AppMagic: Mobile Market Landscape in 2026

The report is covering both gaming & non-gaming apps performance in 2025.

State of the Mobile Market

This section covers both gaming and non-gaming applications.

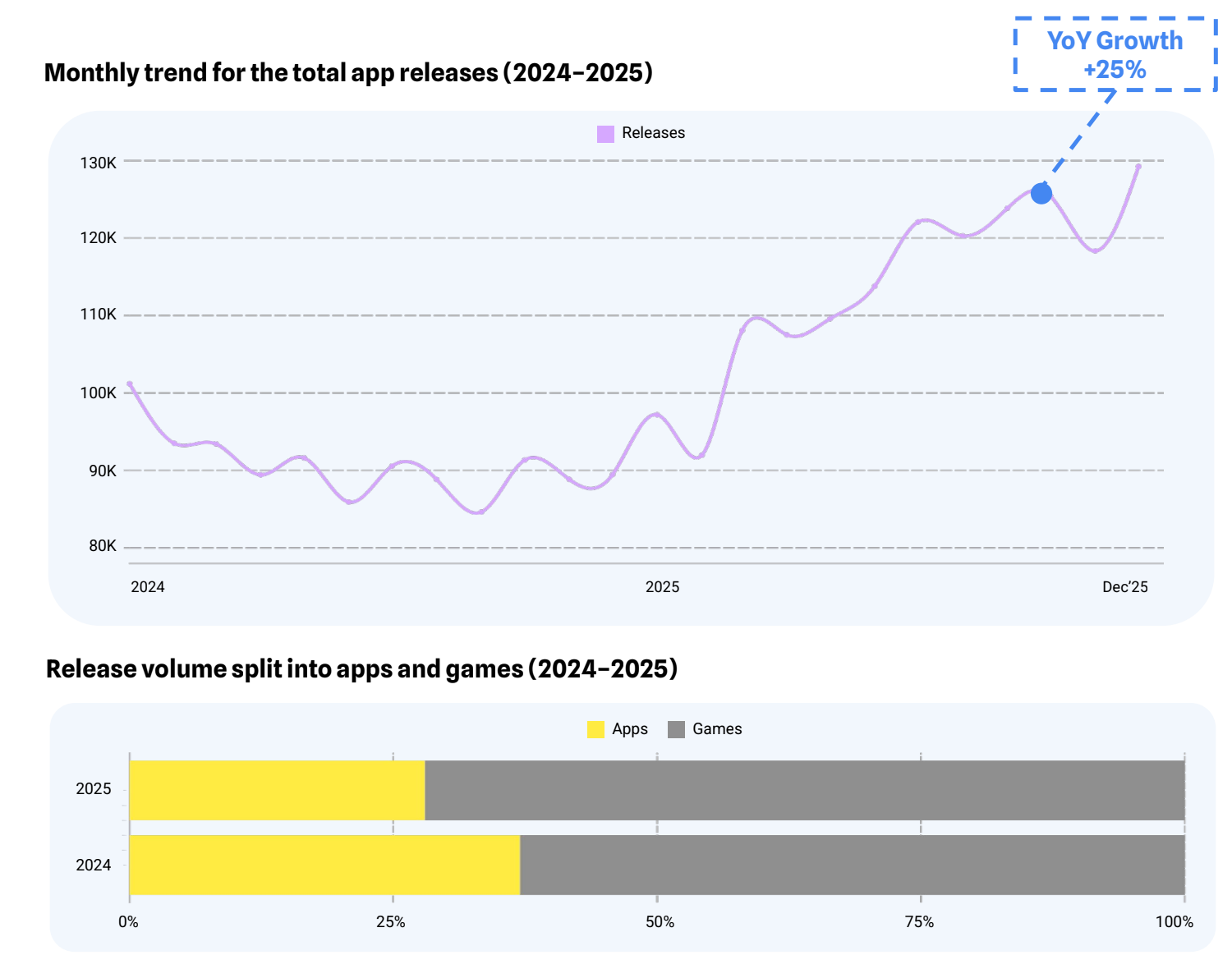

In 2025, 25% more apps were released than in 2024. At the same time, the share of games among new releases increased from 63% in 2024 to 72% in 2025 (competition intensifies!). In absolute terms, more than 1.4 million apps were released on Google Play and the App Store in 2025. Only 10% of them attracted any user attention.

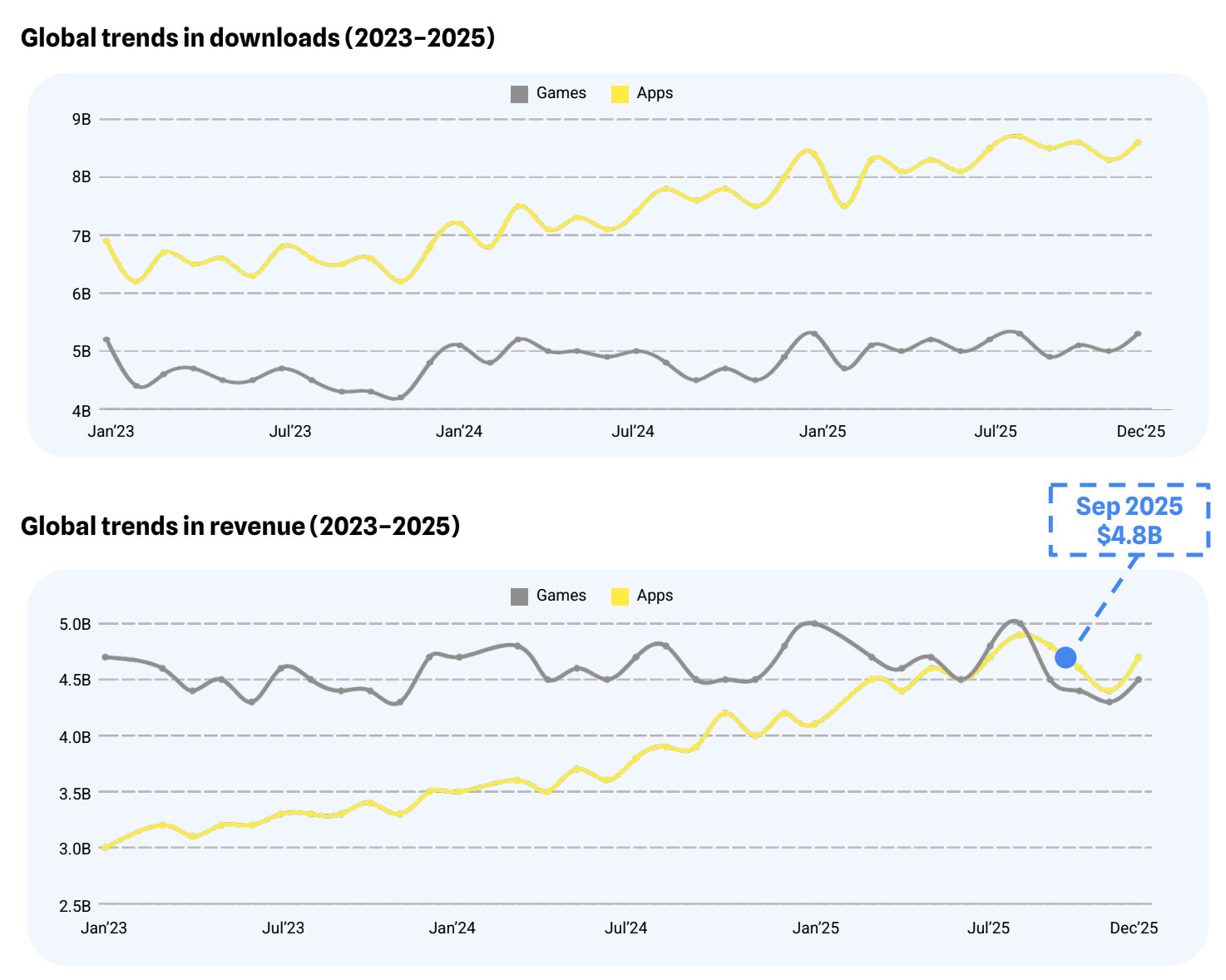

According to AppMagic’s methodology, non-gaming apps overtook games in IAP revenue in September 2025 ($4.8 billion vs. $4.5 billion). The biggest contributors to this were ChatGPT, TikTok, YouTube, Tinder, and HBO Max.

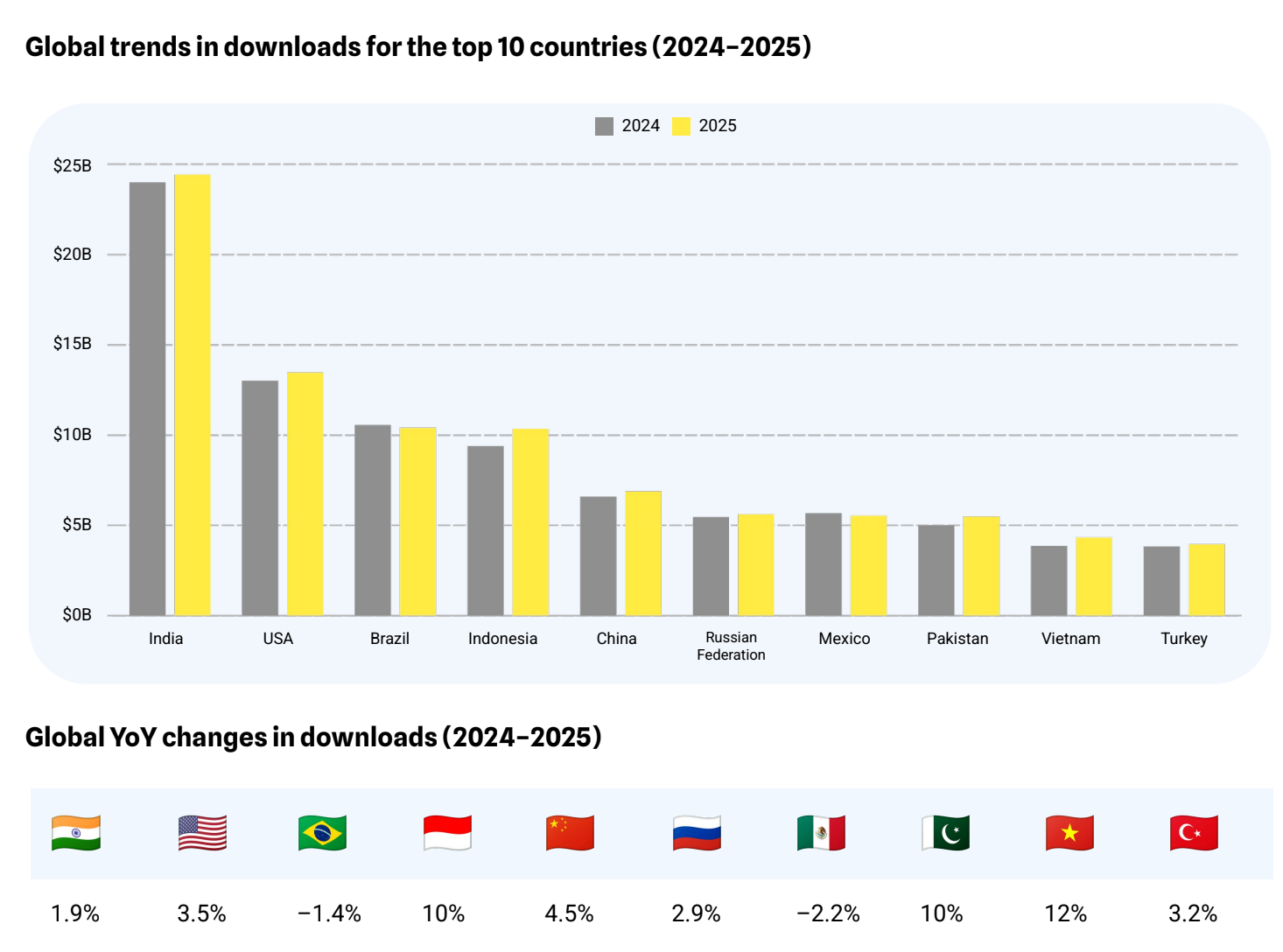

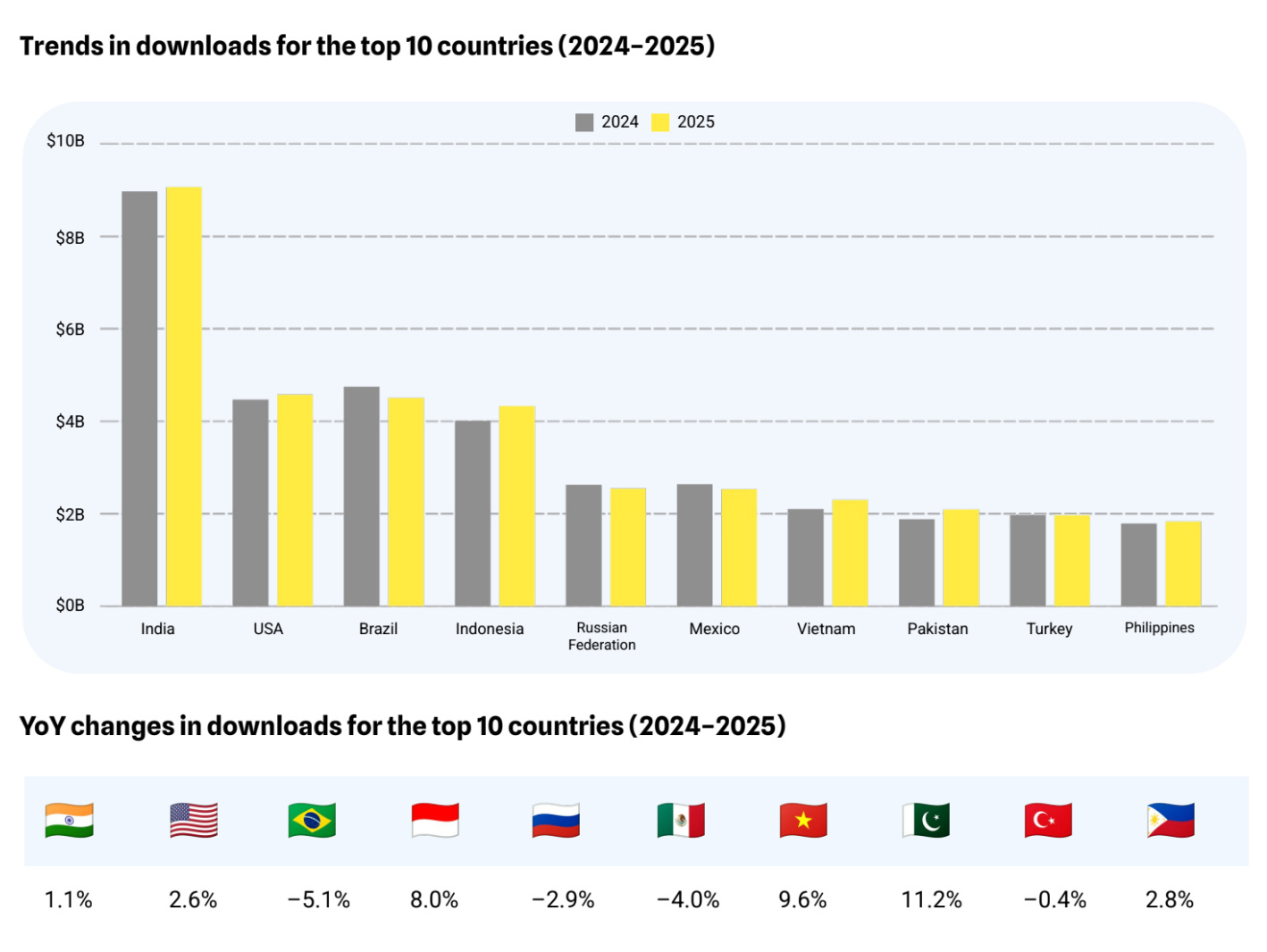

Indonesia is about to enter the top-3 countries by downloads. The country finished 2025 in 4th place with 10% YoY growth, only slightly behind Brazil (-1.4% YoY). The top two positions remain unchanged: India (+1.9% YoY) and the US (+3.5% YoY). Pakistan (+10% YoY) and Vietnam (+12% YoY) also showed rapid download growth.

