selling games in March on PlayStation are MLB: The Show 24, Helldivers II, and Dragon’s Dogma II. New releases include Rise of the Ronin (4th place) and WWE 2K24 (7th place - excluding digital copies).

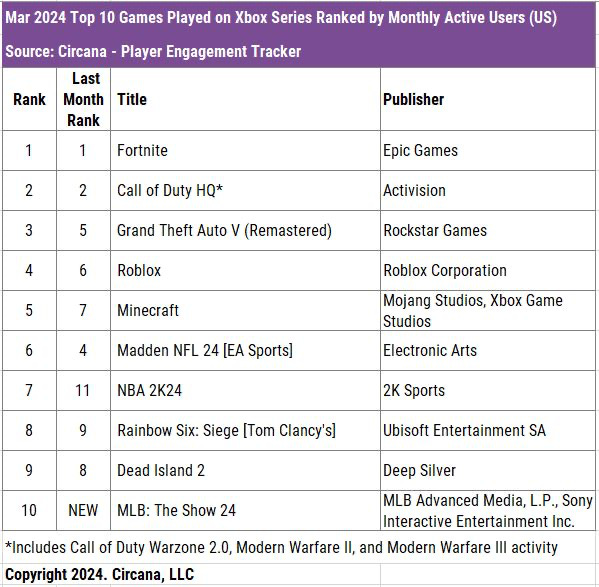

The MAU leaders on Xbox in the USA are the same as on PlayStation - Fortnite, Call of Duty, and GTA V. MLB: The Show 24, which is developed by Sony, is also in the top 10.

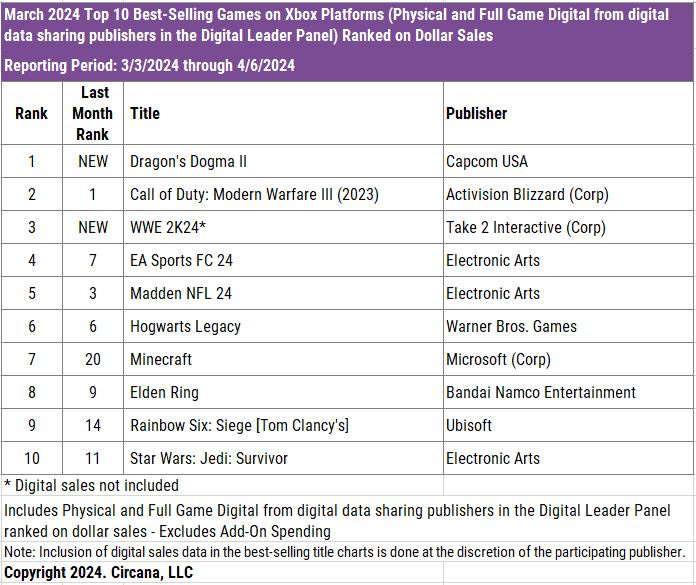

The top-selling games in March on Xbox are Dragon’s Dogma II, Call of Duty: Modern Warfare III, and WWE 2K24. Overall, Xbox's chart is more stable than PlayStation's.

Helldivers II is the MAU leader on PC. Counter-Strike 2 is in second place, and Baldur’s Gate III is in third. Dragon’s Dogma II is in 6th position.

The best-selling games on Nintendo Switch are Princes Peach: Showtime! (excluding digital versions), Unicorn Overlord, and Mario Kart 8 (also excluding digital versions).

Liftoff & GameRefinery: Casual Games in 2024

The data for the report was collected from April 1, 2023, to April 1, 2024. 355B impressions, 36B clicks, and 90M installations were tracked.

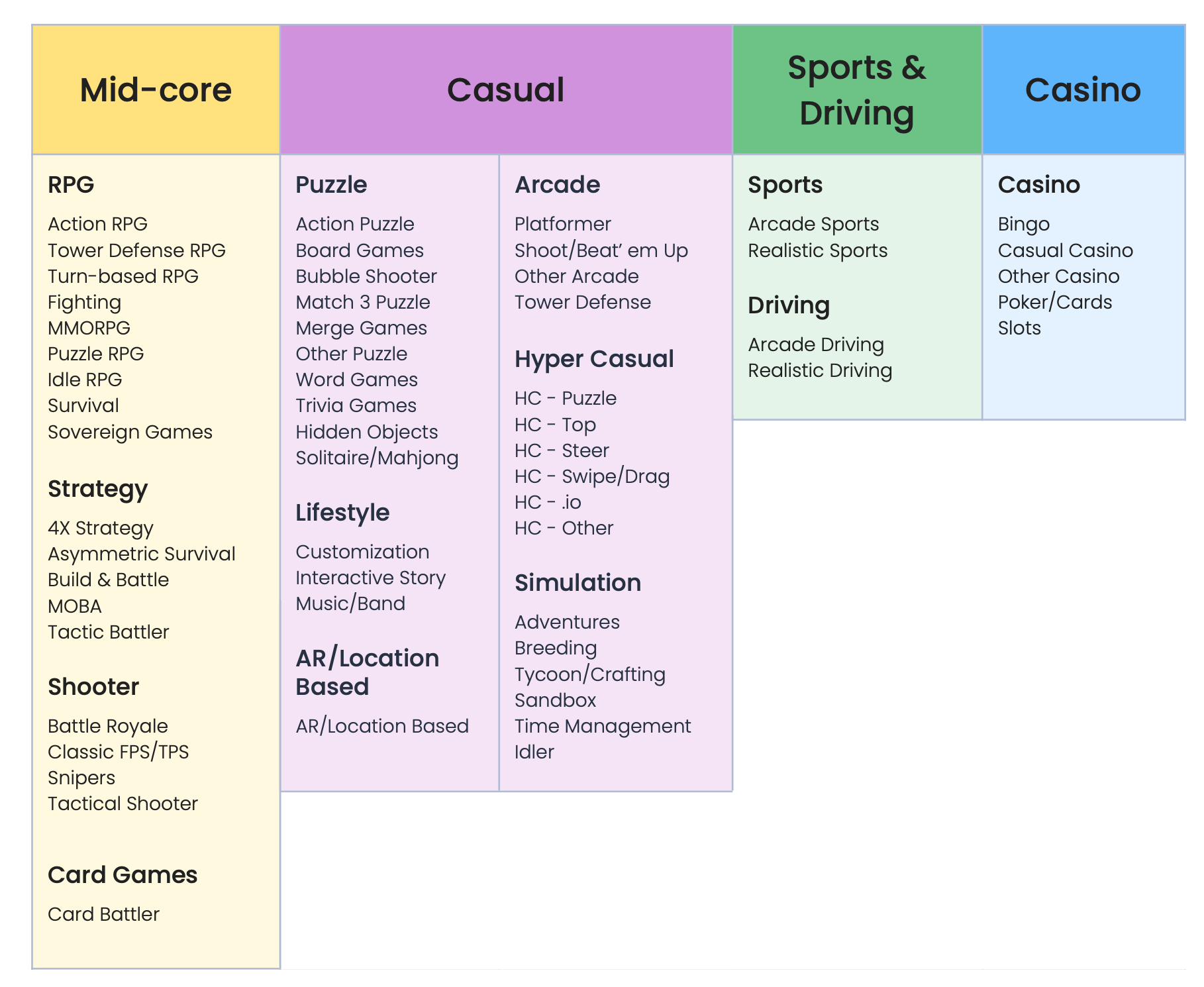

Liftoff and GameRefinery consider puzzle games, lifestyle projects (interactive stories, musical projects), and simulators (city builders, adventure projects) as casual games. Hyper-casual games are also taken into account.

