Weekly Gaming Reports Recap: March 18 - March 22 (2024)

Weekly Gaming Reports Recap: March 18 - March 22 (2024)

Gaming mobile trends by Adjust & AppLovin in 2024; DDM shared the investment status for the 2023; European market grew (or not) in February 2024.

Reports of the week:

Sensor Tower: Japan accounted for nearly 50% of the revenue from geolocation Mobile games in 2023

Game sales Round-up (06.03.2024 - 19.03.2024)

Adjust & AppLovin: Mobile Game Market Trends in 2024

DDM: Gaming Investments in Q4 2023; 2023 Results and 2024 Forecasts

GSD & GfK: The European Gaming Market Actually Grew in February 2024

Sensor Tower: Japan accounted for nearly 50% of the revenue from geolocation Mobile games in 2023

Revenue from location-based games in Japan exceeded $620 million in 2023. This accounts for 49.5% of the global market. The second-place, with 27.9%, is the United States.

Dragon Quest Walk is the highest-earning location-based game in Japan; users spent over $300 million on it in 2023. In second place is Pokemon GO (about $220 million).

In the United States, Pokemon GO performs significantly better. The game earned $300 million in the American market in 2023. An additional $14 million came from South Korea.

Location-based games account for 5% of all mobile game revenue in Japan.

The genre in Japan has about 40% female audience. The average age is 35 years.

Sensor Tower believes that location-based games fit well into the lifestyle of the Japanese, who actively use public transportation. This is indirectly confirmed by the peaks of activity in location-based games - in the morning and evening when people return from work. In contrast, the peak for "traditional" games is at 9 p.m.

Game sales Round-up (06.03.2024 - 19.03.2024)

Total sales of the Persona series have reached 22.6 million copies. Of this number, more than 10 million belong to Persona 5 and its spin-offs. The first part of the series was released in 1996.

Balatro, released on February 20th of this year, has already sold over a million copies. It took 10 days to reach the first half-million. Currently, the developers are working on a mobile version of the project.

Supersonic Studios' games have been downloaded over 5 billion times. Over four years, the studio has released more than 100 projects. The most popular among them is Bridge Race.

The CEO of Moon Studios, the developer of the Ori duology, reported on the cumulative sales of the series. The projects have over 10 million sales across all platforms.

Capcom reported 25 million copies sold of Monster Hunter World. This figure includes sales of the Iceborne expansion (about 4.5 million copies sold by the end of December). In total, the series has nearly 100 million sales.

The number of players in Sea of Stars has exceeded 5 million. These are not sales, as the game was distributed for free on PlayStation Plus. In celebration of this milestone, the developers announced a cooperative mode.

It took just over a year for Wo Long: Fallen Dynasty to reach 5 million players. The game was on Xbox Game Pass, so the figure doesn't equate to sales.

Deep Rock Galactic: Survivor surpassed 1 million copies sold in a month. The original Deep Rock Galactic took 3 years to sell 2 million copies.

Analyst Doug Creutz believes that sales of Helldivers II have exceeded 8 million copies. He stated this in an interview with Bloomberg.

Adjust & AppLovin: Mobile Game Market Trends in 2024

Adjust and AppLovin analyzed over 5,000 applications from January 2022 to January 2024 from various countries.

The report examines apps in general. I will focus on the gaming aspect.

Mobile advertising spending in 2023 increased by 8% to $362 billion.

