Adjust & AppLovin: Mobile Game Market Trends in 2024

A big report with various benchmarks on sessions; retention; eCPI; LTV; and many other things.

Adjust and AppLovin analyzed over 5,000 applications from January 2022 to January 2024 from various countries.

The report examines apps in general. I will focus on the gaming aspect.

Mobile advertising spending in 2023 increased by 8% to $362 billion.

Mobile Games Results in 2023

Overall, downloads decreased by 2% throughout the year; the number of sessions decreased by 7%.

However, in the fourth quarter of 2023, there was a 7% increase in downloads YoY. Adjust and AppLovin believe this signals a return to market growth.

The only market that grew in 2023 in terms of both downloads (+7%) and the number of sessions (+1%) is LATAM.

Other markets are in negative territory. The North American region saw the sharpest decline in downloads (-6%); EMEA saw a decrease of 9% in the number of sessions.

Most popular genres by Downloads and Sessions

Action games account for the highest number of downloads (18%). Hyper-casual projects (14%) and puzzles (14%) follow.

In terms of sessions, action games also lead (27%). Puzzles (12%) and sports projects (12%) have a significant percentage as well.

Growing genres

In 2023, racing games (+61%), Simulation genre (+53%), and arcades (+38%) showed the most significant growth in downloads.

The biggest increase in sessions was seen in arcade games (+19%), adventure games (+7%), and the Simulation genre (+6%).

Sessions in Mobile Games

Globally, the average session length in 2023 remained unchanged. However, looking at regions, it increased in the APAC region (from 35 to 36 minutes), while in other regions (EMEA, LATAM, North America), it slightly decreased.

In 2023, user engagement after installation declined. On the first day, the average number of sessions was 1.93; on the second day, it dropped to 0.63. Hyper-casual projects saw the most significant declines, while Simulation games retained their audience the best.

Retention benchmarks

Overall, Retention decreased slightly compared to 2022 figures.

D1 Retention dropped from 29% in 2022 to 28.3% in 2023. Average D7 Retention decreased from 14% (2022) to 13% (2023); D14 Retention - from 9.7% (2022) to 9.3% (2023); D30 Retention - from 6.4% (2022) to 5.3% (2023).

However, hyper-casual projects saw an opposite trend. Retention in them increased. D1 Retention rose from 26% (2022) to 27% (2023); D7 Retention - from 8% (2022) to 8.4% (2023); D14 Retention - from 4.3% (2022) to 5% (2023); D30 Retention - from 1.8% (2022) to 2% (2023). Perhaps the complication of meta-mechanics played a role.

Retention in many genres increased in 2023. The highest figures are seen in adventure games, RPGs, board, and word games.

eCPI and LTV Trends

In almost all genres in 2023, eCPI increased. It only decreased among RPG projects (-$0.42). The highest growth was observed in the Simulation genre (+$1.23).

The highest average LTV is in RPGs ($3.31 after the first month); adventure games come second ($2.35). No genre breaks even in the first month when comparing eCPI and LTV.