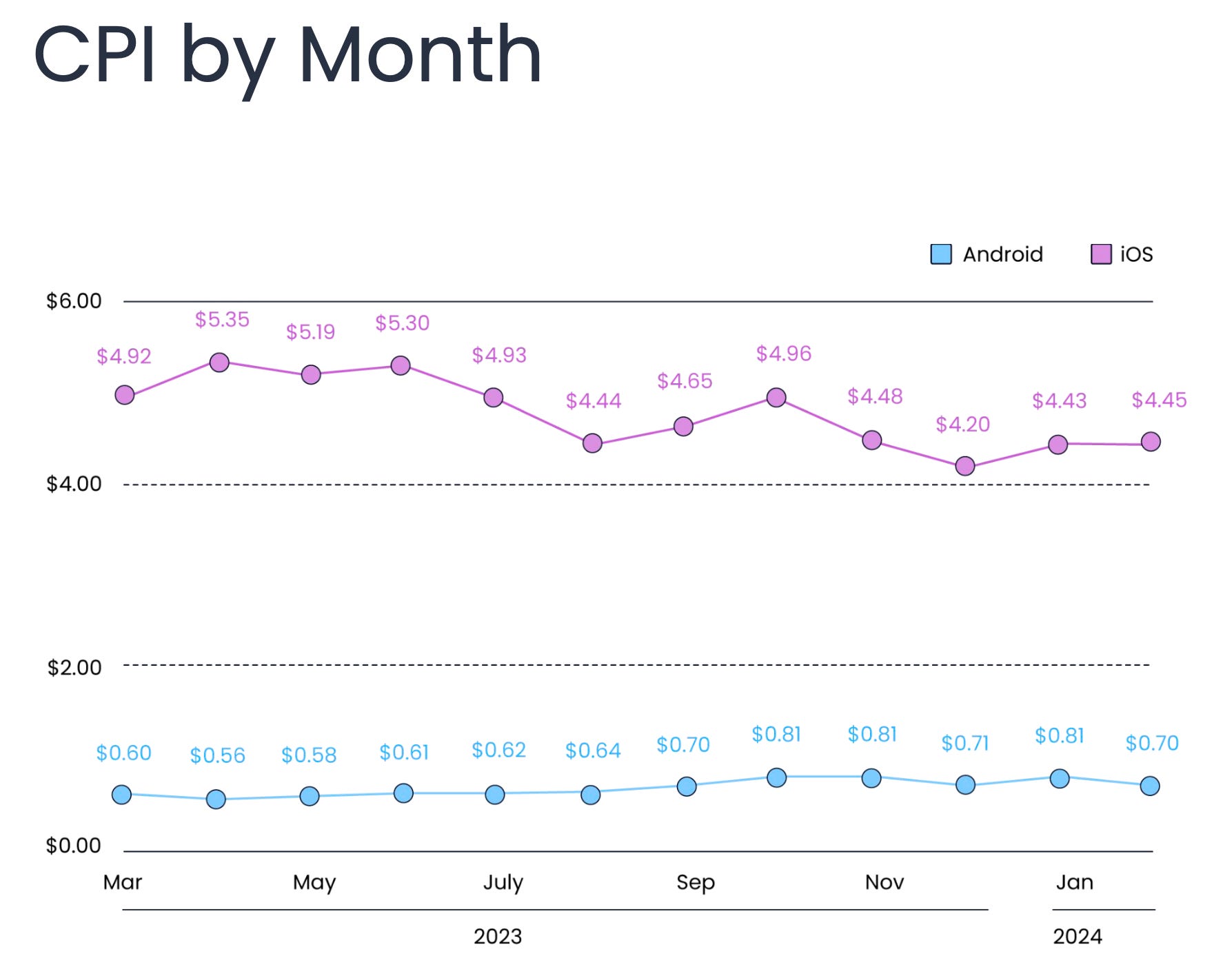

CPI Benchmarks

Average CPI for casual games - $2.17. On Android - $0.65; on iOS - $4.83.

On iOS, the highest CPI in 2023 was from March to May, after which it declined. On Android, however, growth occurred in the second half of the year - from September to December. Thus, platform seasonality is not identical.

$6.78 - average CPI in casual games in North America (NAMER). In EMEA - $1.11; in APAC - $1.05; in LATAM - $0.44.

The highest CPI is for lifestyle projects - $2.95; puzzles - $2.23; followed by simulators - $1.77.

GameDev Reports Newsletter offers promotion opportunities to gaming companies. Reach out to learn more.