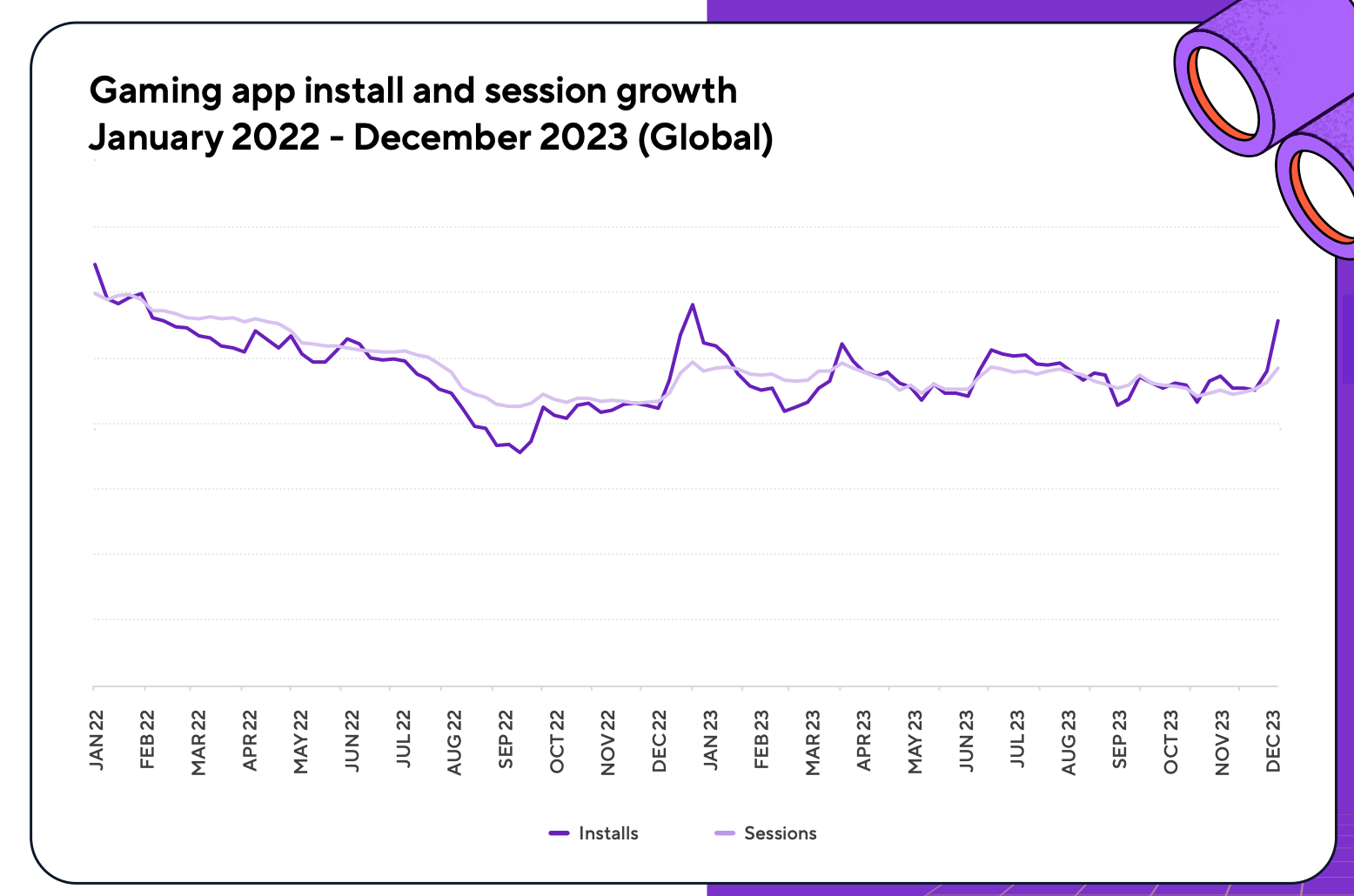

Mobile Games Results in 2023

Overall, downloads decreased by 2% throughout the year; the number of sessions decreased by 7%.

However, in the fourth quarter of 2023, there was a 7% increase in downloads YoY. Adjust and AppLovin believe this signals a return to market growth.