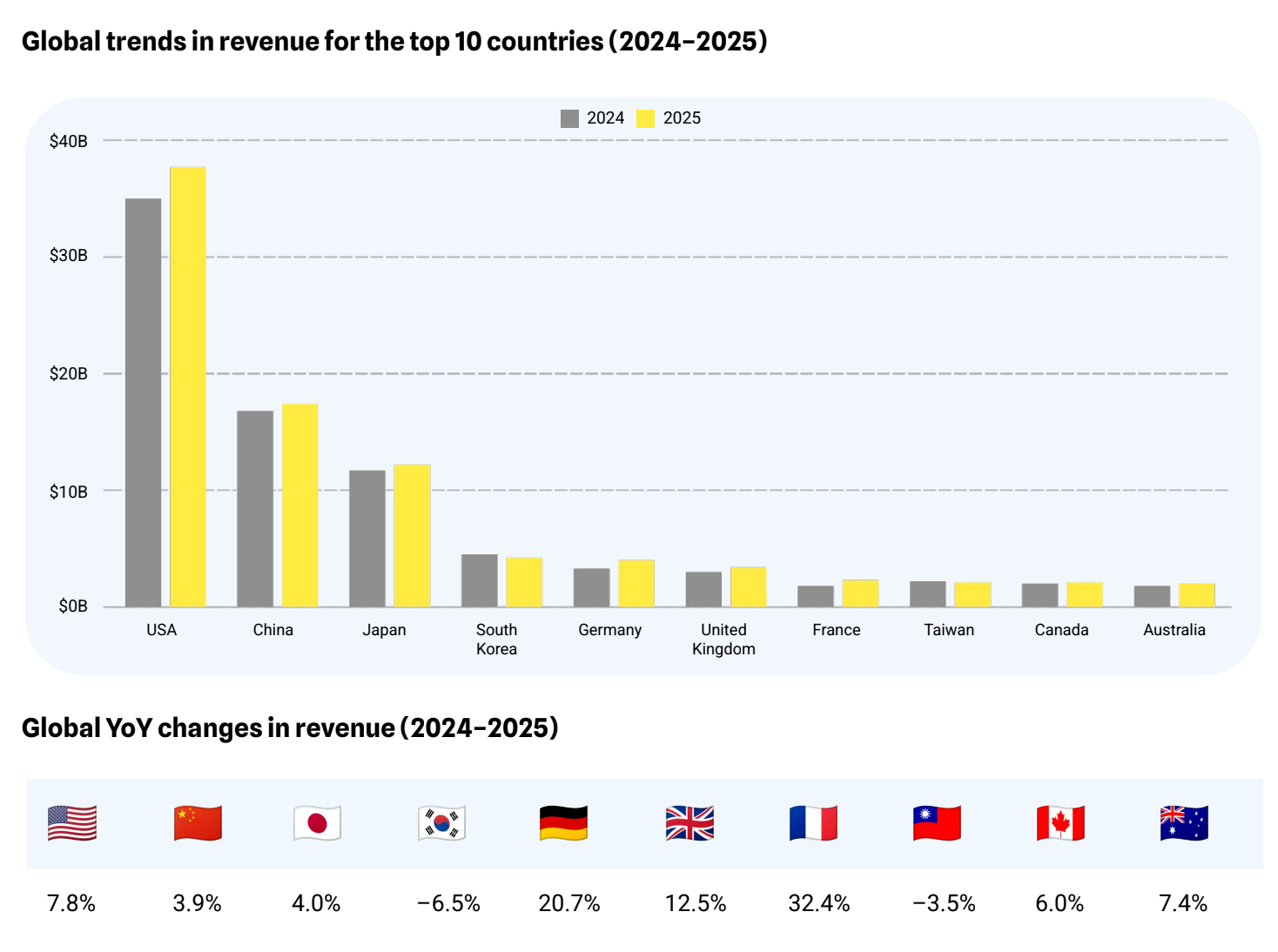

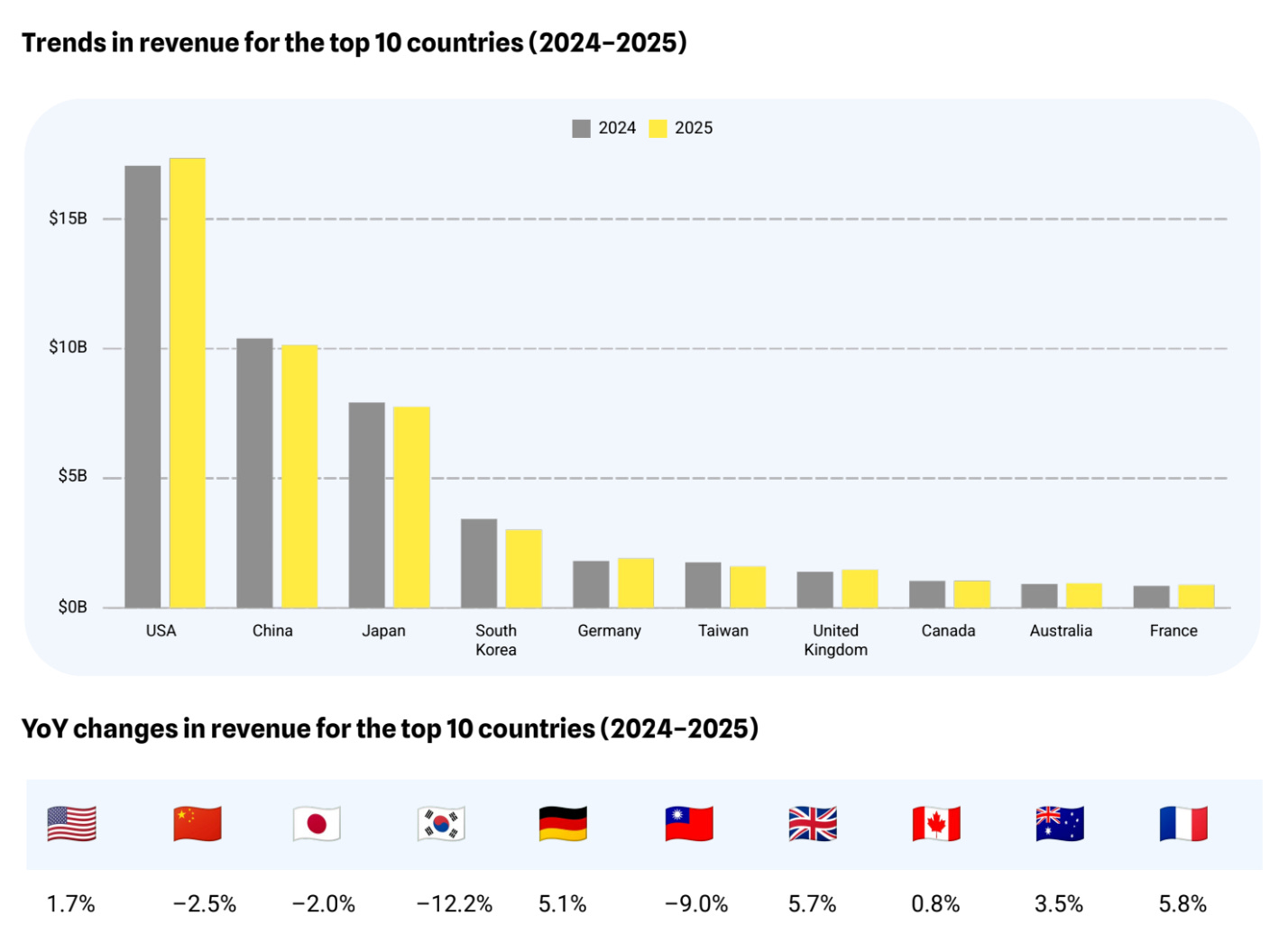

Looking at revenue trends, growth continues in the US (+7.8% YoY), China (+3.9% YoY, iOS only), and Japan (+4% YoY). Among the top-10 countries, only South Korea (-6.5% YoY) and Taiwan (-3.5% YoY) saw revenue declines.

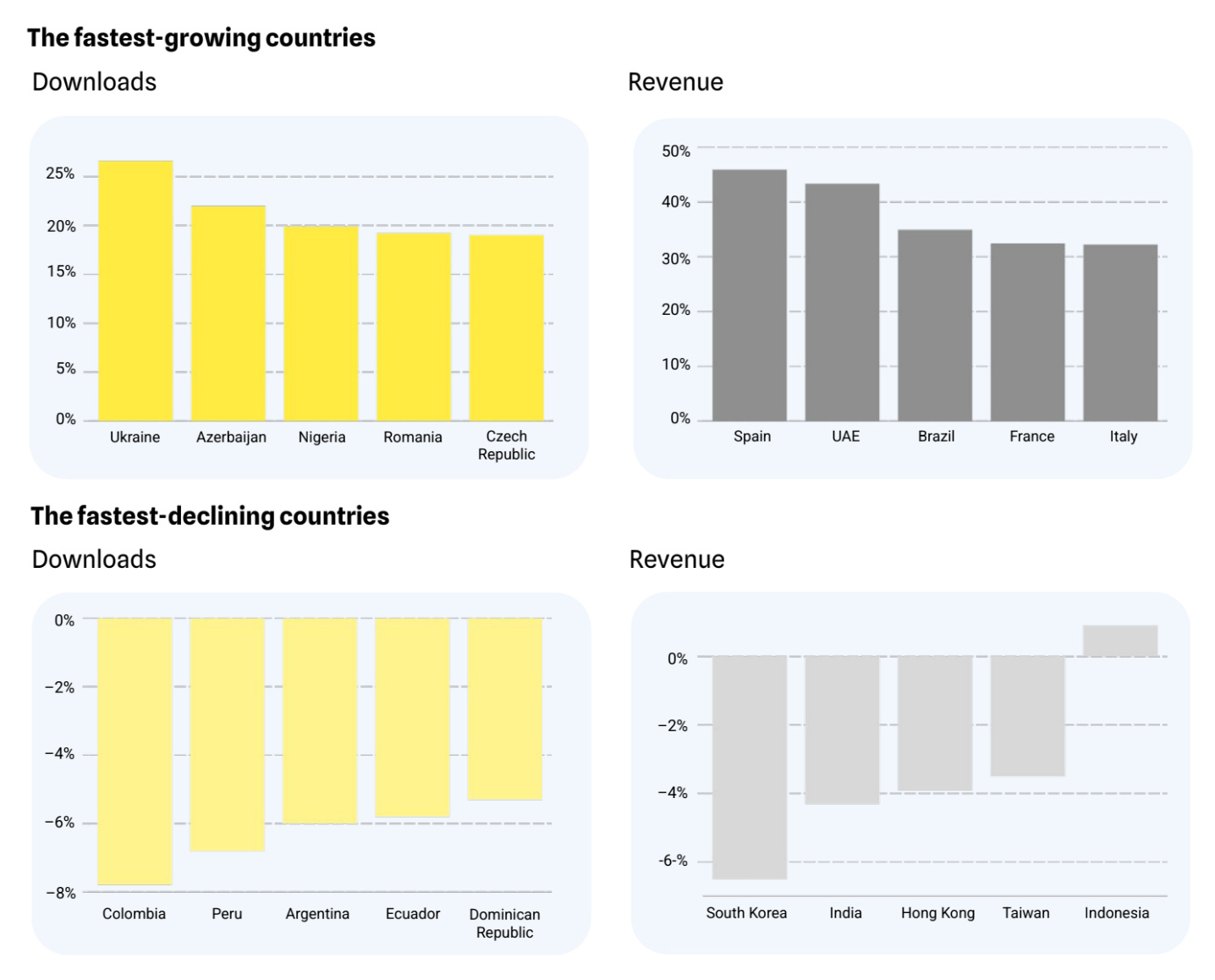

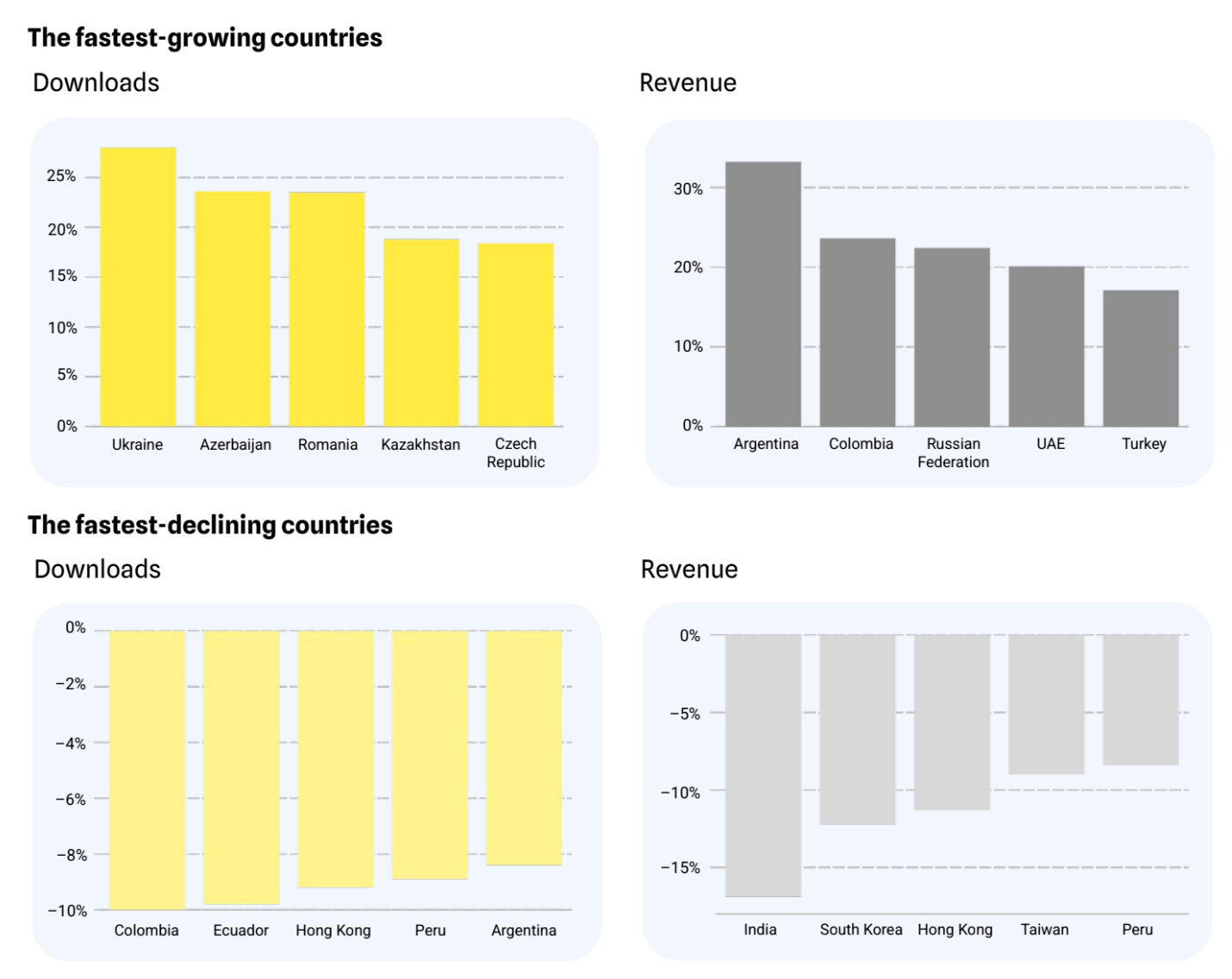

Ukraine, Azerbaijan, Nigeria, Romania, and the Czech Republic were the leaders in download growth in 2025. Revenue growth leaders were Spain, the UAE, Brazil, France, and Italy.