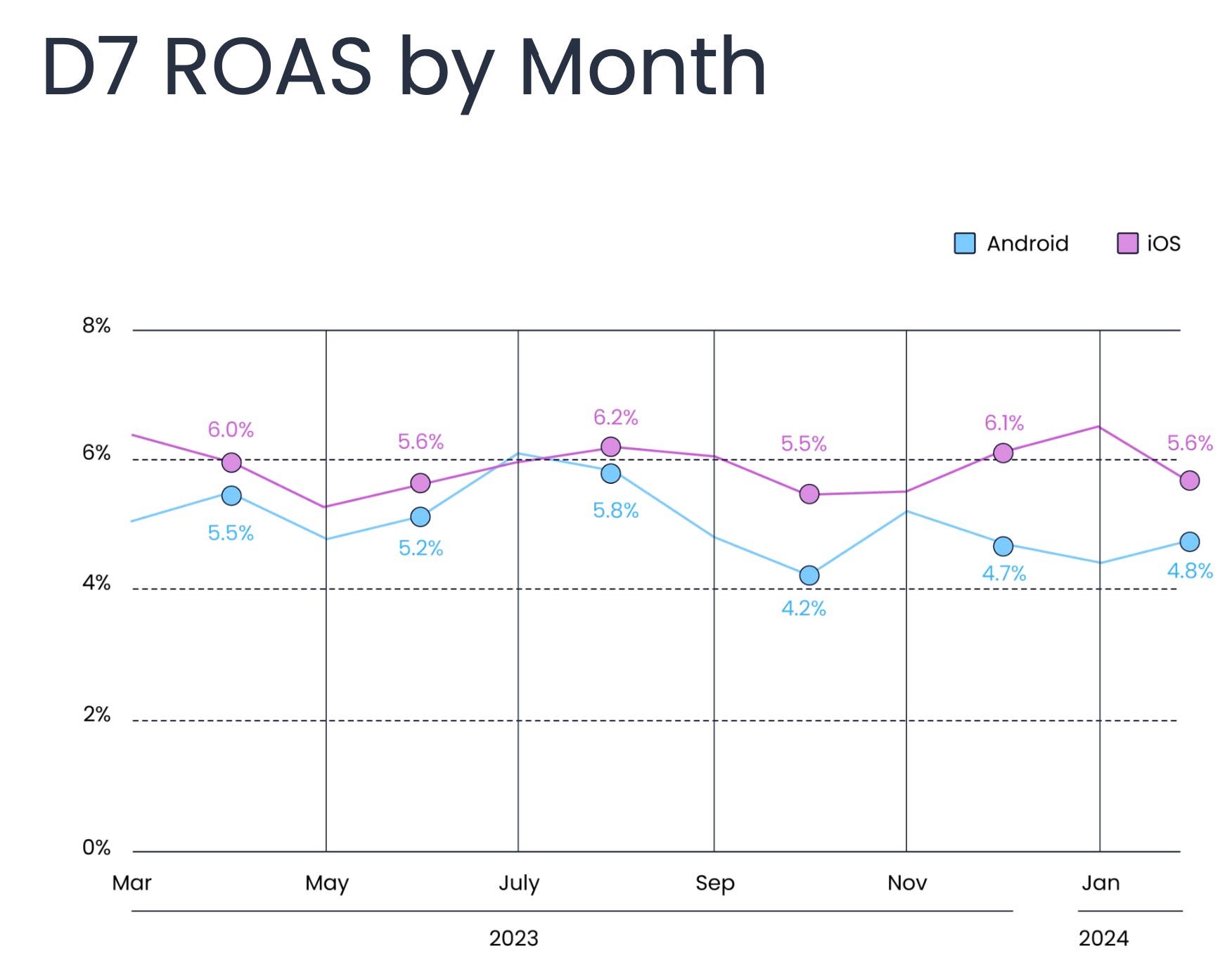

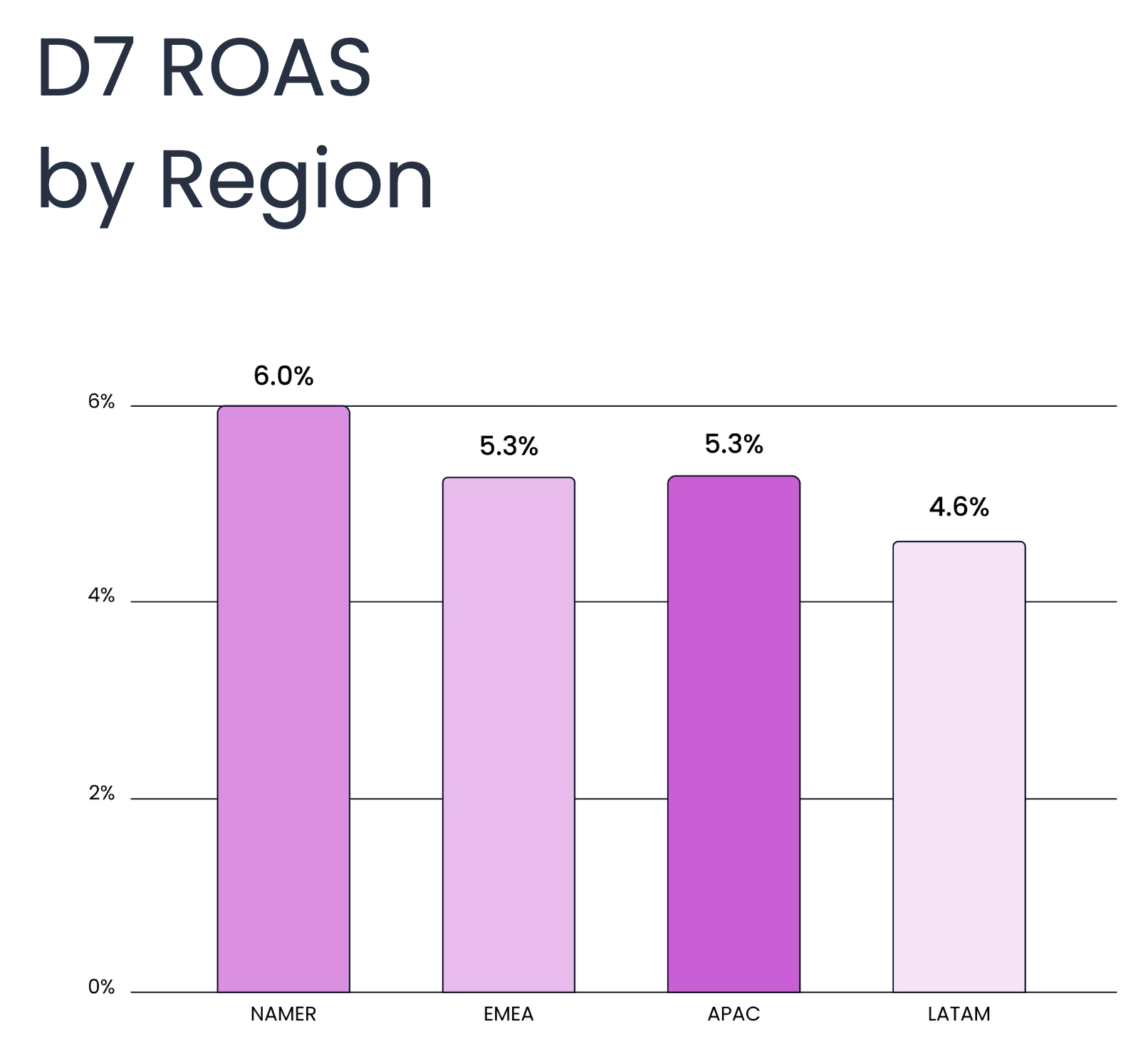

D7 ROAS Benchmarks

Average D7 ROAS in the casual genre - 5.7%. Slightly lower on Android - 5.1%; higher on iOS - 5.9%.

In the NAMER region, the average D7 ROAS reaches 6%; in EMEA - 5.3%; in APAC - 5.3%; in LATAM - 4.6%.

❗️I’d like to note that the figures are market averages. For successful products, both CPI and ROAS metrics can be (and most likely are) significantly different.

Downloads Sources

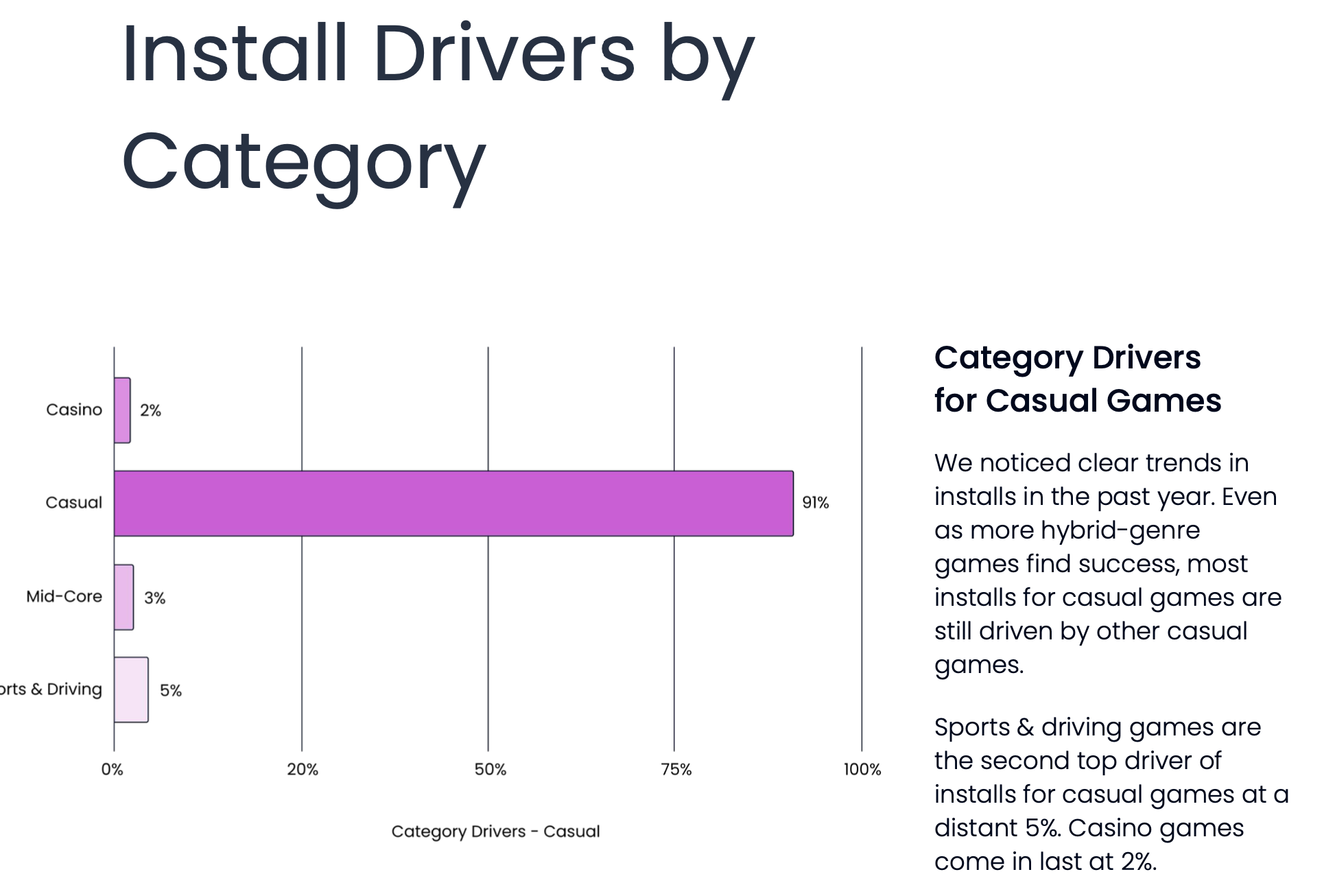

91% of traffic for casual games comes from... other casual games. 5% - from racing and sports games. 3% - from mid-core projects. 2% - from casinos.