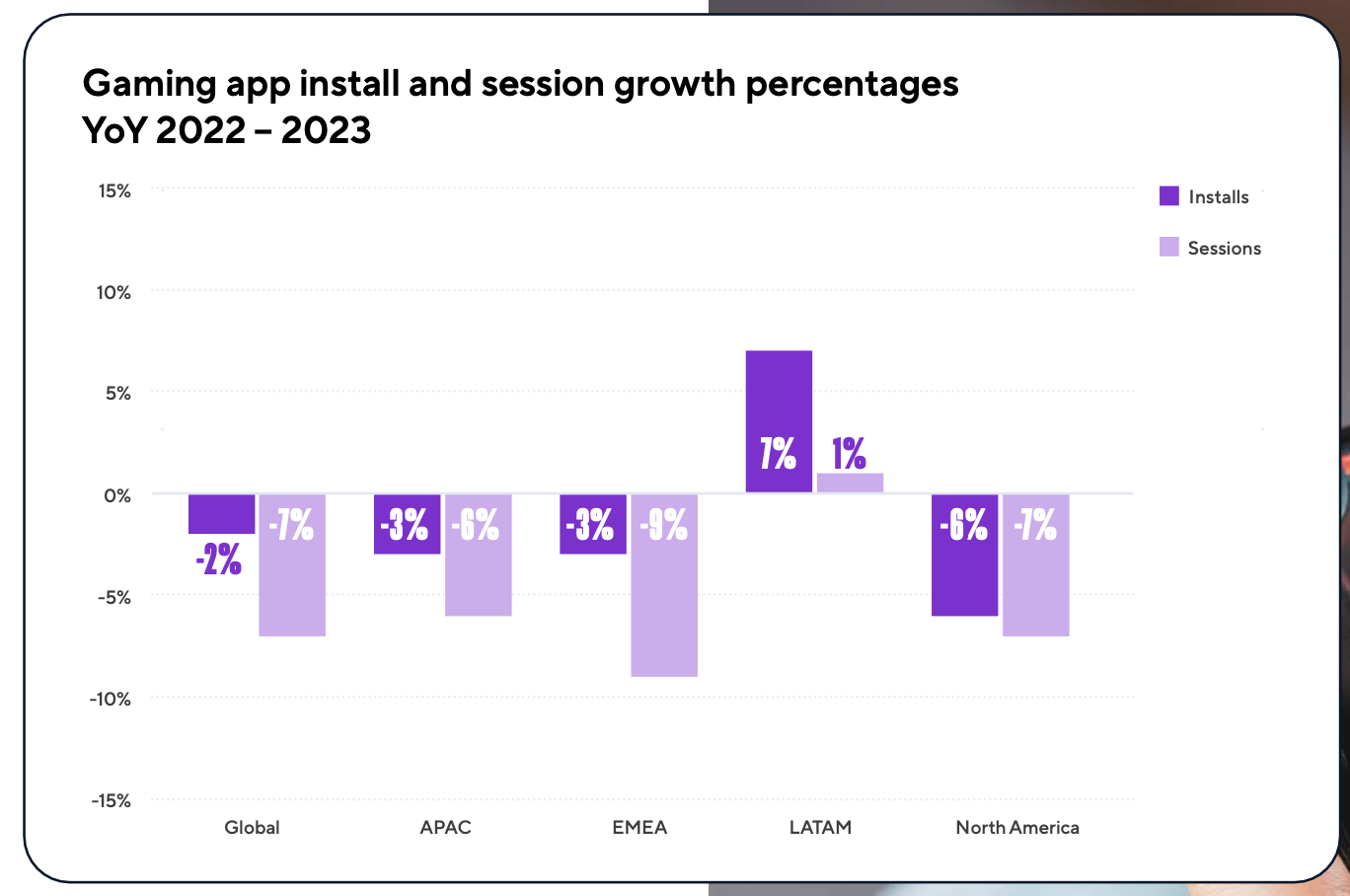

The only market that grew in 2023 in terms of both downloads (+7%) and the number of sessions (+1%) is LATAM.

Other markets are in negative territory. The North American region saw the sharpest decline in downloads (-6%); EMEA saw a decrease of 9% in the number of sessions.

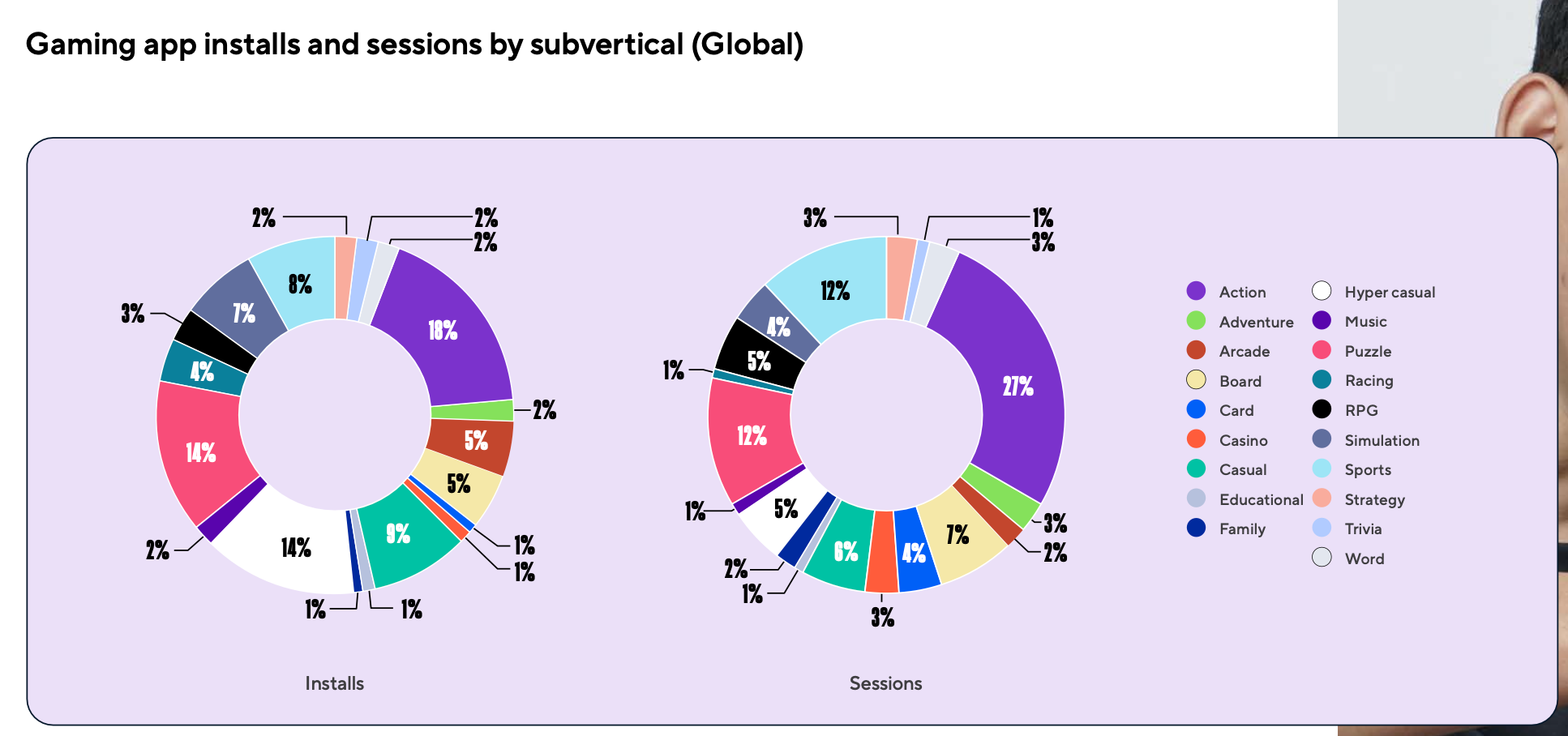

Most popular genres by Downloads and Sessions

Action games account for the highest number of downloads (18%). Hyper-casual projects (14%) and puzzles (14%) follow.