The sharpest download decline was observed in Colombia, Peru, Argentina, Ecuador, and the Dominican Republic. Revenue declined most in South Korea, India, Hong Kong, and Taiwan. AppMagic believes that Latin American markets have reached saturation, and future growth will be driven more by an increase in paying users than by audience growth.

💬 Roman Garbar, Marketing Director at Tenjin, believes that the decline in downloads in LATAM may be linked to reduced UA spend in 2025. Companies may have set overly optimistic expectations for eCPM and IAP revenue and, failing to reach them, reduced investments in the region.

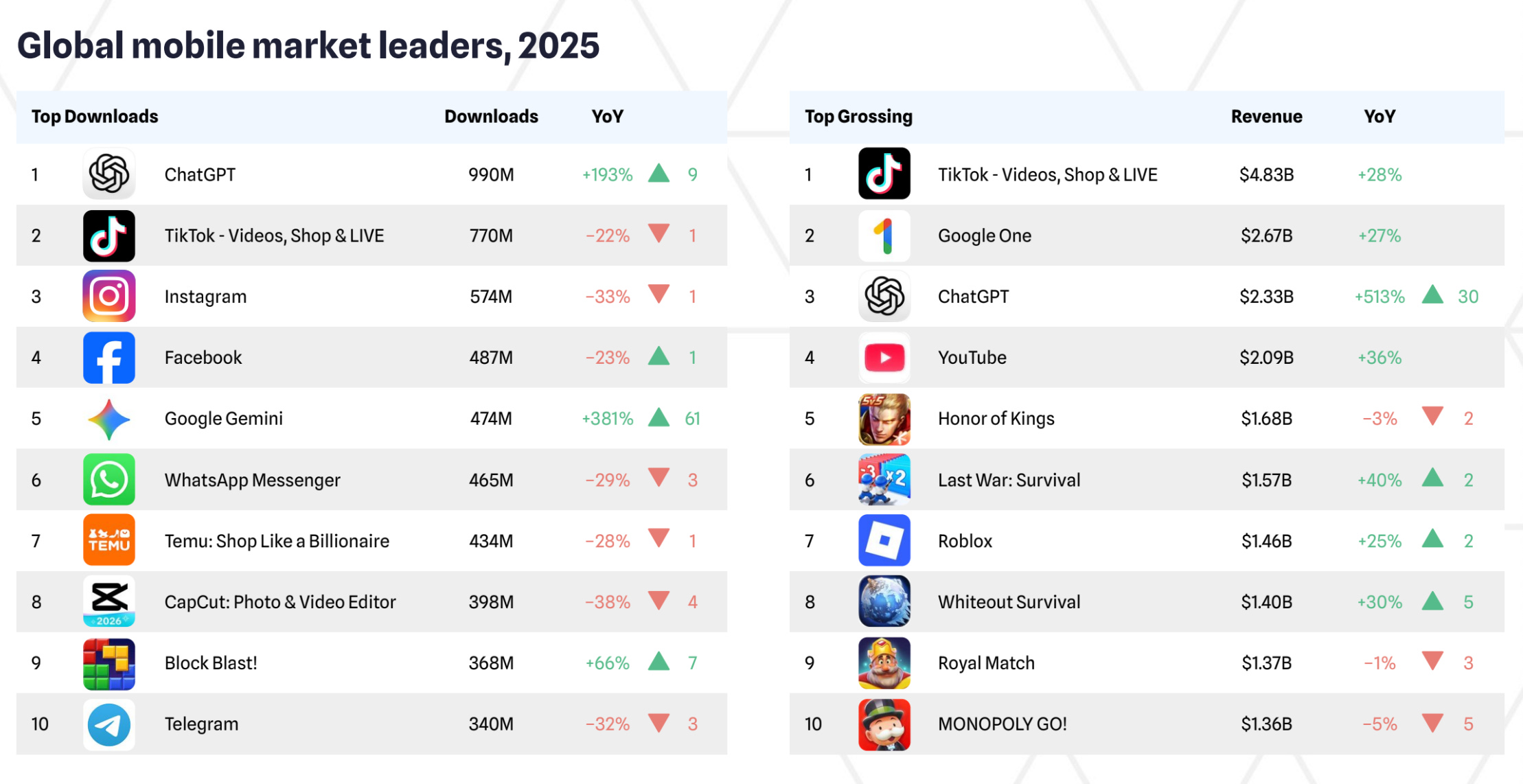

Only one game topped the 2025 downloads chart: Block Blast! (368 million installs, +66% YoY).

There are more games than non-gaming apps in the top-10 by revenue, but they are in the lower part of the list. Honor of Kings ($1.68 billion in revenue, -3% YoY) was the highest-grossing game of the year. The strongest revenue growth was shown by Last War: Survival ($1.57 billion in 2025, +40% YoY).

A word from our sponsor

Maximize your game’s global revenue with Xsolla’s Global Payments - offering seamless, localized checkout in multiple languages and integrating 1,000+ local payment methods to boost conversion rates.

Protect your income with advanced machine-learning anti-fraud, cross-game blocklisting, and 3DS 2.0, while Xsolla handles tax, compliance, support, refunds, and chargebacks for you. Deliver a smooth, secure payment experience optimized for all devices and expand your reach with confidence!

Make payments easy with Xsolla!