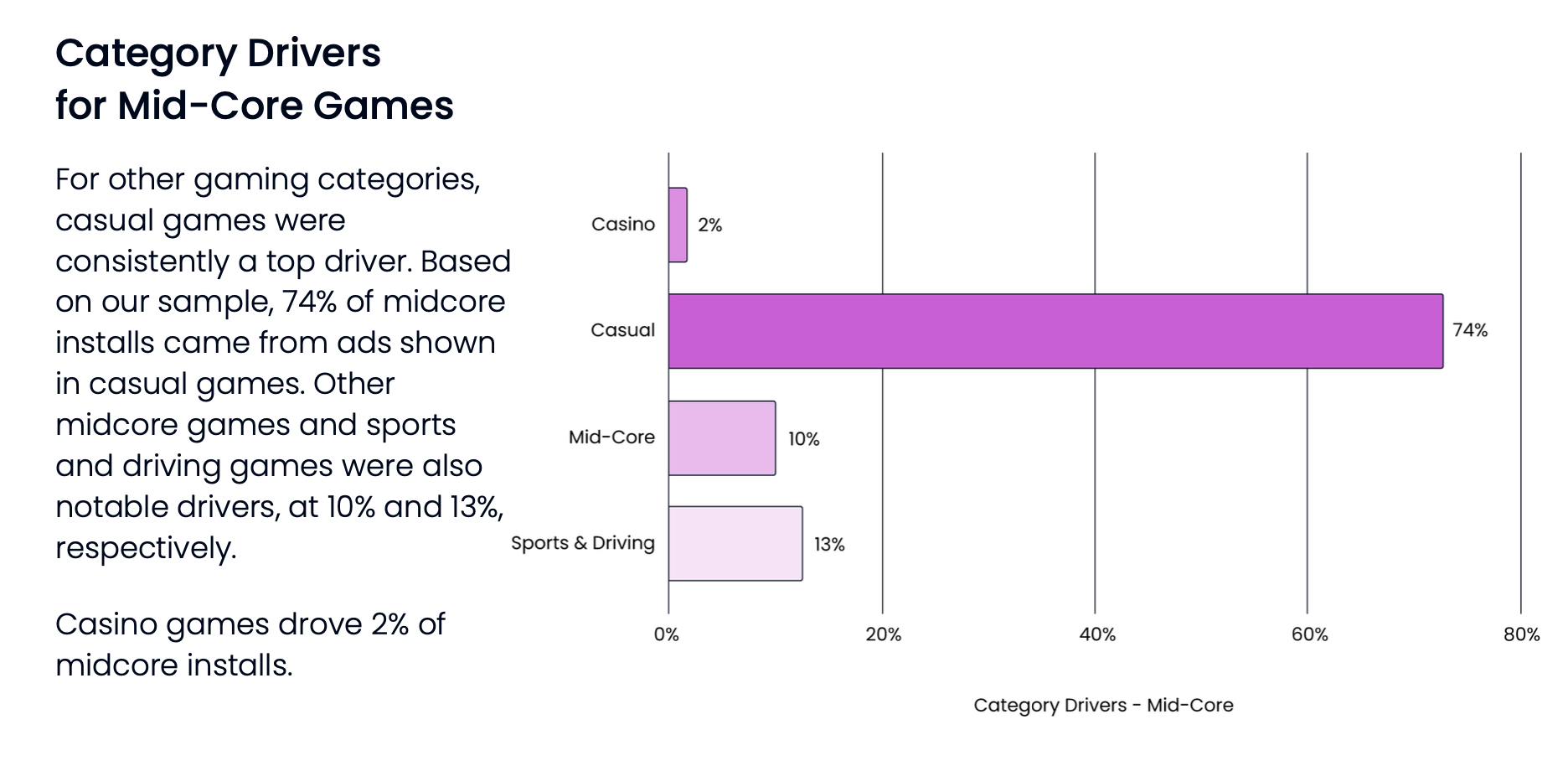

However, 74% of installations for mid-core games also come from casual projects. 13% - from sports and racing games; 10% - from other mid-core projects; 2% - from casino titles.