In terms of sessions, action games also lead (27%). Puzzles (12%) and sports projects (12%) have a significant percentage as well.

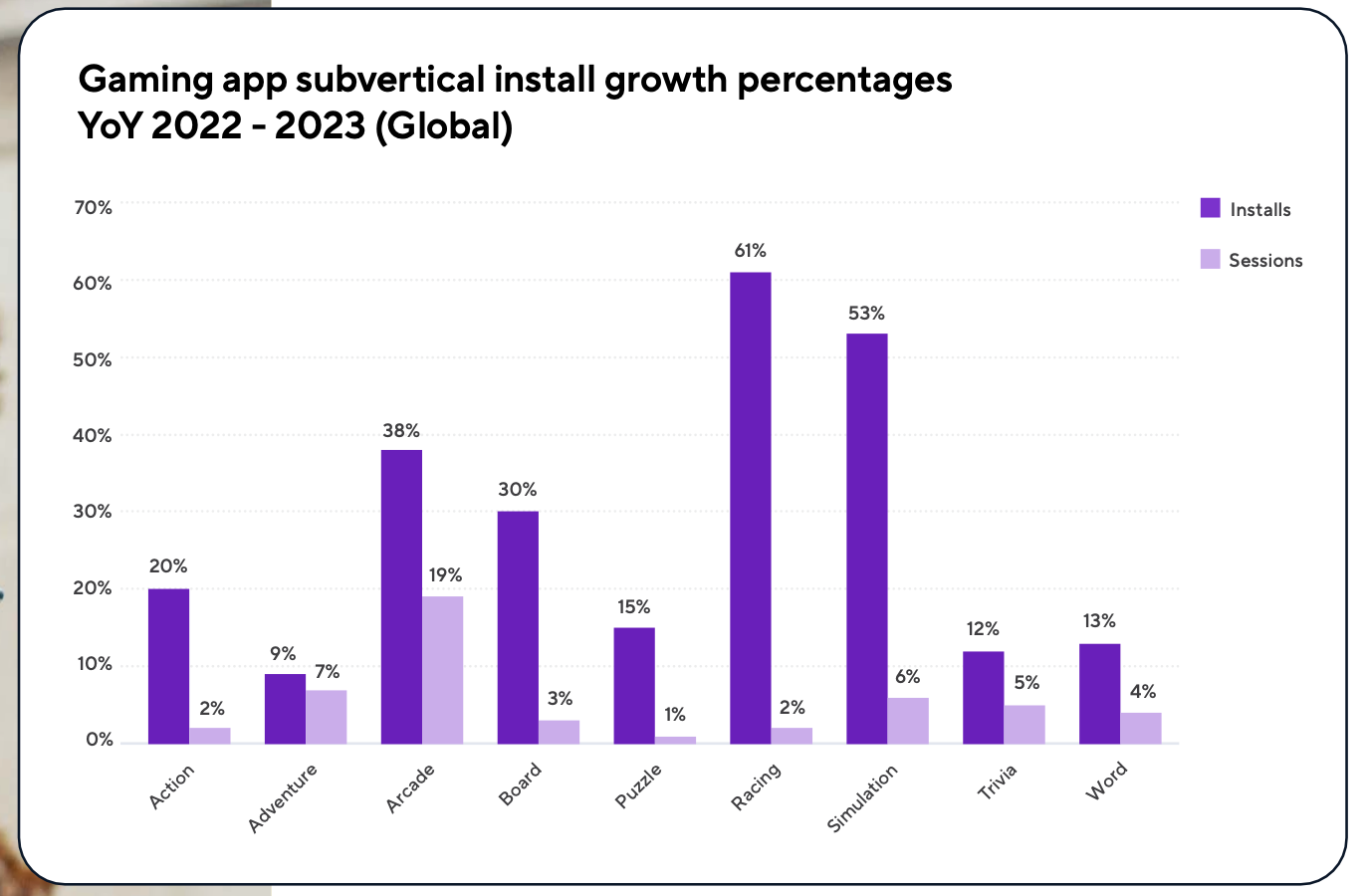

Growing genres

In 2023, racing games (+61%), Simulation genre (+53%), and arcades (+38%) showed the most significant growth in downloads.

The biggest increase in sessions was seen in arcade games (+19%), adventure games (+7%), and the Simulation genre (+6%).

Sessions in Mobile Games

Globally, the average session length in 2023 remained unchanged. However, looking at regions, it increased in the APAC region (from 35 to 36 minutes), while in other regions (EMEA, LATAM, North America), it slightly decreased.

In 2023, user engagement after installation declined. On the first day, the average number of sessions was 1.93; on the second day, it dropped to 0.63. Hyper-casual projects saw the most significant declines, while Simulation games retained their audience the best.