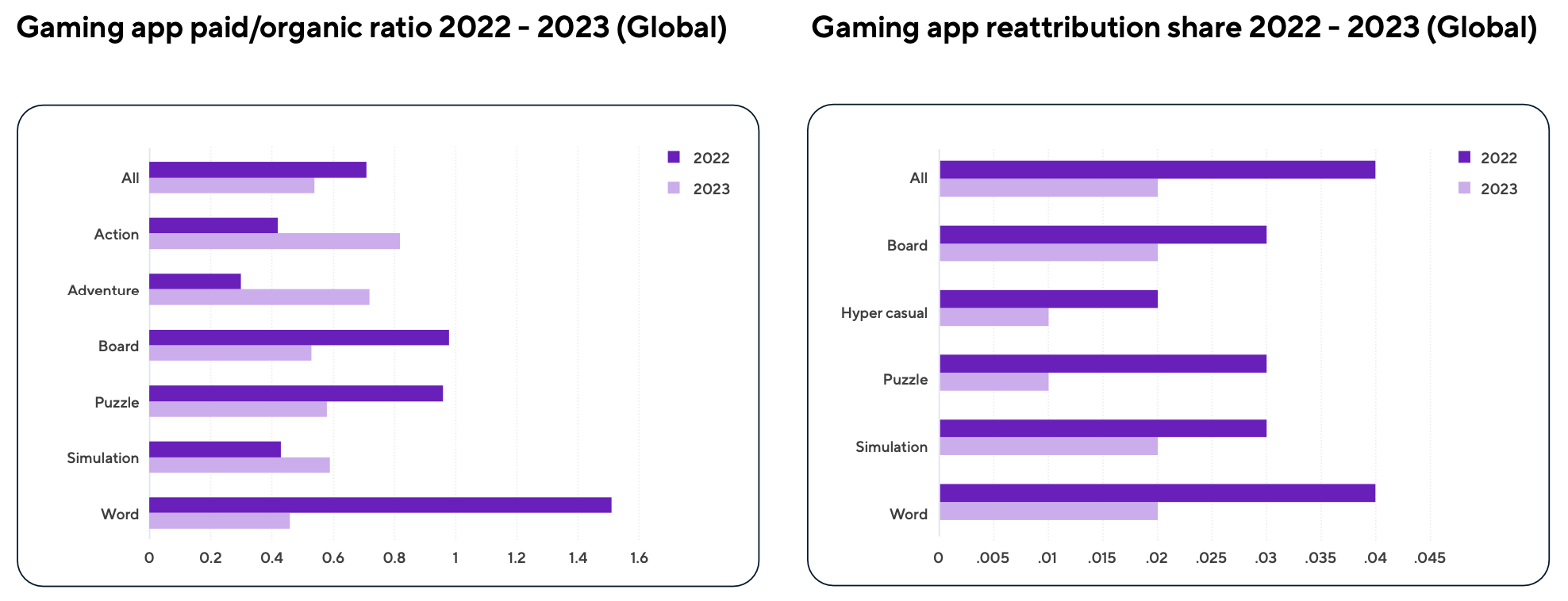

Organic and Paid Traffic

The overall ratio of organic traffic to paid traffic in 2023 significantly decreased - from 0.71 in 2022 to 0.54. This is especially noticeable in the Word genre, puzzles, and board games.

However, there are genres where organic traffic increased. These include action games (from 0.42 in 2022 to 0.82 in 2023) and adventure games (from 0.3 to 0.72).

Re-attribution in 2023 dropped from 0.04 (2022) to 0.02.

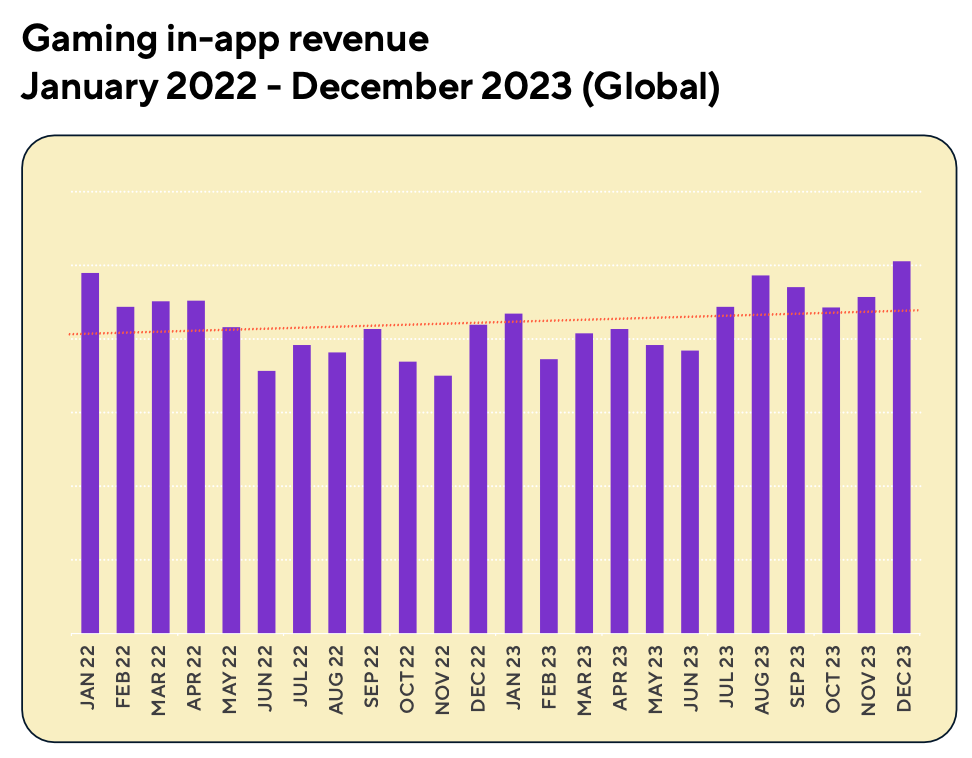

IAP Revenue in Mobile Games

According to Adjust and AppLovin data, by the end of 2023, mobile revenue from IAPs increased by 6% compared to 2022.

In December 2023, IAP revenue was 17% higher than the previous year.

ATT opt-in Rates

The ATT Opt-in rate in games rose to 39% in the first quarter of 2024. A year earlier, this figure was 36%.

This is the highest level among all applications. The market's average level is 32%.