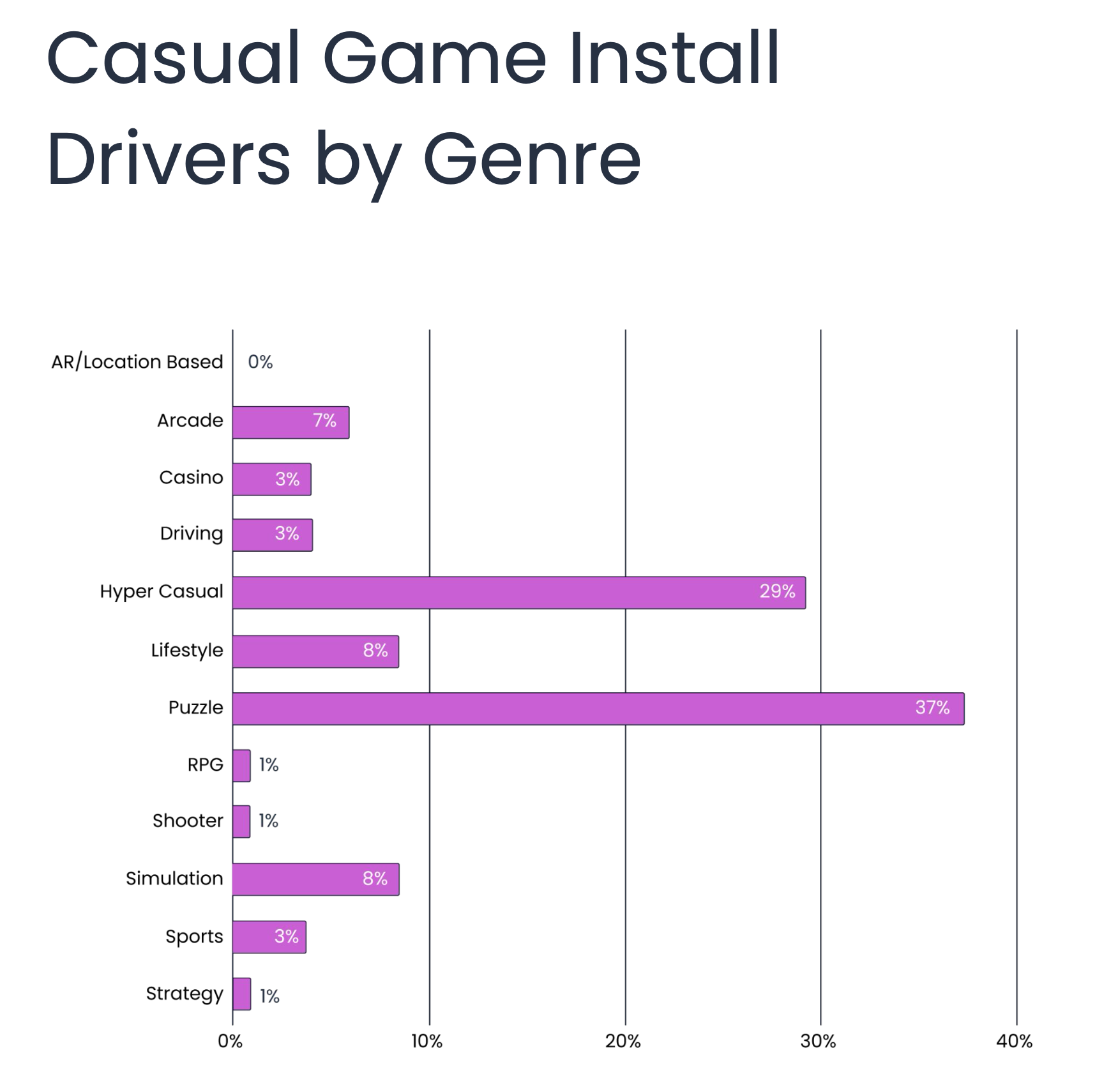

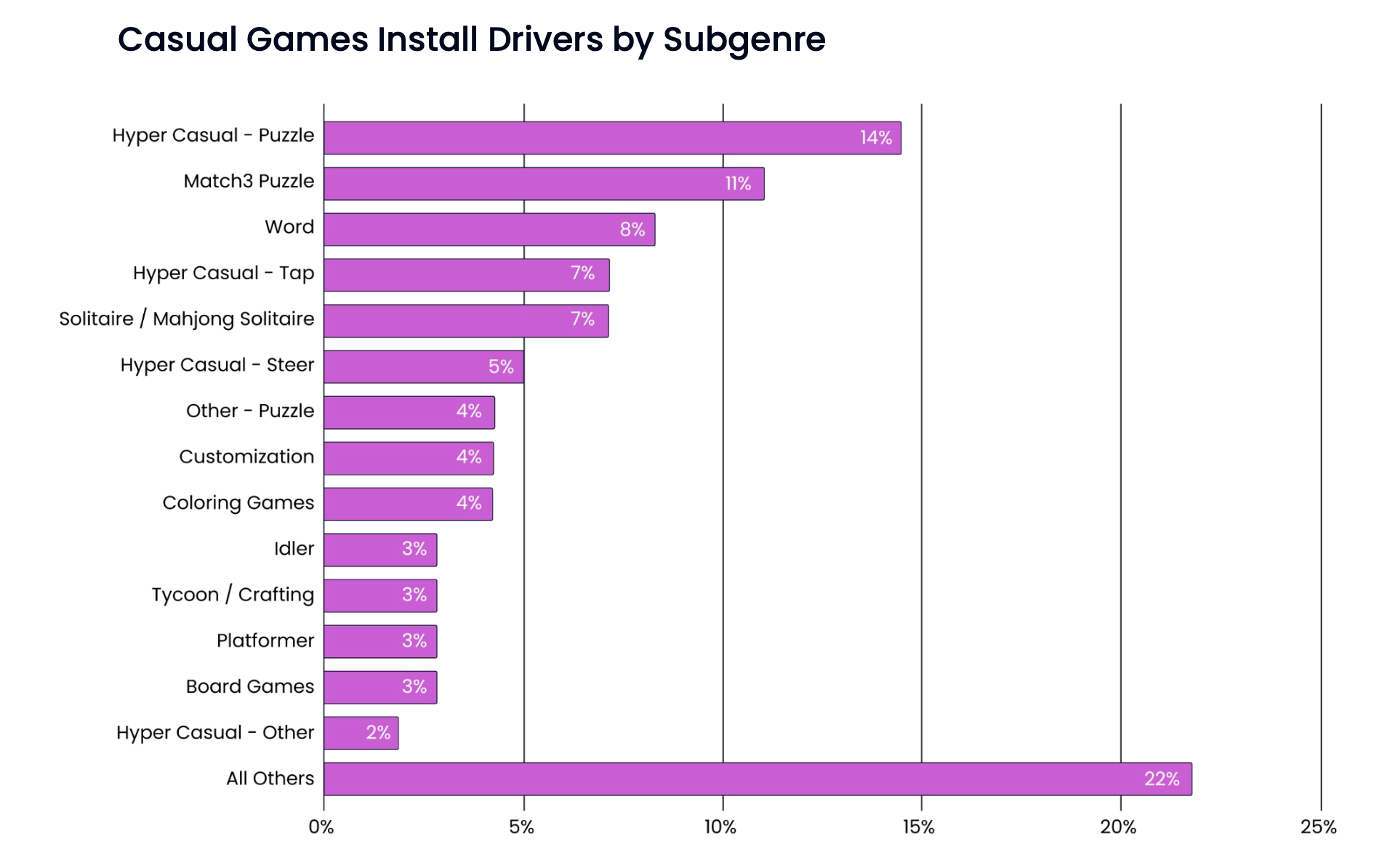

Puzzles account for 37% of all installs of casual games. Hyper-casual projects for 29% (and this share is decreasing); lifestyle projects and simulators for 8% each.

Looking at subgenres, hyper-casual puzzles lead - they account for 14% of downloads. They are followed by Match 3 (11%); then Word games (8%).

Noteworthy Genres and Projects

Match 3D is gaining popularity. According to GameRefinery, the subgenre market share in the top 500 in the USA grew from $2.95 million in Q4’22 to $15.25 million in Q4’23.

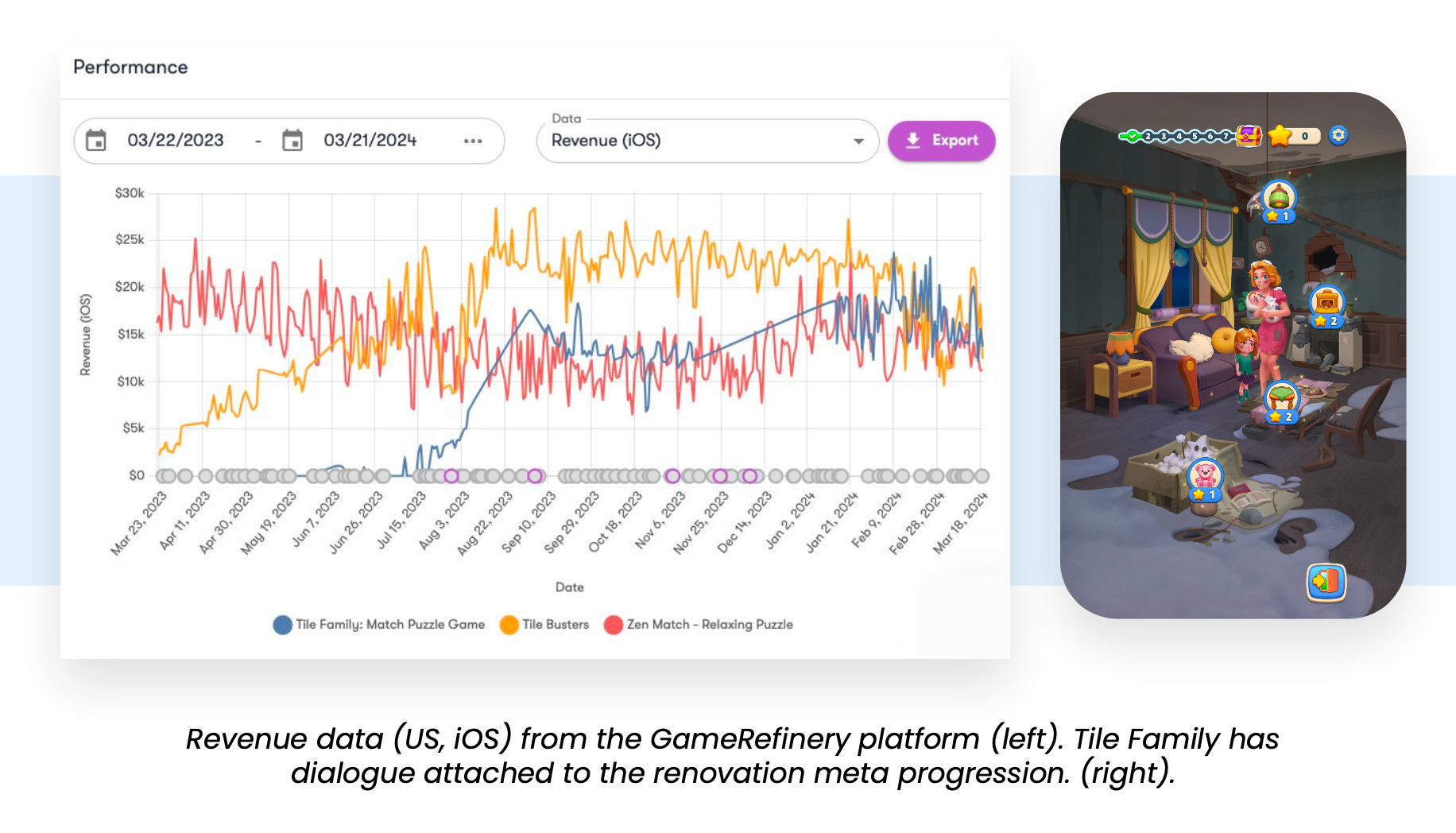

The Mahjong solitaires are showing traction. The main growth drivers are Tile Busters and Tile Family.