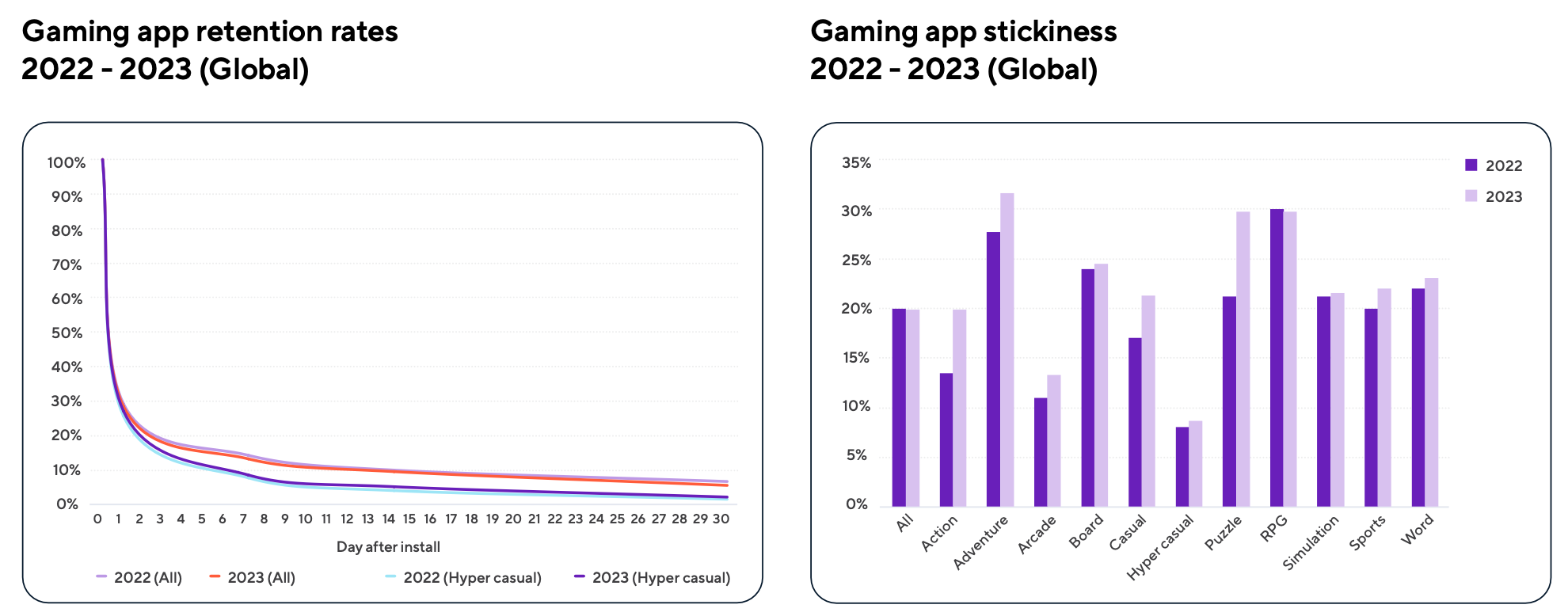

Retention benchmarks

Overall, Retention decreased slightly compared to 2022 figures.

D1 Retention dropped from 29% in 2022 to 28.3% in 2023. Average D7 Retention decreased from 14% (2022) to 13% (2023); D14 Retention - from 9.7% (2022) to 9.3% (2023); D30 Retention - from 6.4% (2022) to 5.3% (2023).

However, hyper-casual projects saw an opposite trend. Retention in them increased. D1 Retention rose from 26% (2022) to 27% (2023); D7 Retention - from 8% (2022) to 8.4% (2023); D14 Retention - from 4.3% (2022) to 5% (2023); D30 Retention - from 1.8% (2022) to 2% (2023). Perhaps the complication of meta-mechanics played a role.

Retention in many genres increased in 2023. The highest figures are seen in adventure games, RPGs, board, and word games.