Mobile Gaming Market

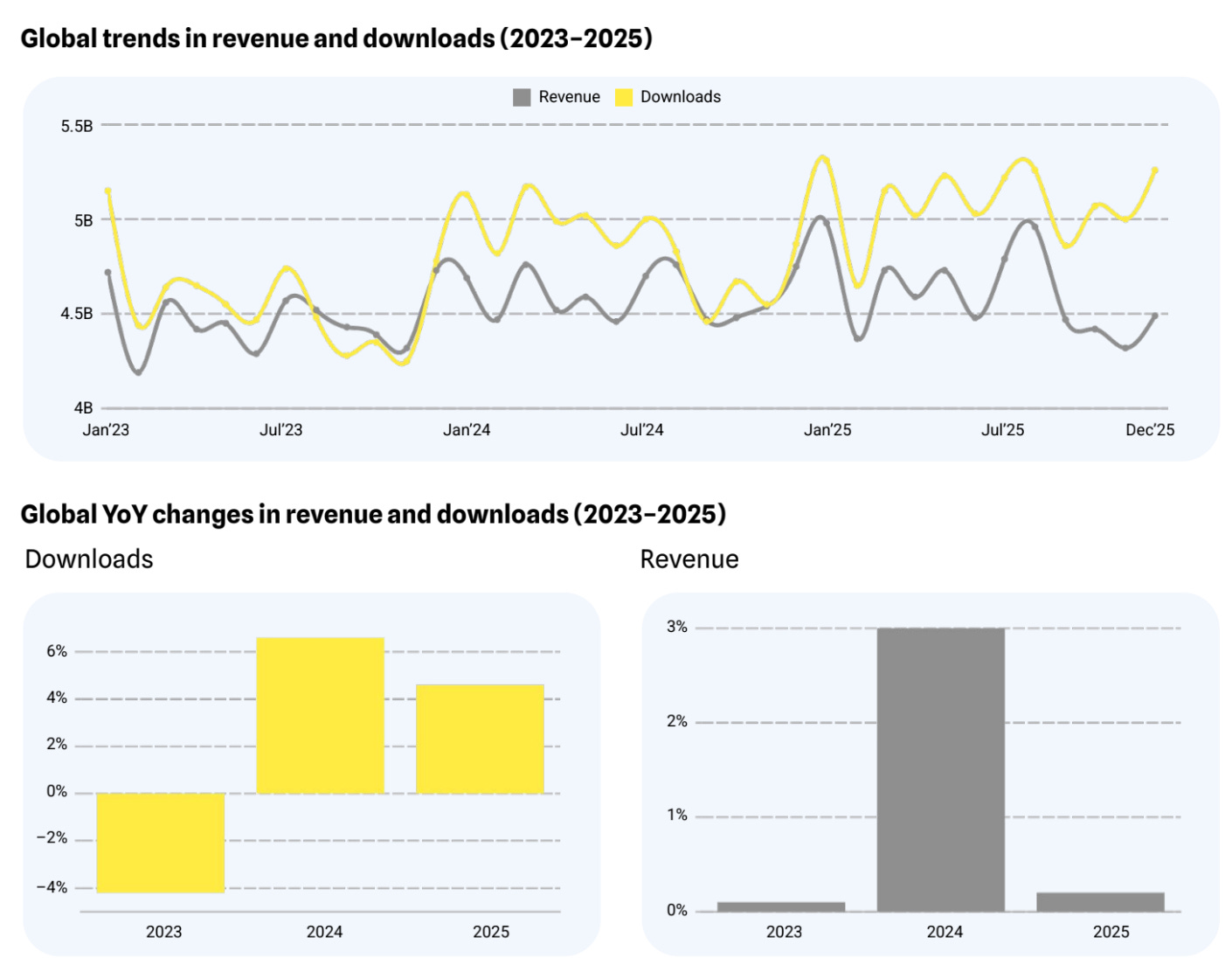

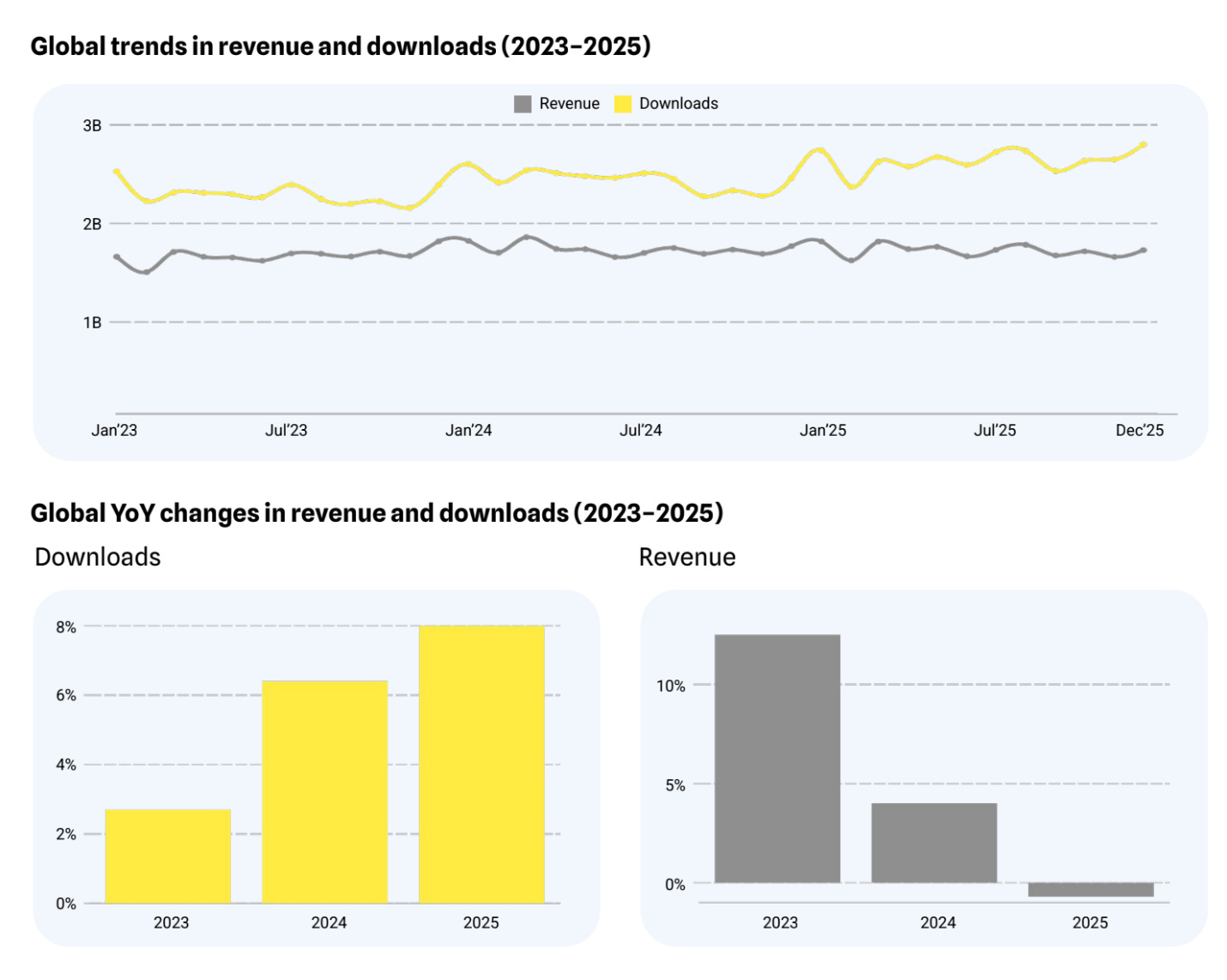

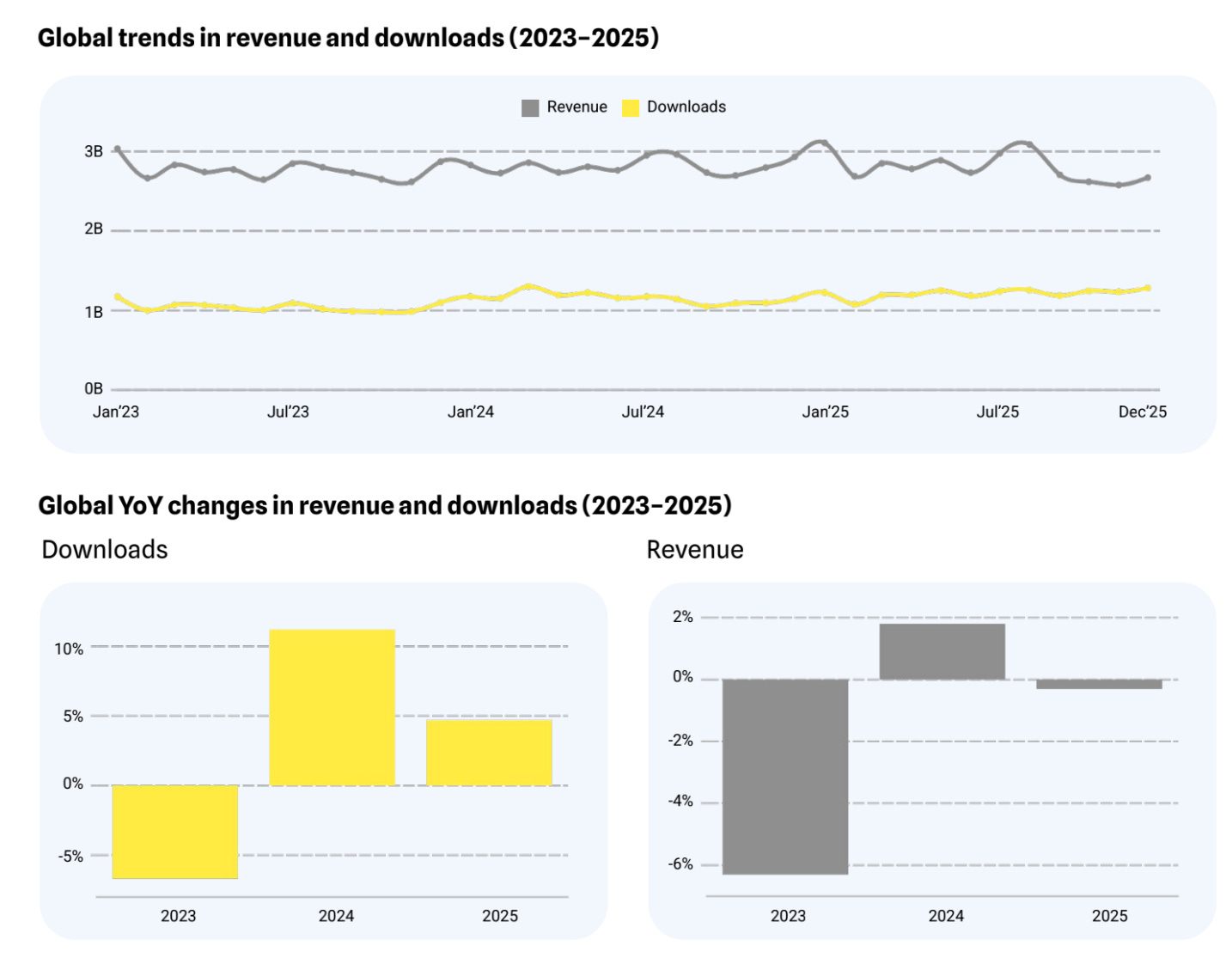

In 2025, the mobile gaming market grew by only 0.2%, according to AppMagic. In 2024, growth was 3%.

AppMagic observes download growth in both 2024 (+6.6% YoY) and 2025 (+4.6% YoY).

❗️These numbers differ from the situation described recently by Sensor Tower. According to their report, downloads have been declining since 2023, while revenue has been growing faster than AppMagic reports.

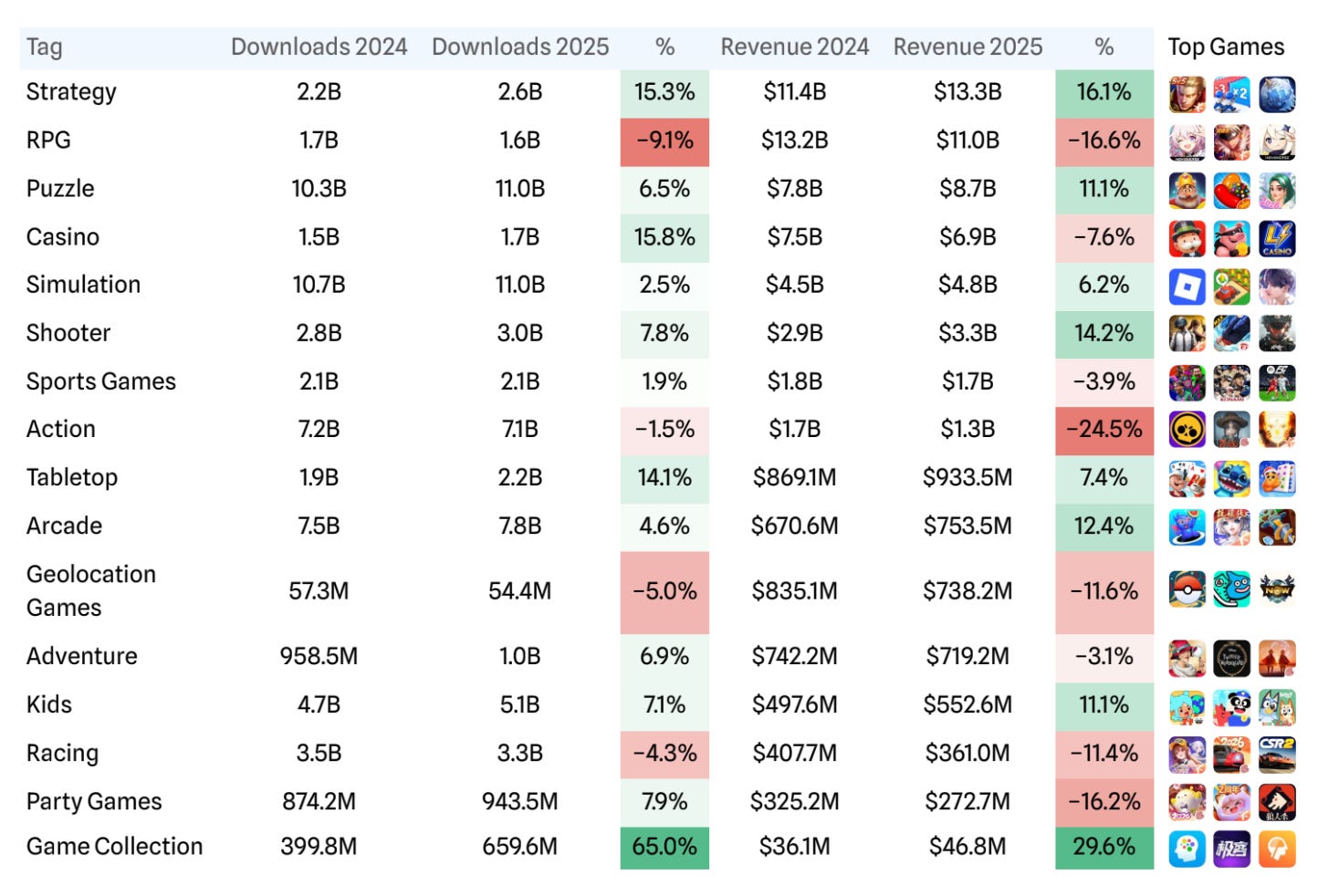

The steepest revenue declines in 2025 were recorded in action games (-24.5% YoY), RPGs (-16.6% YoY), party games (-16.2% YoY), geo-based games (-11.6% YoY), racing (-11.4% YoY), and casino (-7.6% YoY).

Growth was concentrated in Game Collection (+29.6% YoY), strategies (+16.1% YoY), and shooters (+14.2% YoY).

❗️Please, note that revenue here is shown excluding D2C payments. The real picture may differ.

India (+1.1% YoY), the US (+2.6% YoY), Brazil (-5.1% YoY), Indonesia (+8% YoY), and Russia (-2.9% YoY) were the top-5 countries by game downloads in 2025.

The US (+1.7% YoY), China (-2.5% YoY), Japan (-2% YoY), South Korea (-12.2% YoY), and Germany (+5.1% YoY) led by revenue in 2025.

Overall, Western markets showed the strongest revenue growth, especially in European countries.

The list of countries with the strongest growth and decline in game revenue and downloads largely overlaps with the chart for all apps above, but there are differences. For example, Kazakhstan entered the top countries by game install growth, while Argentina, Colombia, Russia, and Turkey appeared among the top countries by revenue growth.

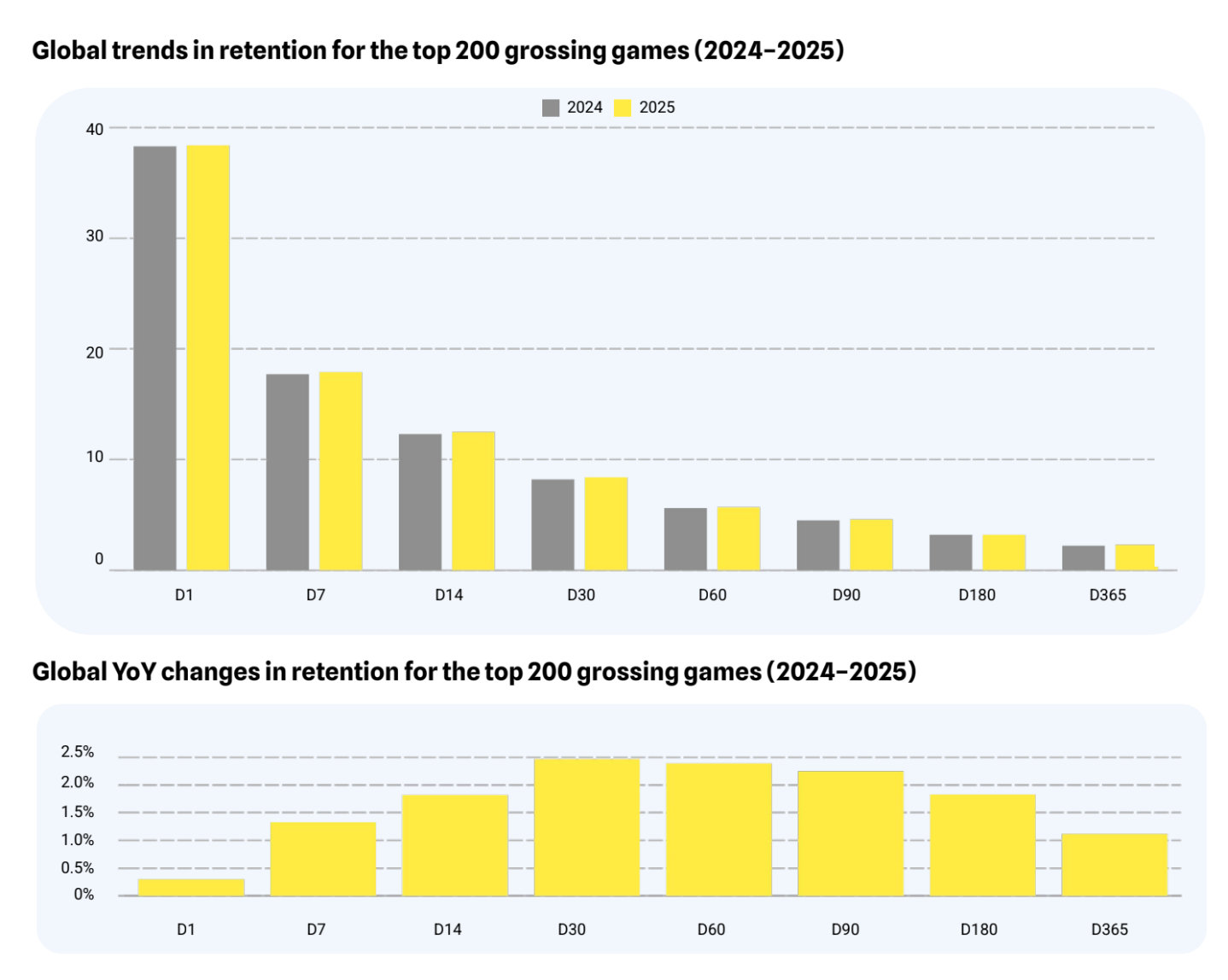

Overall retention trends for the top 200 games in 2025 remained largely unchanged. D14–D60 retention increased slightly by a couple of percentage points.

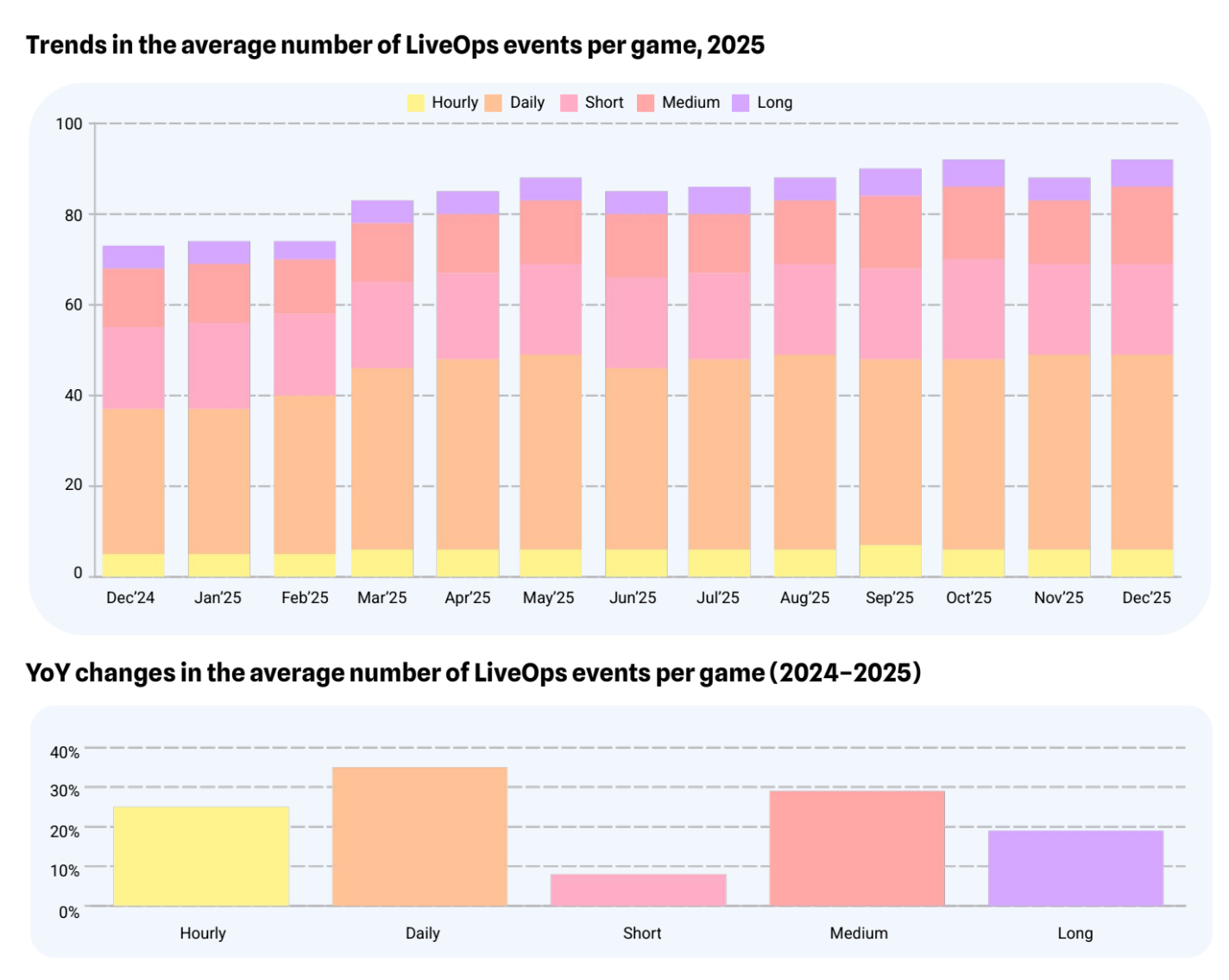

At the same time, LiveOps intensity increased significantly. In December 2025, the average number of LiveOps events was 16% higher than in December 2024.