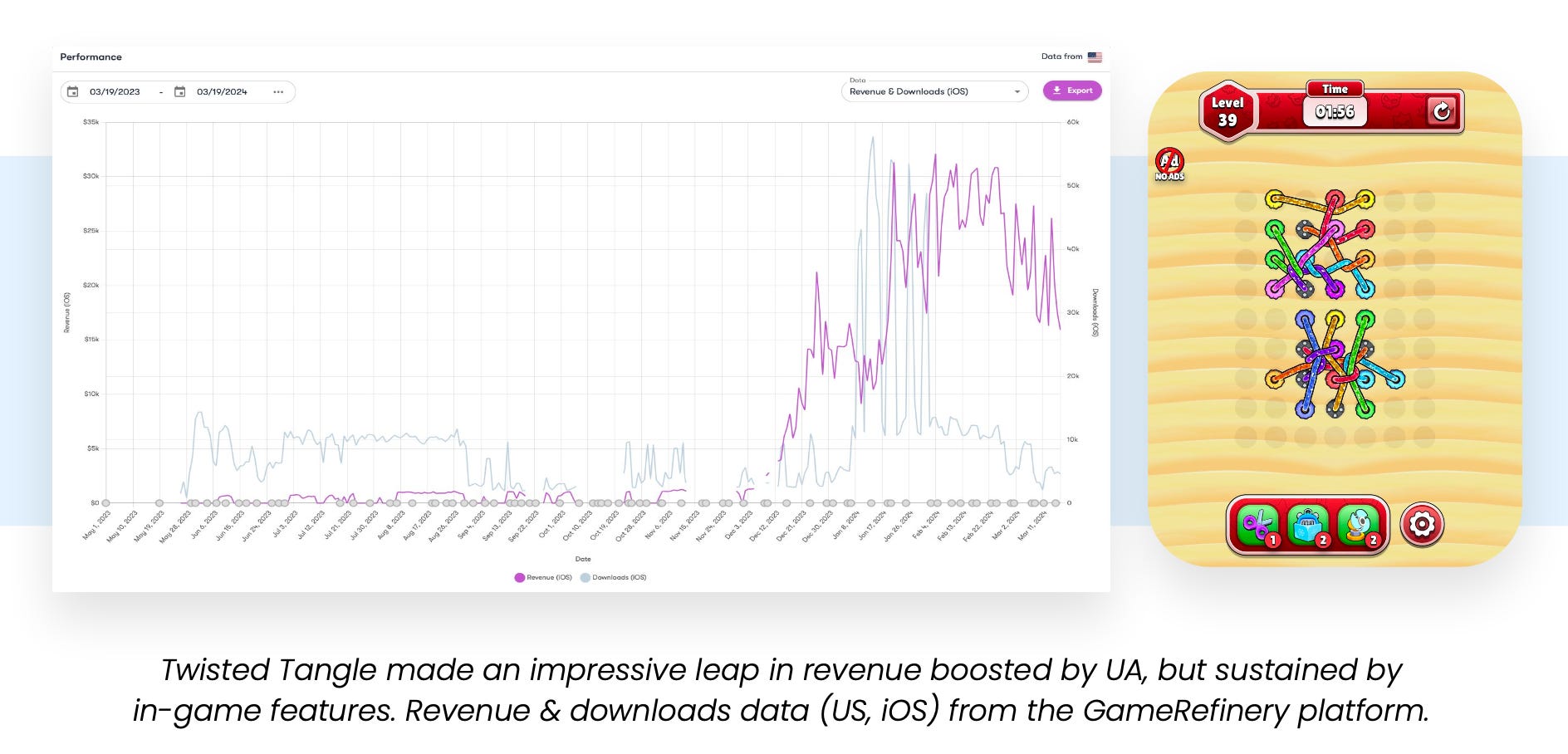

Twisted Tangle - a new hyper-casual hit from Rollic - originated from advertising creative. Since its revenue growth in December 2023, the game has solidified its position in the top 200 by revenue in the USA.

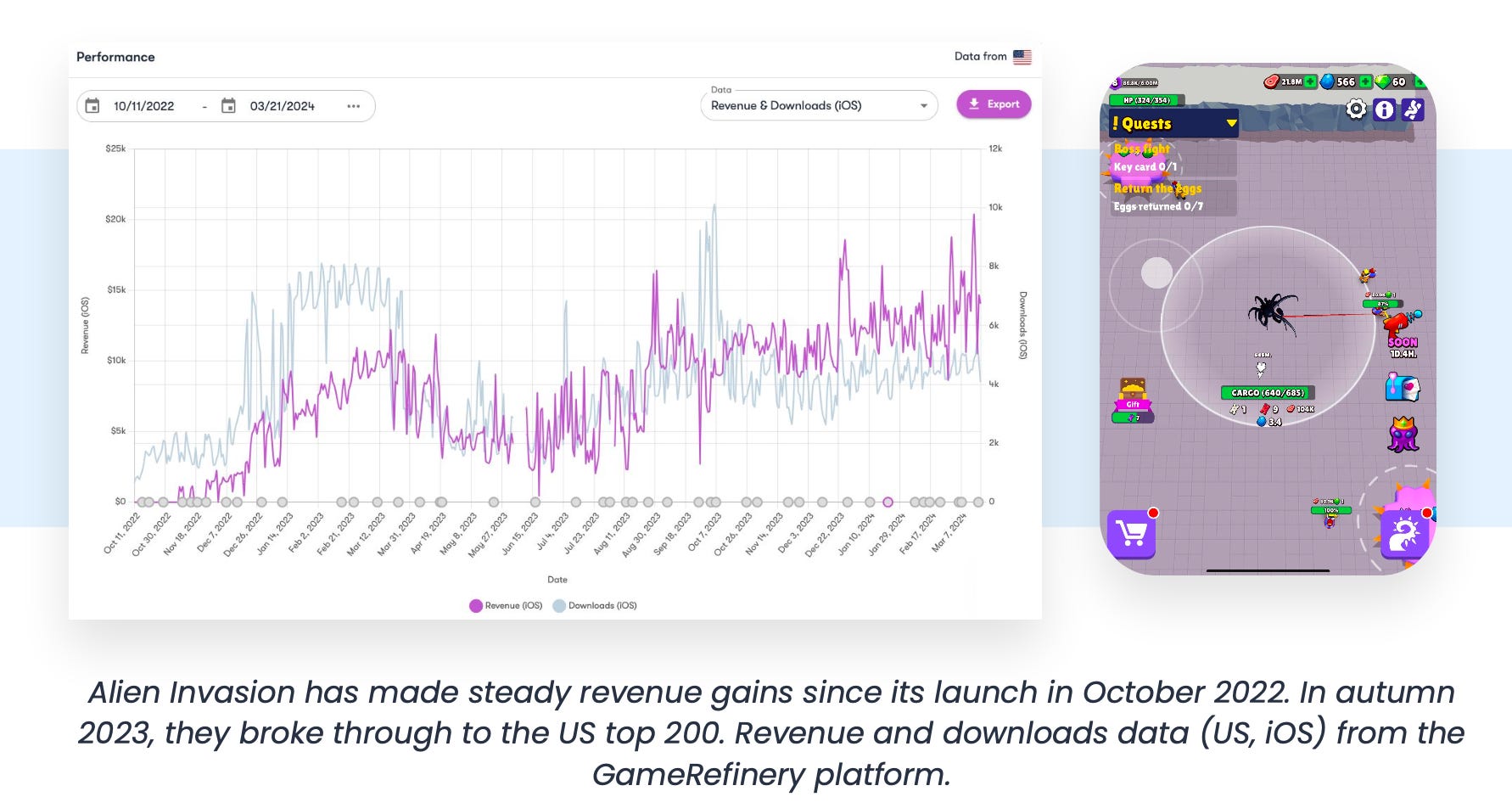

Alien Invasion continues to grow actively since its release in October 2022. This proves that hybrid casual games can linger on the market for a long time.

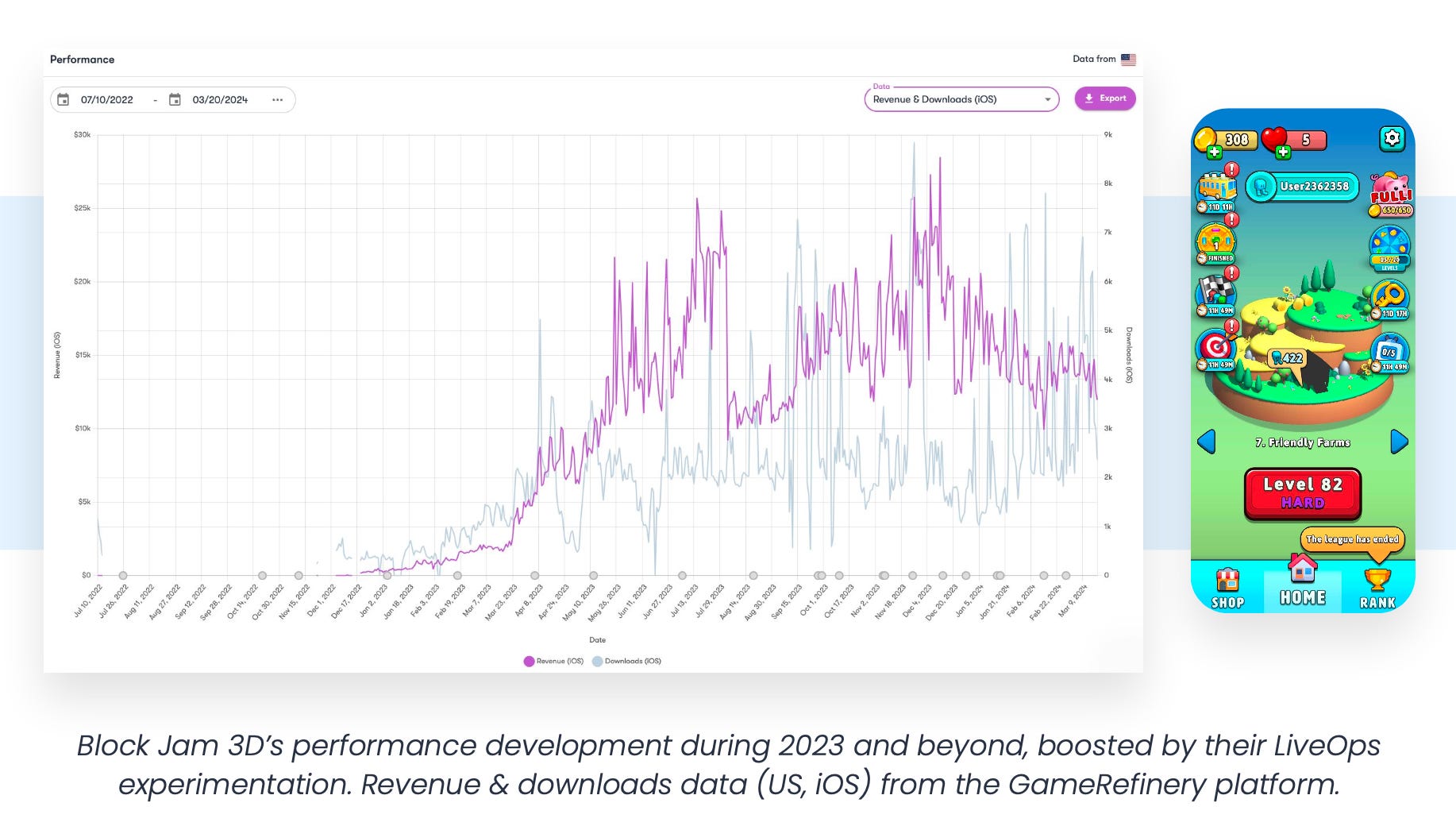

GameRefinery notes similar success with Block Jam 3D. Especially, the team praised the LiveOps of the game.