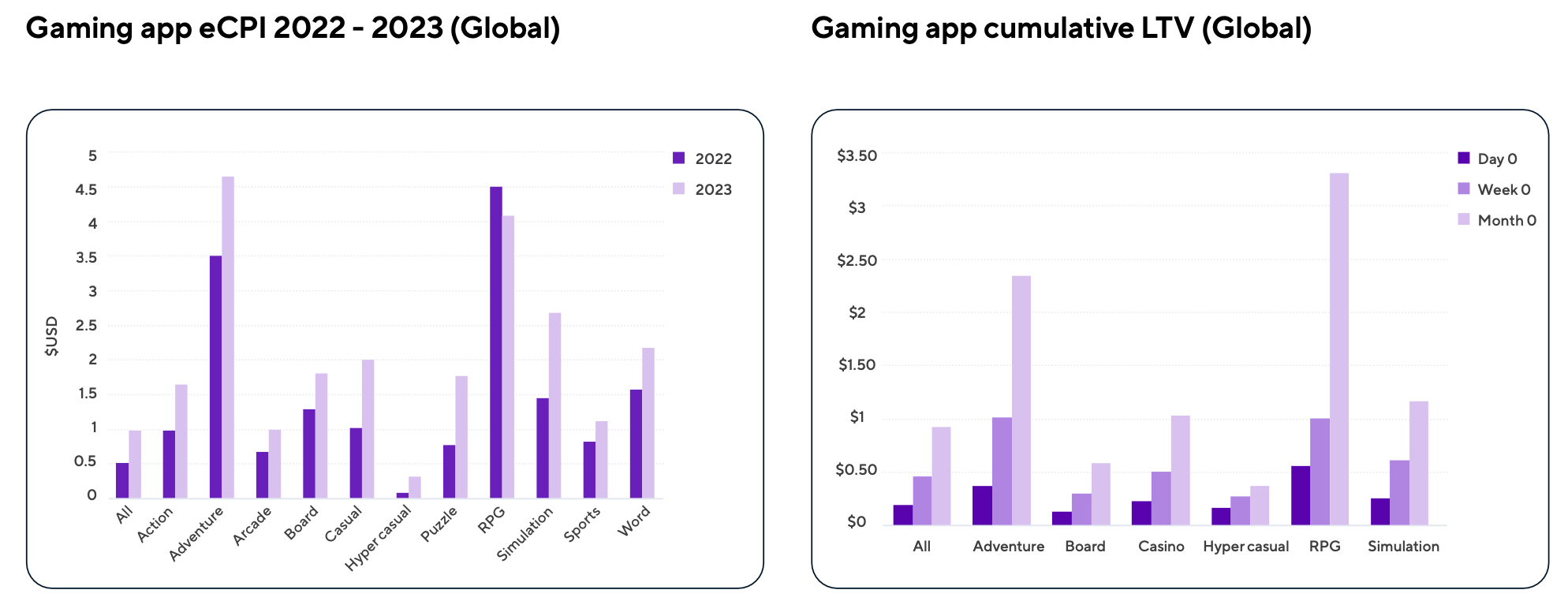

eCPI and LTV Trends

In almost all genres in 2023, eCPI increased. It only decreased among RPG projects (-$0.42). The highest growth was observed in the Simulation genre (+$1.23).

The highest average LTV is in RPGs ($3.31 after the first month); adventure games come second ($2.35). No genre breaks even in the first month when comparing eCPI and LTV.

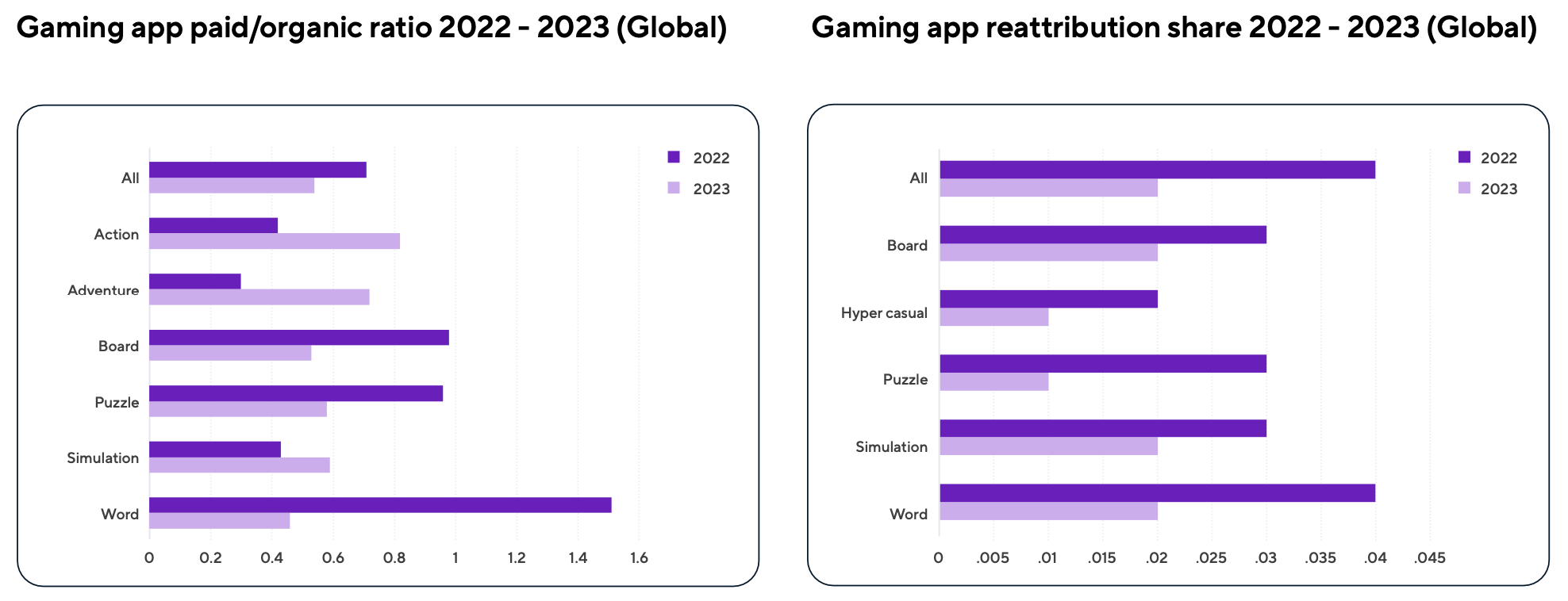

Organic and Paid Traffic

The overall ratio of organic traffic to paid traffic in 2023 significantly decreased - from 0.71 in 2022 to 0.54. This is especially noticeable in the Word genre, puzzles, and board games.

However, there are genres where organic traffic increased. These include action games (from 0.42 in 2022 to 0.82 in 2023) and adventure games (from 0.3 to 0.72).

Re-attribution in 2023 dropped from 0.04 (2022) to 0.02.