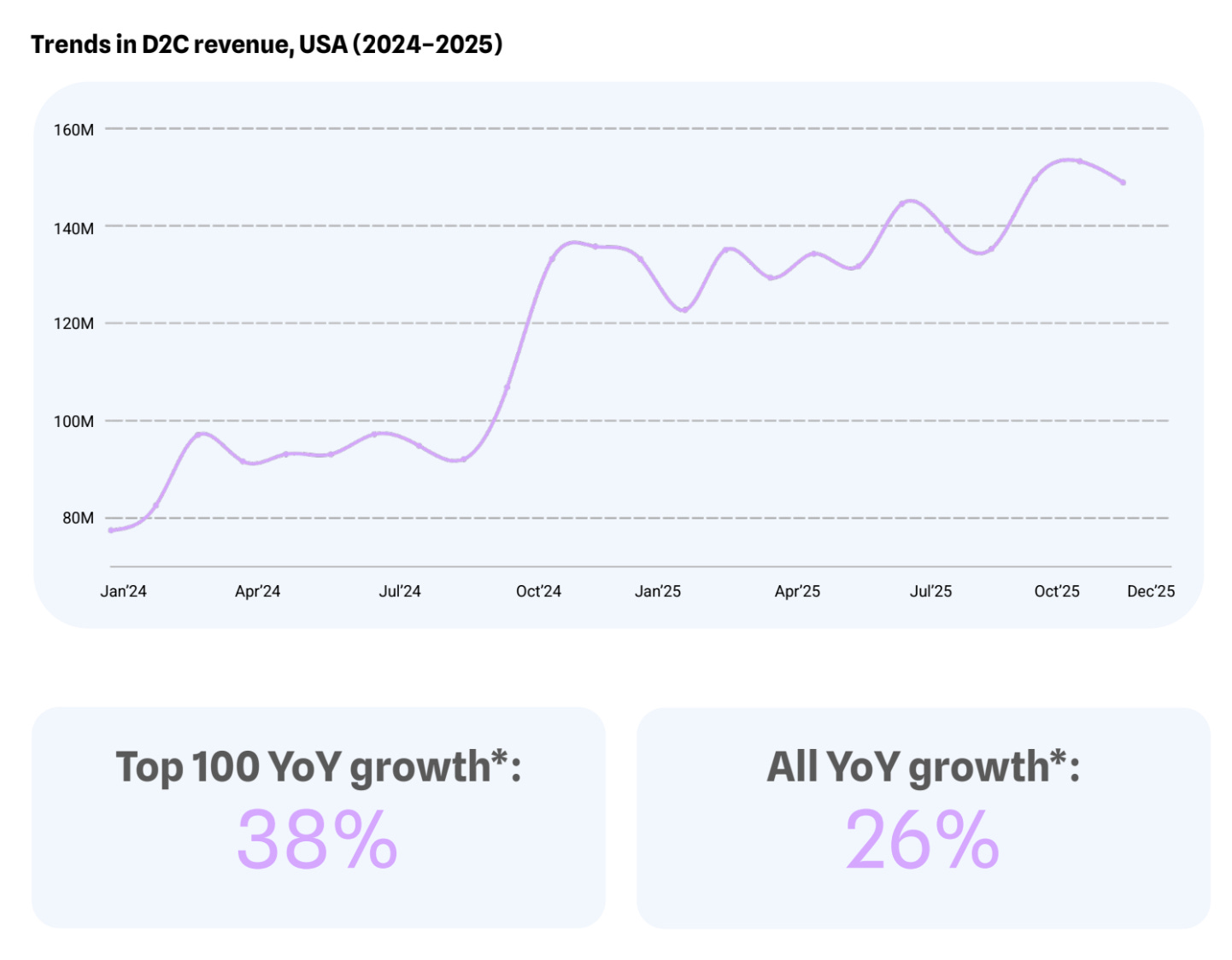

D2C revenue in the US continues to grow. In 2025, it increased by 26% YoY. Projects in the top-100 by revenue grew the fastest in this area, at +38% YoY.

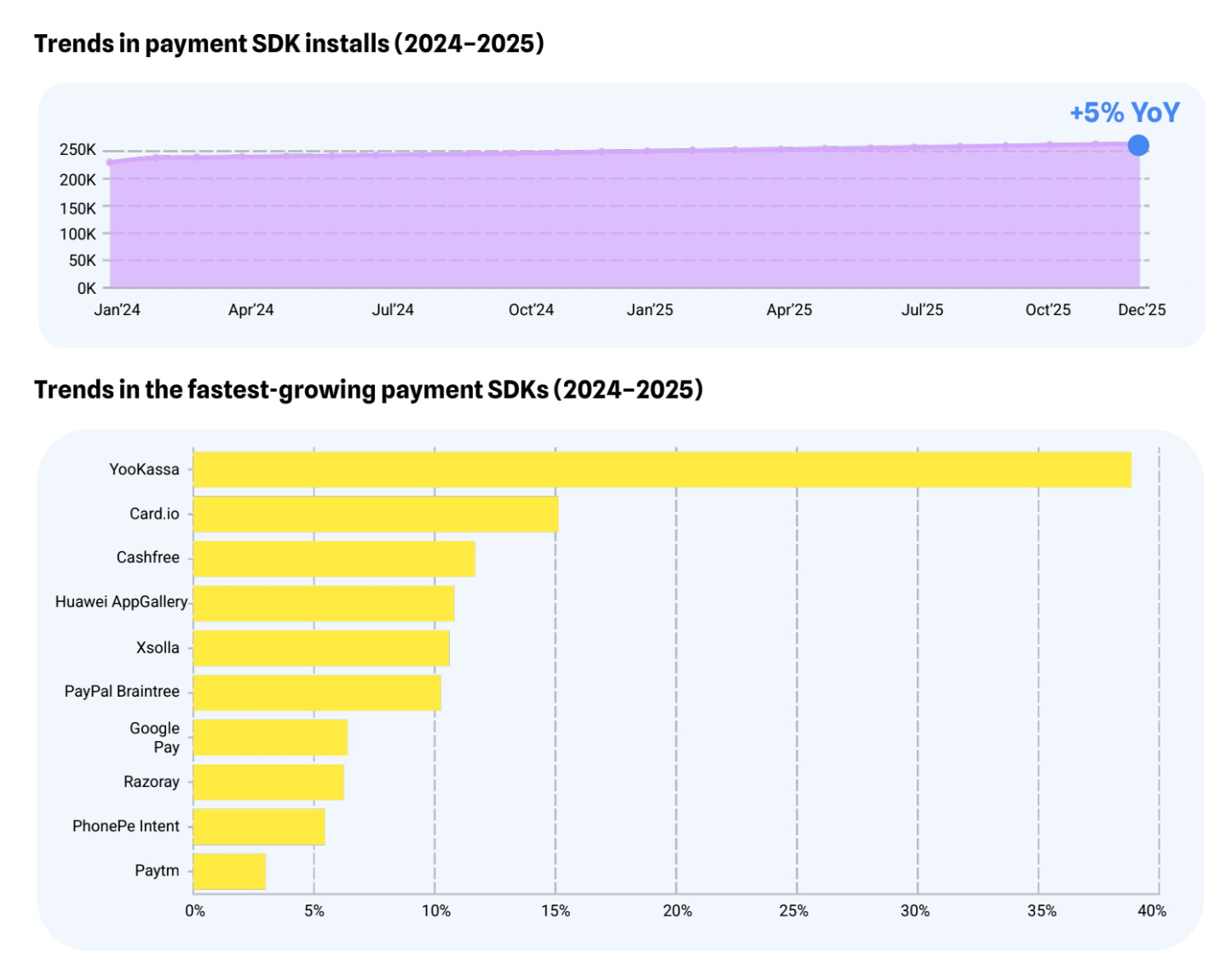

Growth in payment SDK integrations in games reached only 5% in 2025. The fastest-growing SDKs were YooKassa (a payment system focused on the Russian market, which means there is a continued interest in Russia after Visa and Mastercard exited), Card.io, and Cashfree.

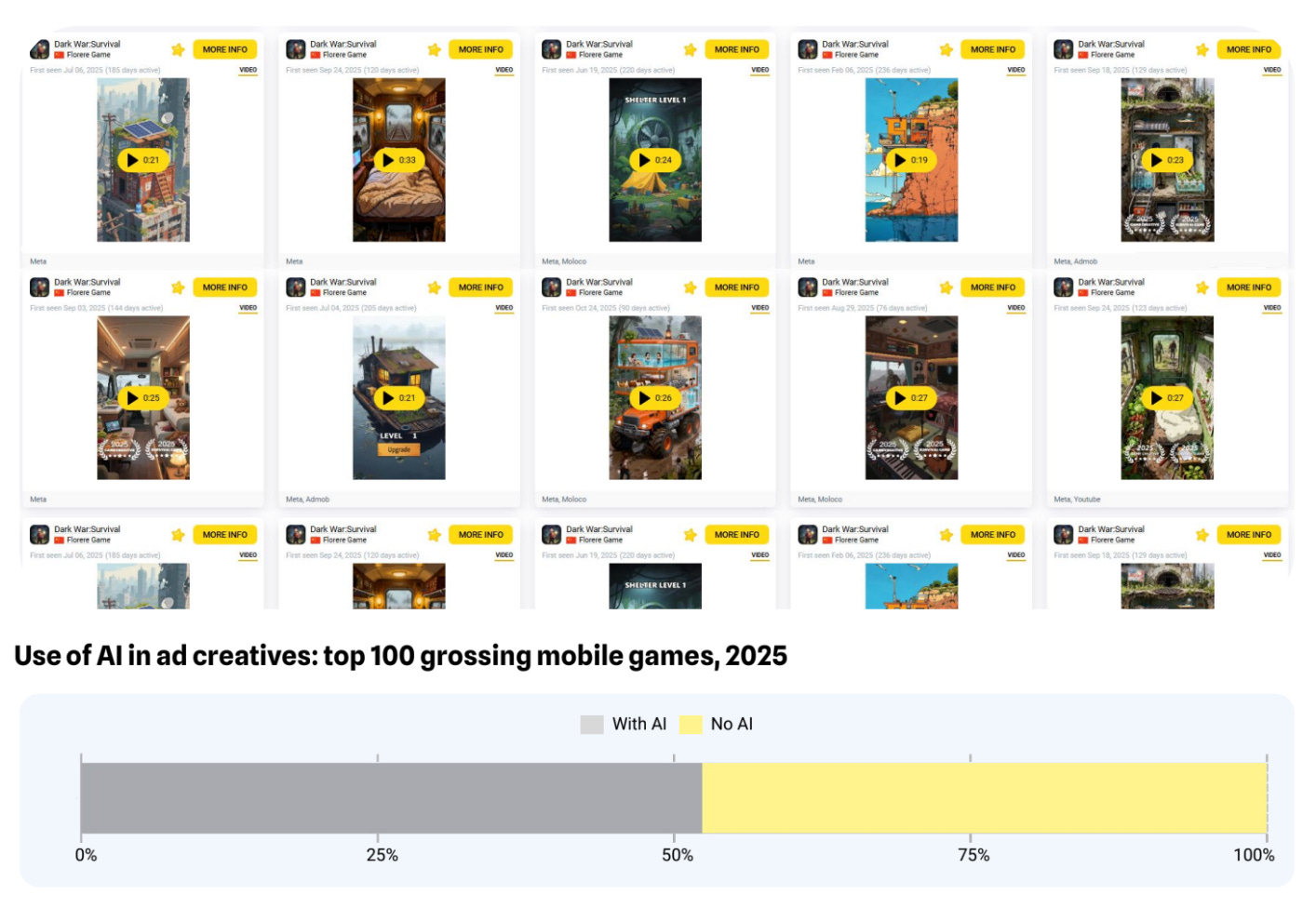

More than half of ad creatives (56%) used by top-100 revenue games were created with the help of AI. A notable example is Dark War: Survival, where (subjectively!) around 90% of creatives appear to be AI-generated.

Block Blast! (368 million, +66% YoY), Roblox (295 million, +37% YoY), and Garena Free Fire (287 million, -2% YoY) were the top games by downloads in 2025.

Mobile revenue leaders were already mentioned above. Pokémon TCG Pocket ($677 million in 2025) entered the top-10 and was the only relatively new project in the ranking.

Casual Games Trends

Downloads in the casual segment continued to grow, increasing by 8% in 2025.

Revenue, however, remained flat (and even slightly declined). Casual games generated around $21 billion in 2025.

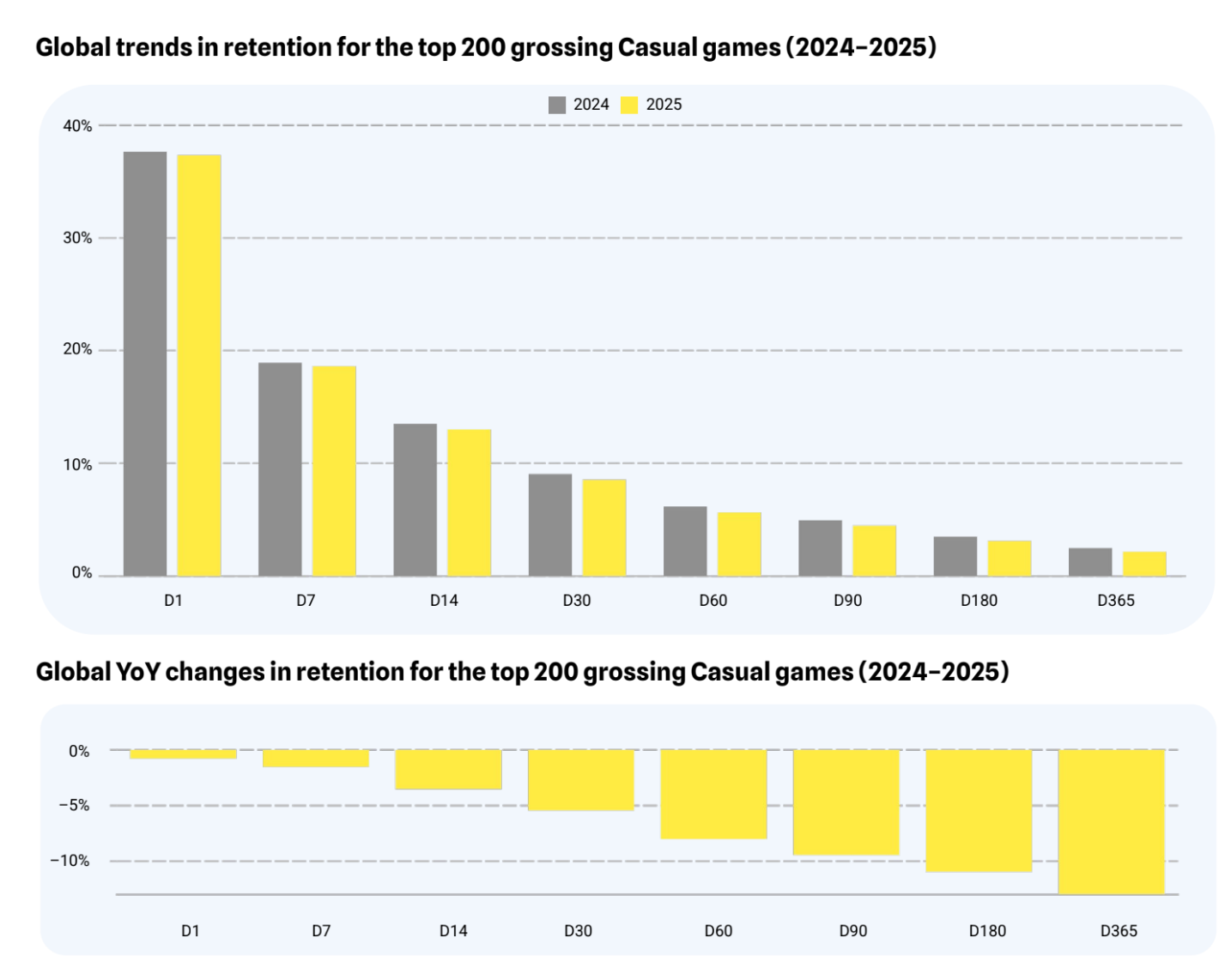

Mid-term and long-term retention for casual games declined. D14–D30 retention dropped by 3.5% to 5.4%, while the steepest decline was observed over a one-year horizon (-8% to -13%).