Trends in Casual Games

Digging events. They appeared in Legend of Slime; Royal Match applied the same mechanic in June 2023, becoming the first of casual games to do so. Since then, it has appeared in many other casual projects.

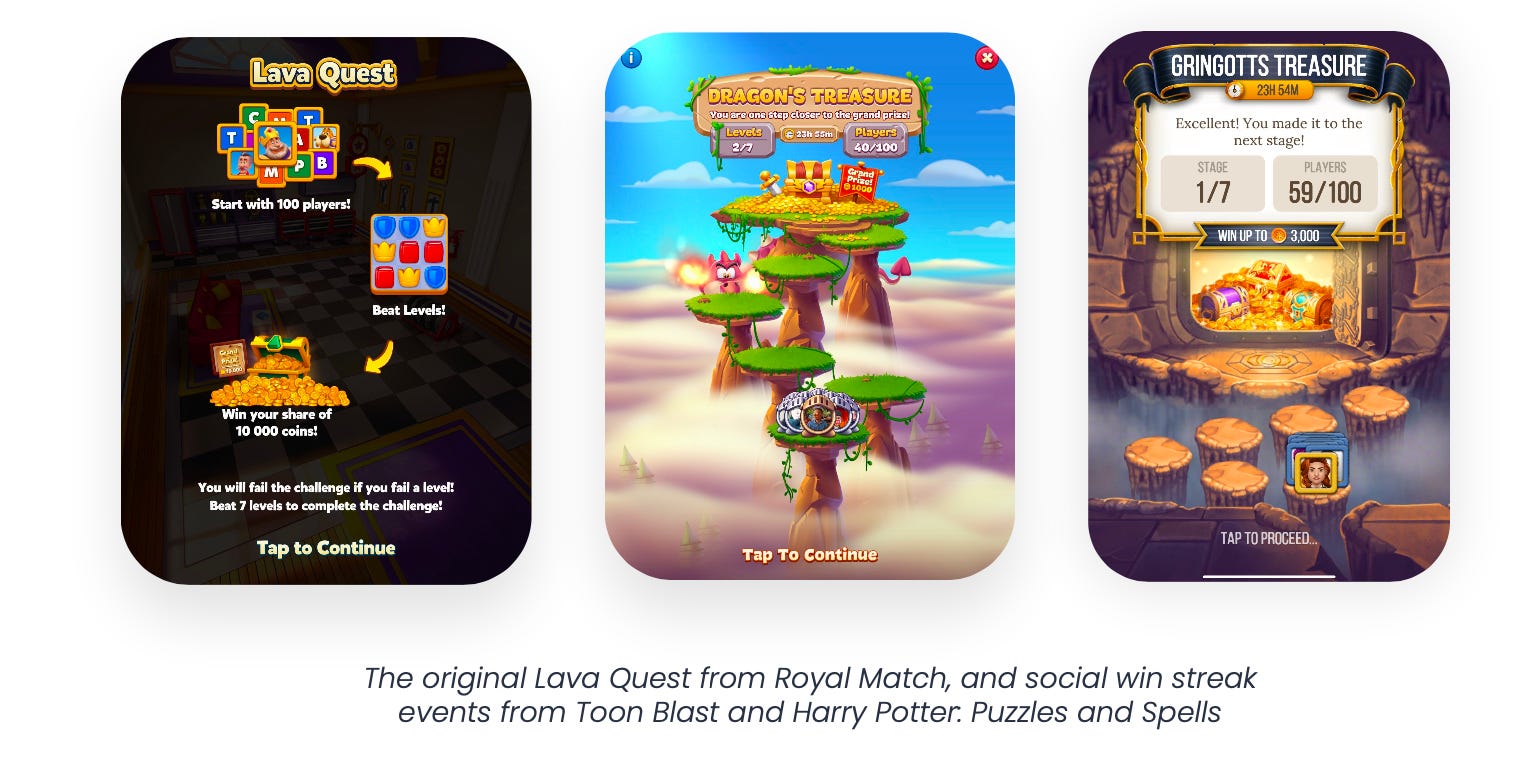

Social win streak events. The mechanics first appeared in Royal Match (Lava Quest) in March 2023. In this mode, the player competes with 99 other users; whoever completes successful levels in a row faster receives a reward. Toon Blast and Harry Potter: Puzzles and Spells have already implemented such mechanics.

Partnership events. The essence of the mechanic is to unite users towards a common goal (for example, in Monopoly GO! - bake a cake).