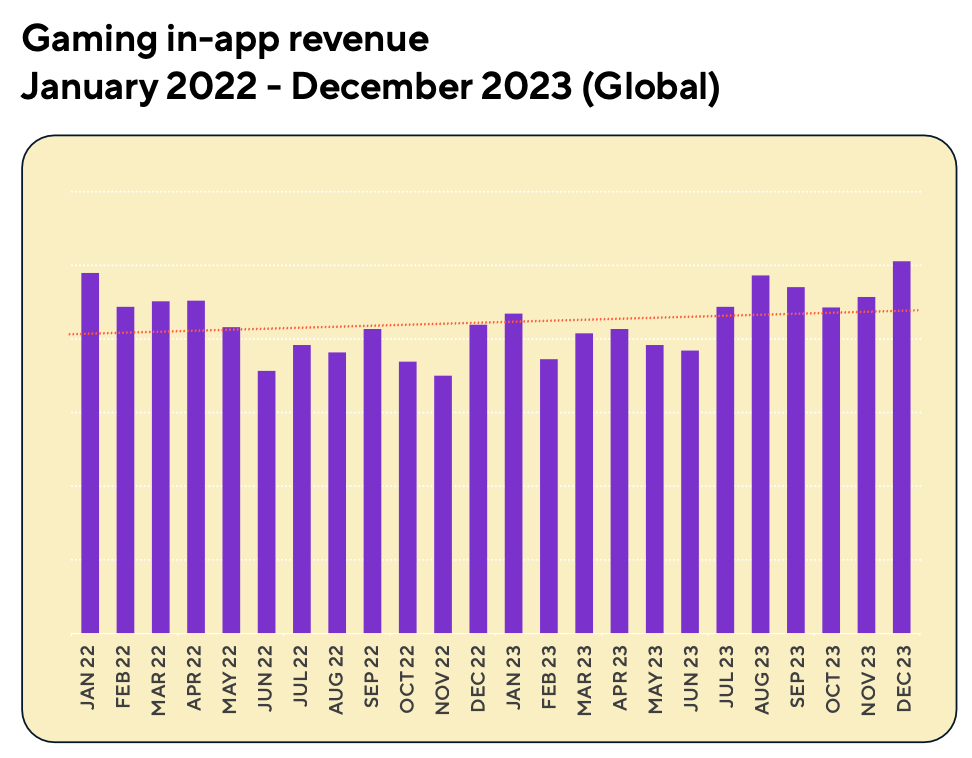

IAP Revenue in Mobile Games

According to Adjust and AppLovin data, by the end of 2023, mobile revenue from IAPs increased by 6% compared to 2022.

In December 2023, IAP revenue was 17% higher than the previous year.

ATT opt-in Rates

The ATT Opt-in rate in games rose to 39% in the first quarter of 2024. A year earlier, this figure was 36%.

This is the highest level among all applications. The market's average level is 32%.

DDM: Gaming Investments in Q4 2023; 2023 Results and 2024 Forecasts

Results for 2023 and Future Forecast

There are no companies too big for M&A deals. Activision Blizzard and Microsoft took 633 days from announcement to prove this. The deal amount - $68.7 billion.

Saudi Arabia's influence will continue to grow. Acquiring Scopely ($4.9 billion) and investing in VSPO ($265 million) is just the beginning.

Embracer Group has grown to a scale it couldn't sustain.

DDM expects the Chinese market to stagnate amid regulatory rhetoric from authorities.

In 2023, there were the highest number of undisclosed M&A (78%) and investment (28%) deals in history.

eSports is experiencing a crisis. The best demonstration is the purchase of FaZe Clan for $17 million. This is a company that went public through SPAC in July 2022 with a valuation of $725 million.

In 2023, there were 214 investment deals (-57% YoY) totaling $1.4 billion (-72% YoY) in blockchain projects. This is 35% of all gaming investments (-34% compared to 2022). FOMO among investors has ended.

AI is one of the few bright spots of 2023. There were 61 deals totaling $319 million (including a $54 million Series A round for Futureverse). DDM expects sustained interest in AI startups, albeit less explosive than in Web 3 projects.

Since 2020, Poland has had 34 gaming IPOs - three times more than in the US. In 2023, there was only one IPO through SPAC - MultiMetaVerse merged with Model Performance Acquisition Corp.

Accelerators are playing a more significant role in the gaming ecosystem. For example, Speedrun from Andreessen Horowitz invested $500,000 checks in 32 companies.

Companies are becoming interested in Africa, as evidenced by deals with 24 Bit Games and eSports provider Galactech.

Australia wants to compete globally. In 2023, there was a 217% increase in investments in local companies. The government awarded 35 grants to local studios.

Fortnite, Minecraft, Roblox, and UGC continue to grow and attract investor interest. The most notable transactions are Gamefam ($16.5 million); Pahdo Labs ($15 million) and Melon ($3.3 million).

Rockstar Games acquired RP server developer FiveM and RedM - Cfx.re company. Everyone expects Grand Theft Auto VI to feature an RP mode in multiplayer.

2023 Results in Numbers

Overall Results

In 2023, there were 787 deals totaling $81.1 billion. The deal between Microsoft and Activision Blizzard accounts for 85% of the total volume in 2023.