❗️We are speaking of percentage, not percentage points, decrease.

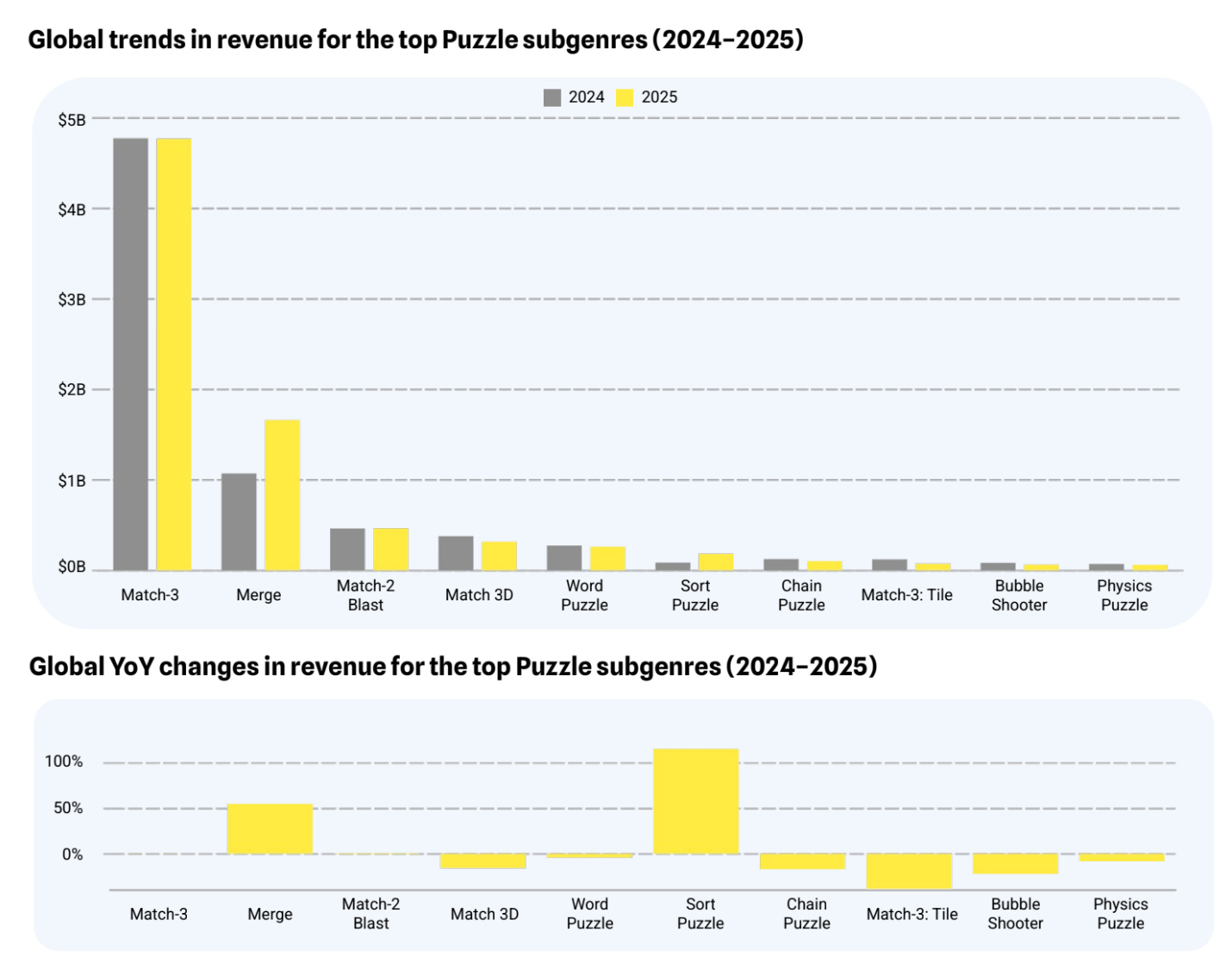

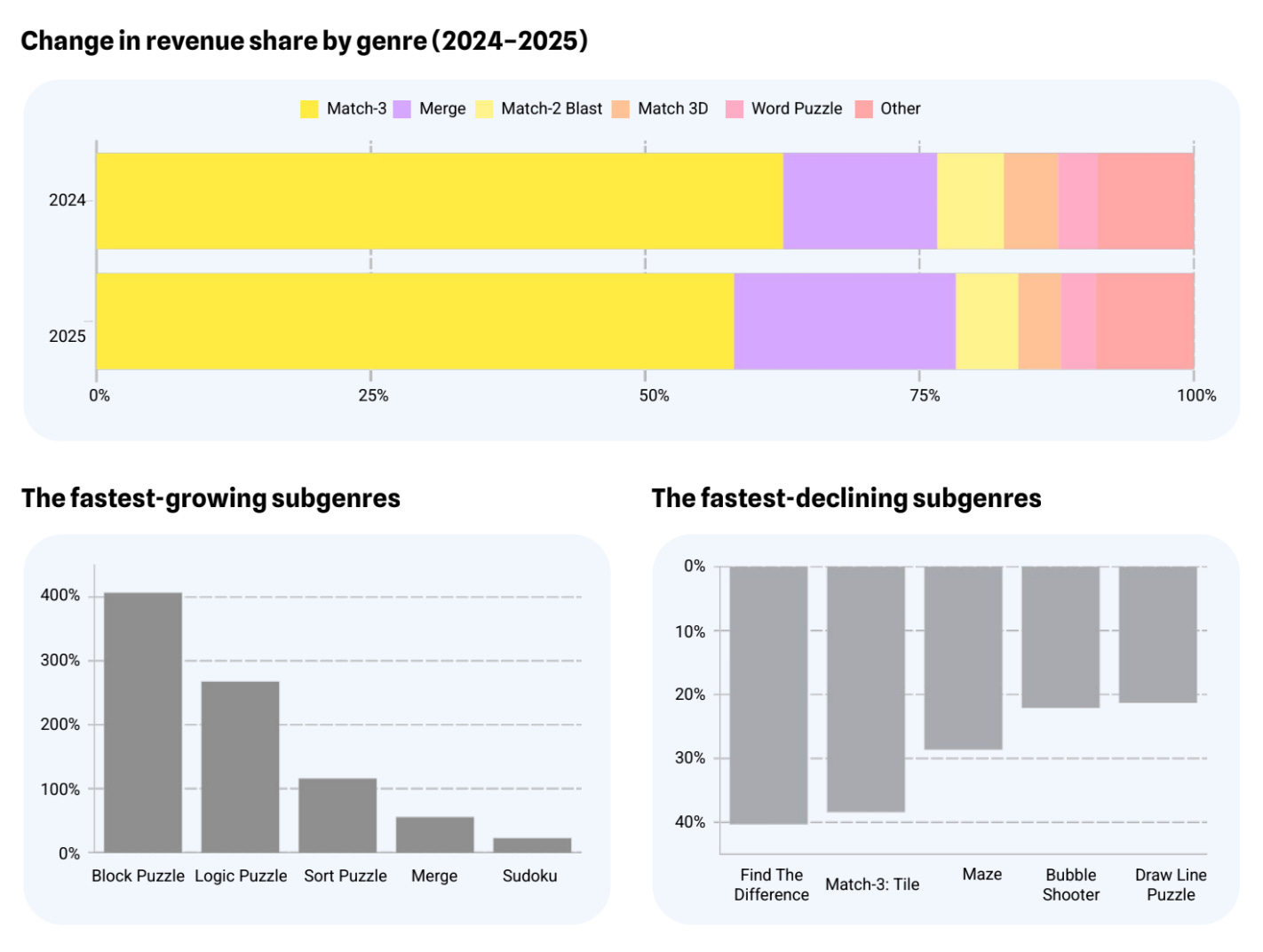

Match-3 remains the largest casual sub-genre. Its revenue in 2025 remained the same as in the previous year.

Merge games saw strong revenue growth (over 50%). The Sort Puzzle genre grew by 116%.

Merge games continue to take a growing share of total revenue.

Revenue growth leaders include Block Puzzle, Logic Puzzle, Sort Puzzle, Merge, and Sudoku.

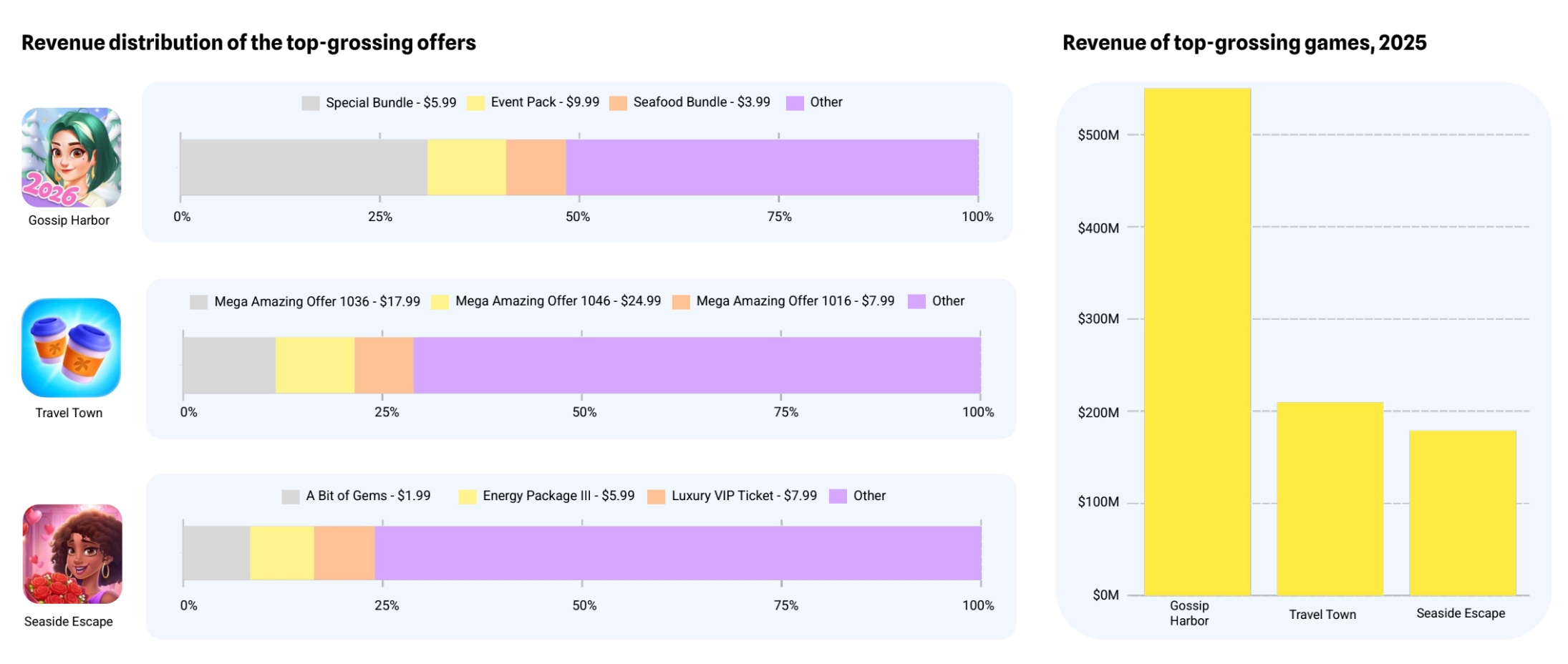

Despite the growth of Merge games, 80% of the genre’s revenue is concentrated in the top-10 titles. Gossip Harbor alone earned $550 million, accounting for over 33% of the entire genre’s revenue.

AppMagic notes that LiveOps events are the core monetization driver in Merge games, unlike other casual games, where monetization is centered around hard currency and bundles.

Midcore Games Trends

Midcore game downloads grew by nearly 5% in 2025.

Midcore games generated $33–34 billion in 2025, roughly at the same level as in 2024 (slightly lower).