Monetization Trends

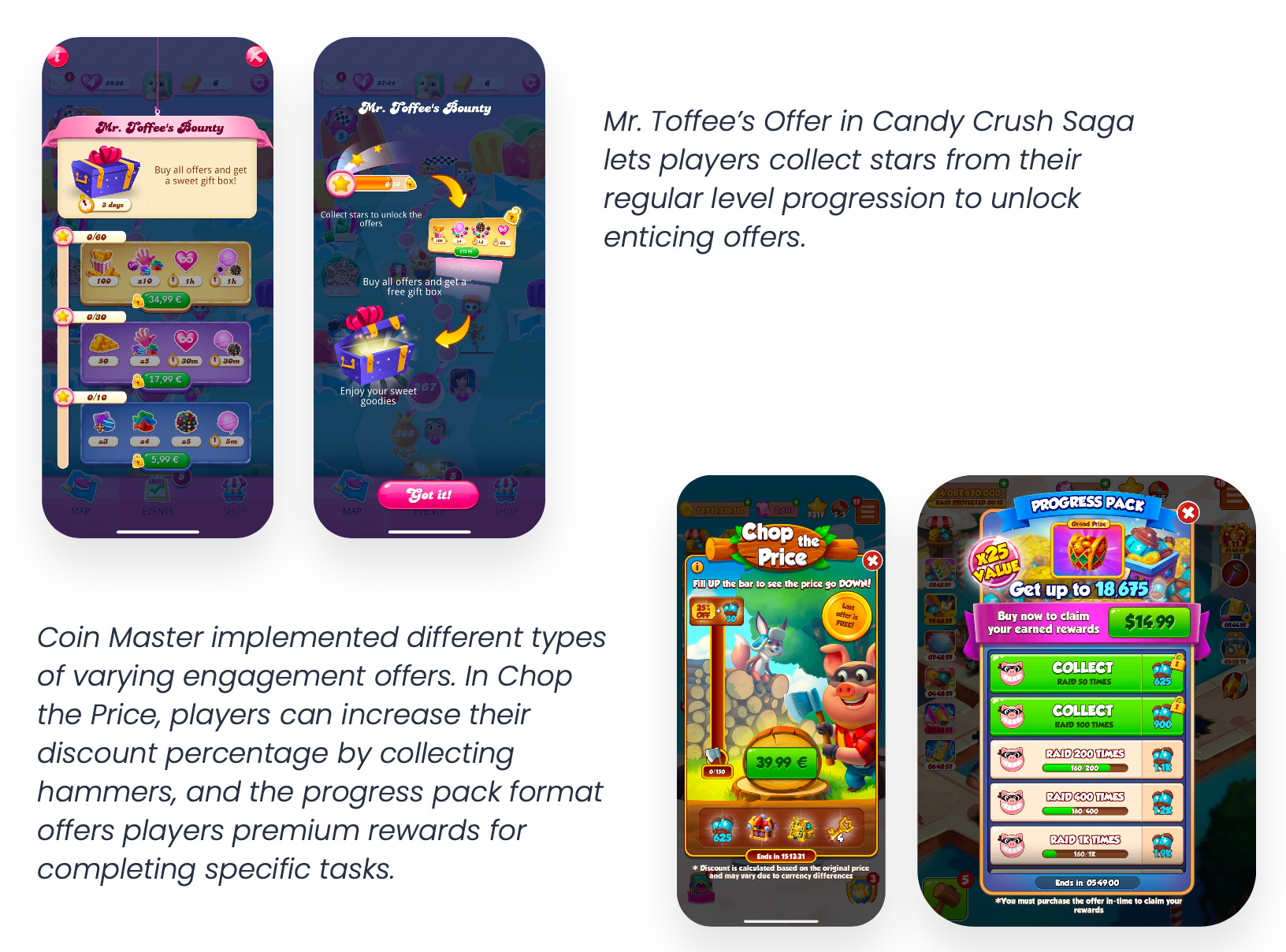

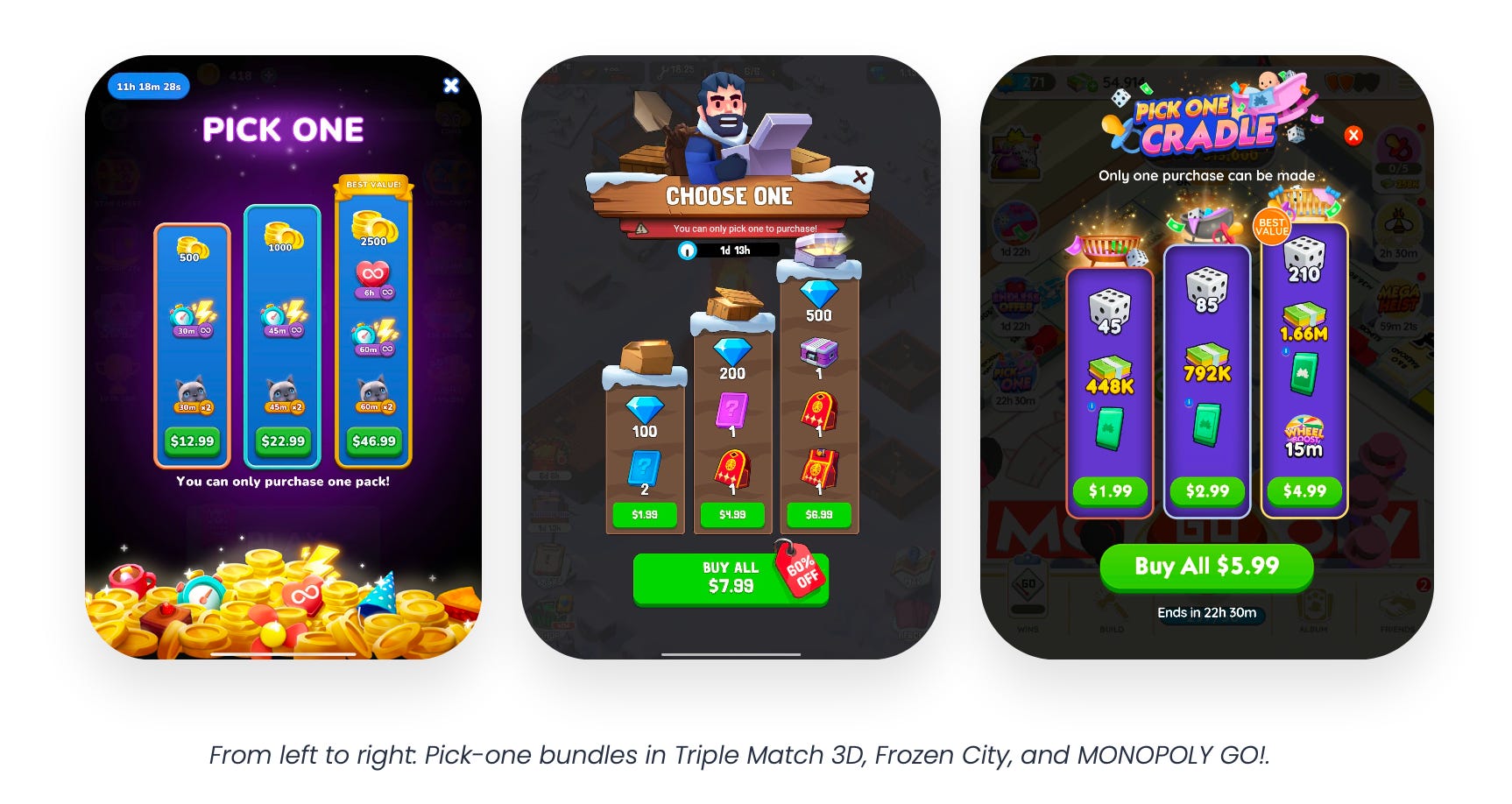

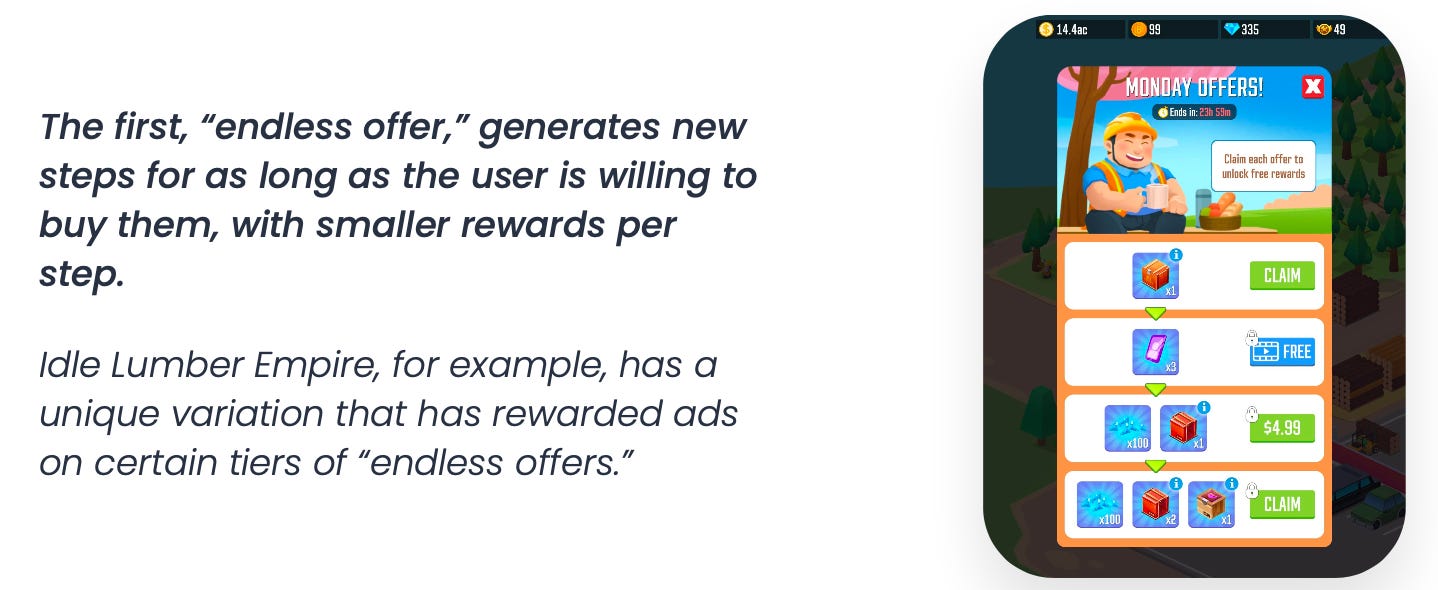

Pick-one Bundles. In 2024, developers increasingly offer the player to choose one offer from several (usually three) with different prices and values.

Progressive offers. First introduced by Royal Match in June 2021, they continue to gain popularity. Now this type of offer can be found in 70% of casual games in the top 25 in the USA by revenue. The mechanic is simple - a chain of offers is proposed, where the first (or several first) offers are free, and then a paywall is set, behind which there are several more "free" rewards.

Consider subscribing to the GameDev Reports Premium tier to support the newsletter. Get access to the list of curated articles & archive of Gaming Reports that I’ve been collecting since 2020.

Engagement offers. GameRefinery first noted them at the end of 2023. This type of offer combines Battle Pass, Piggy Bank, and other monetization mechanics. The player is offered to perform certain actions to improve the offer/increase the discount.