Private investment totaled $4.4 billion in 2023 (-69% YoY) through 616 transactions (-35% YoY). However, in terms of the number of deals, the result was better than pandemic-ridden 2020.

Excluding the Microsoft-Activision Blizzard deal, the volume of M&A transactions in 2023 was $8 billion. There were a total of 146 transactions. This is the lowest figure since 2019.

12 companies went public in 2023, with a total valuation of $619.3 million (-60% YoY). This is the lowest figure since 2016.

In 2023, there were 415 deals with game developers (-57% YoY) totaling $2.2 billion (-72% YoY). This is excluding M&A and IPOs. Despite the decline, the share of deals with developer studios in 2023 increased to 67% of the total private investment volume. The previous record was in 2013 (63.5%).

In 2023, 119 funds (-20% YoY) announced raising funds totaling $45.4 billion (-54% YoY).

Private Investments

In the second half of 2023, there were 270 venture investment deals totaling $2.1 billion. This is 4% less in volume and 22% less in quantity compared to the first half.

DDM expects venture investment activity in 2024 to remain at 2023 levels.

Saudi PIF still has over 75% of unallocated capital. It is expected that the company will continue to actively deploy funds.

Large Chinese companies will continue to try to gain a foothold in the West against the backdrop of regulating the local market.

The crypto winter is over, so an increase in venture activity in blockchain can be expected in 2024.

M&A and IPO

In the second half, the volume of M&A deals amounted to $76 billion (73 deals). Of course, this includes the acquisition of Activision Blizzard for $68.7 billion.

The trend of layoffs will continue in 2024, including from large companies. ByteDance, Epic Games, Unity have already started.

There will be more opportunities for cheap M&A deals on the market as independent companies find it difficult to stay in the market.

The IPO market is stable - 3 transactions per quarter, most of which are on the Polish market. The boom seen in 2020-2021 will not return for a long time.

Q4 2023 Results - Private Investments

In Q4 2023, there were 119 deals (-21% compared to Q3) totaling $936.6 million (-22% compared to Q3). This is the first quarter since Q3 2018 when the volume of venture investments in games was less than $1 billion.

33% of the volume went to mobile startups; 20% to MGC (a segment DDM allocates to multiplayer projects, including metaverse projects); 18% to tech startups; 15% to AR/VR; 11% to PC and consoles; 4% to eSports.

In terms of the number of venture deals, 30% went to mobile; 25% to tech startups; 14% to PC/console studios; 13% to eSports; 9% to MGC; 8% to AR/VR; 1% to browser projects.

In the fourth quarter, there were 29 undisclosed venture deals (24% of the total). The average for previous periods is 17%.

Q4 2023 Results - M&A

The deal volume amounted to $69.9 billion. Excluding the Activision Blizzard deal - $1.2 billion. There were 42 transactions (41 without AB). This is an 80% decrease in volume compared to Q4 2022.

The valuation of companies went public was $112 million (+257% YoY).

GSD & GfK: The European Gaming Market Actually Grew in February 2024

Analytical platforms report only actual sales figures obtained directly from partners. The mobile segment is also not taken into account.

Game Sales

In February of this year, 16.74 million games were sold on PC and consoles in Europe. In fact, this is a growth of 21.2% compared to February 2023, but this year February had 5 weeks of sales. Comparing equivalent periods, game sales in 2024 dropped by 0.1%.

In February of last year, Hogwarts Legacy was released; its sales in just 5 weeks after release were higher than the sales of the entire top 10 games in February 2024.

It is worth noting that Palworld is not included in sales figures. Therefore, February 2024 could have been better than February 2023.

Helldivers II was the top hit of the month. 56% of the project's sales came from PC. The project has an interesting sales dynamic, quite atypical for a paid game. In the second week, it sold 70% better than the first. And in the third week, it sold 3% better than the second. Only in the fourth week did sales drop by 28% compared to the third week.

For most paid projects, sales in the second week are 60-80% lower than in the first.

Helldivers II sales for the first 4 weeks are only 5% behind Marvel’s Spider-Man II. The latter, however, was only available on PS5 and sold at a higher price.

EA Sports FC 24 takes the second position; the game sells well.

Final Fantasy VII: Rebirth climbed to the 3rd position on the chart. But its sales are 23% worse than the first part of the remake. And if compared to last year's Final Fantasy XVI, sales are 4% better.

Skull and Bones debuted at the 9th position. Its sales after the first 3 weeks are 30% worse than Sea of Thieves, released in March 2018.

Suicide Squad: Kill the Justice League didn't even make it to the top 10; it's at the 12th position. After the first 5 weeks, it sells 33% worse than Gotham Knights and 61% worse than Guardians of the Galaxy.

Console Sales

GSD does not take into account console sales in Germany and the United Kingdom.

In February, just over 474 thousand consoles were sold in Europe. This is actually 11% more than the previous month, but if compared weekly, sales dropped by 14%.

PS5 dropped slightly - by 2% YoY. Nintendo Switch suffered greater losses - -17% YoY; Xbox Series S|X suffered the most - its sales dropped by 47%.

In February 2024, 1.6 million accessories were sold. The best-selling ones were DualSense and Xbox Wireless Controller.