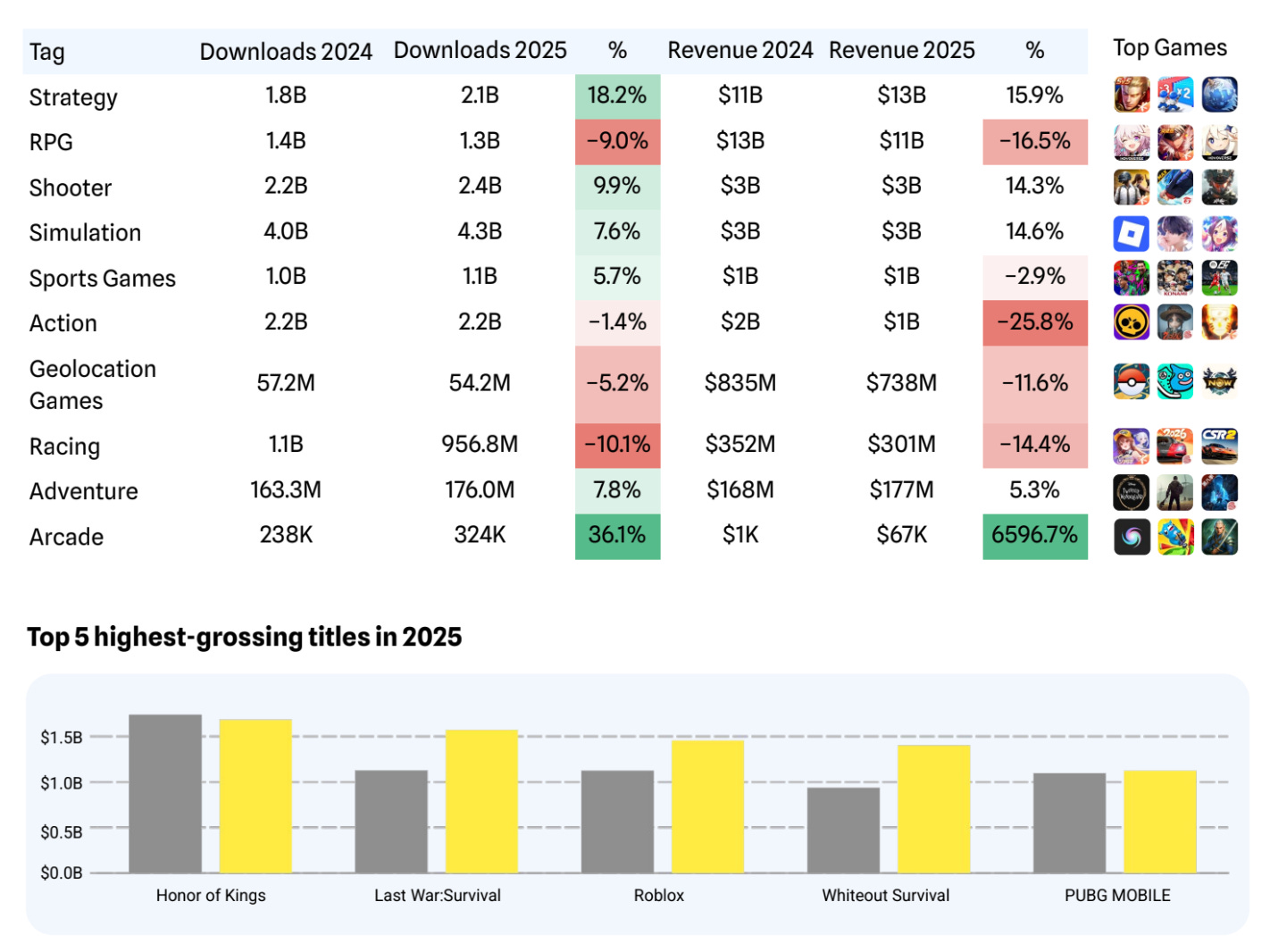

Strategies grew by 18.2% in downloads and 15.9% in revenue in 2025, making them the strongest genre in absolute growth terms. AppMagic classifies Honor of Kings as a strategy game.

Simulators and shooters also grew in revenue (nearly 15%), while arcade games had a strong year in downloads (+36.1% YoY).

Honor of Kings, Last War: Survival, Roblox, Whiteout Survival, and PUBG Mobile were the top revenue leaders of 2025. All except Honor of Kings showed growth.

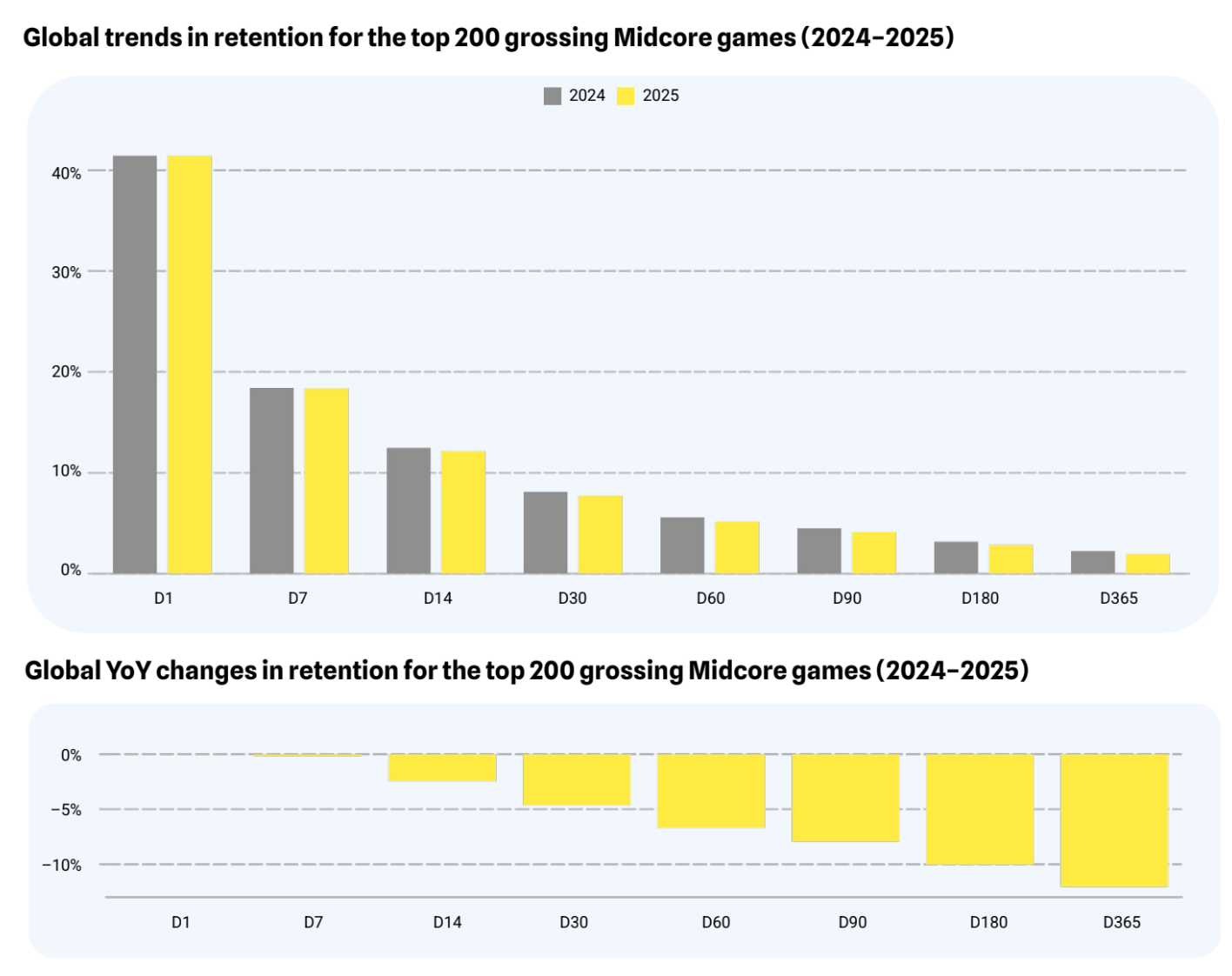

According to AppMagic, retention metrics for midcore games are declining at all stages, with the trend worsening over time. For example, D365 retention dropped by 12% in 2025 (again, not percentage points).

AppMagic links the lack of revenue growth, despite rising downloads, to declining retention.

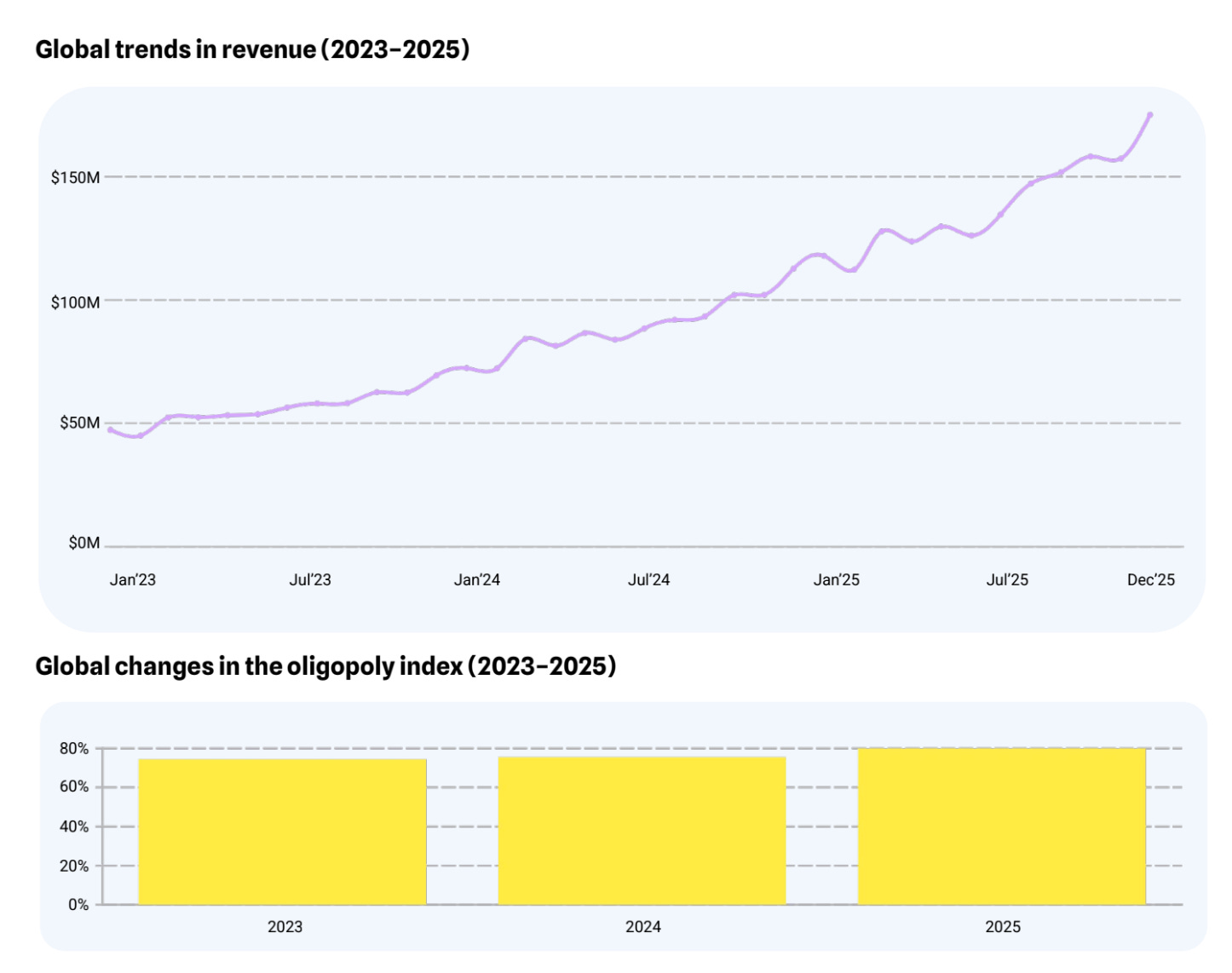

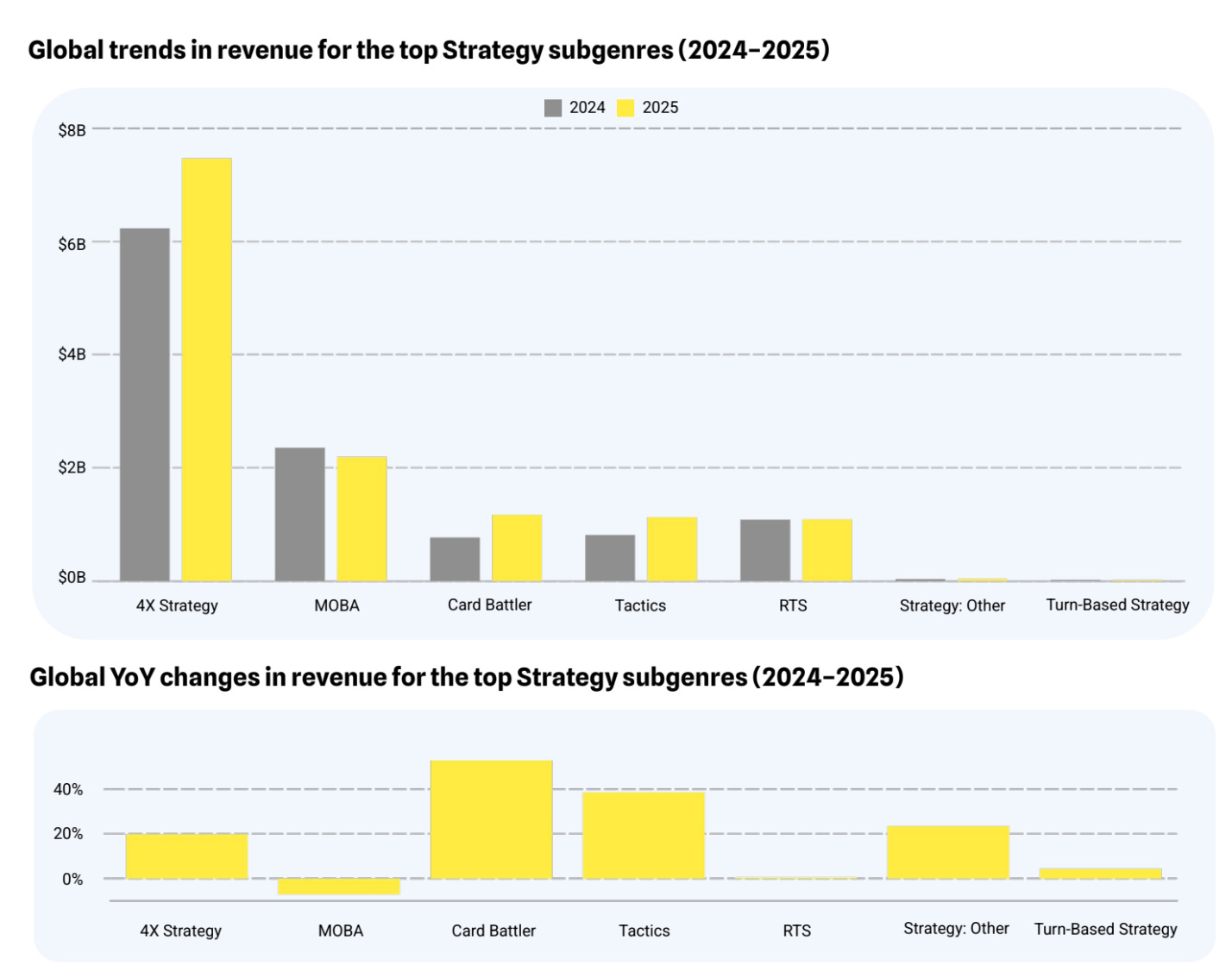

4X strategies are the main growth driver for midcore games. Although card battlers and tactical games grew faster, their absolute scale is much smaller.

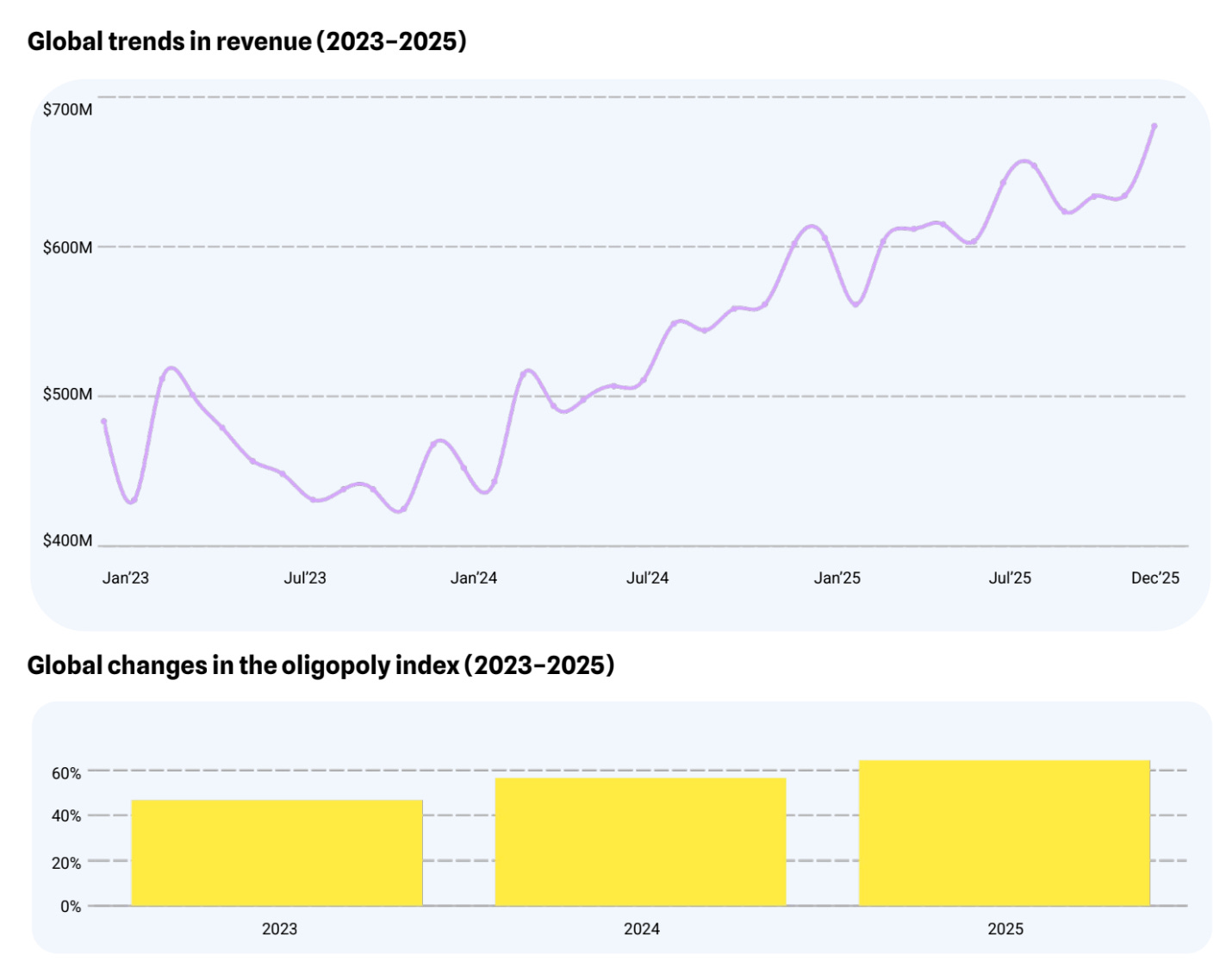

The oligopoly index in 4X is increasing. In 2025, the top-10 games accounted for 64% of revenue, up from 47% in 2023. At the same time, strong newcomers are emerging, such as Kingshot, launched in 2025.

AppMagic highlights the importance of high-priced offers in 4X strategies. These account for more than 25% of total revenue for genre leaders.

A word from our sponsor

Maximize your game’s global revenue with Xsolla’s Global Payments - offering seamless, localized checkout in multiple languages and integrating 1,000+ local payment methods to boost conversion rates.

Protect your income with advanced machine-learning anti-fraud, cross-game blocklisting, and 3DS 2.0, while Xsolla handles tax, compliance, support, refunds, and chargebacks for you. Deliver a smooth, secure payment experience optimized for all devices and expand your reach with confidence!

Make payments easy with Xsolla!

Hypercasual Games Trends

❗️Personally, I find the definition of this segment very blurred. It seems that both hypercasual and hybrid-casual games are included in this section.

IAP revenue for hypercasual games grew by 80% YoY. Over the past three years, this metric increased by 4–5x, indicating a significant increase in in-app purchases.

Downloads declined by 3.7% YoY in 2025.

Puzzles, simulators, and adventure games were the fastest-growing hypercasual (or hybrid-casual?) genres by revenue in 2025.

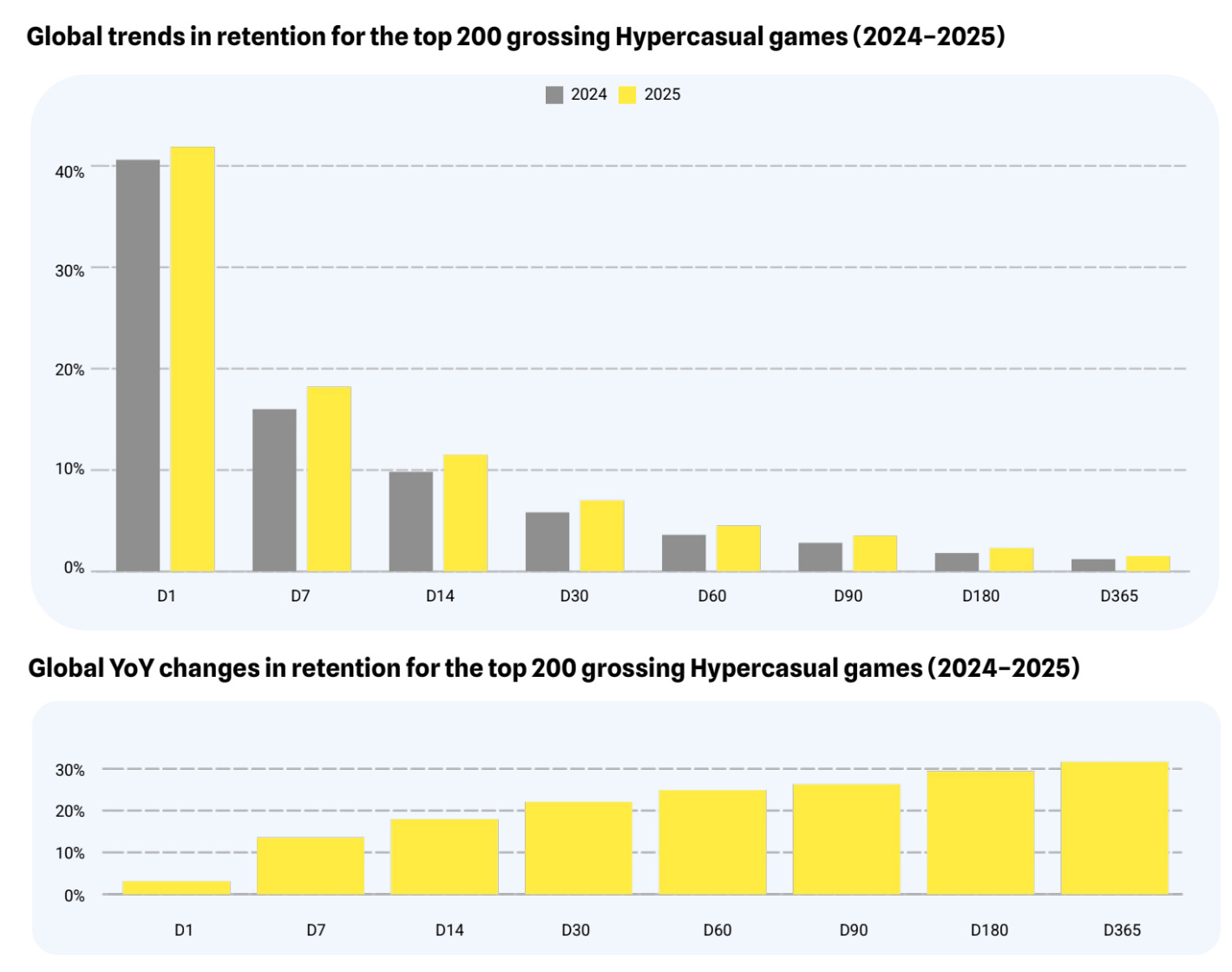

According to AppMagic’s methodology, hypercasual games improved retention at all stages, from D1 (+3%) to D365 (+32%). The longer the retention window, the higher the growth.

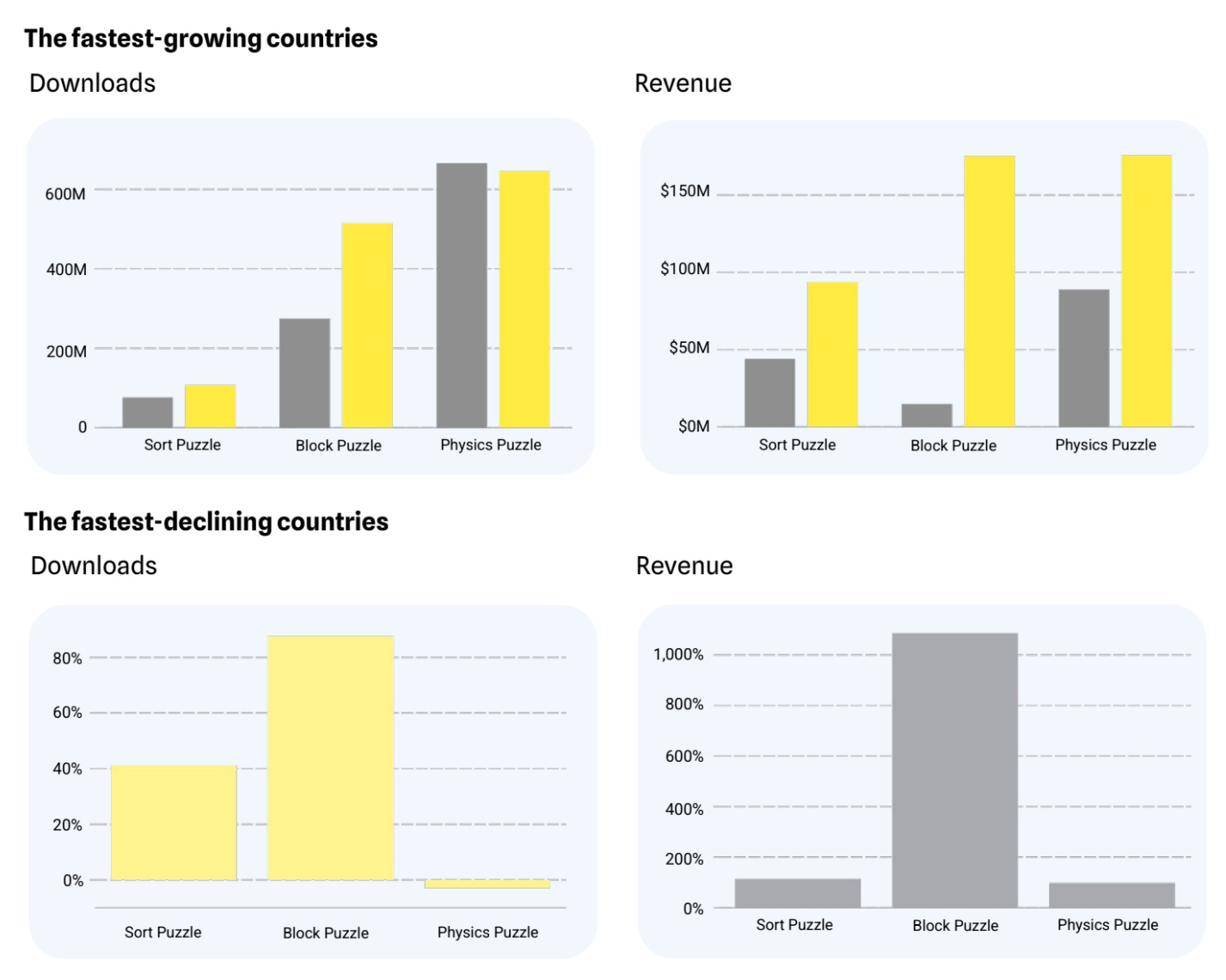

Block Puzzle was the fastest-growing sub-genre of the year, both in revenue and downloads.

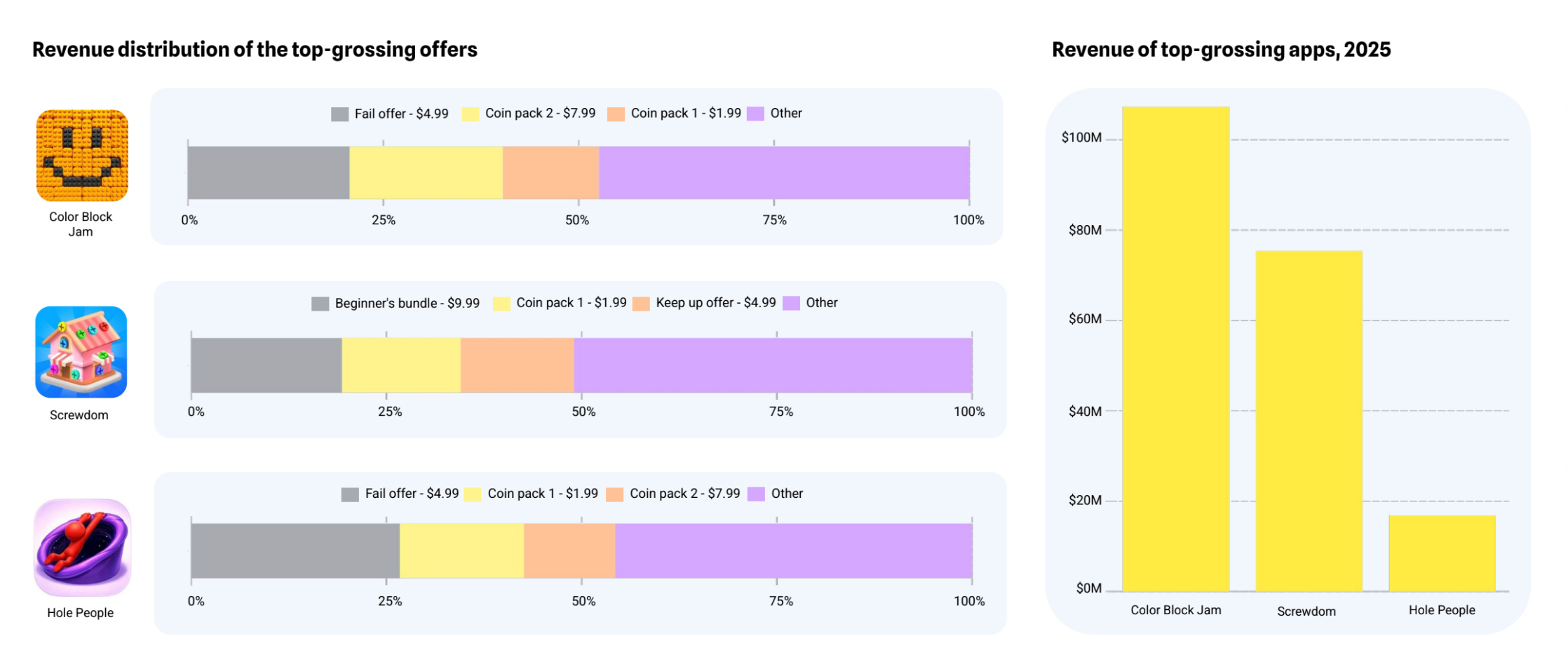

Monetization in hypercasual games is built around fail-offers and small (up to $8) currency bundles.