DDM: Gaming investment market overview in Q2 2023 & H1 2023

H1 2023 was the weakest since 2016, but H2 2023 has all chances to break all-time records.

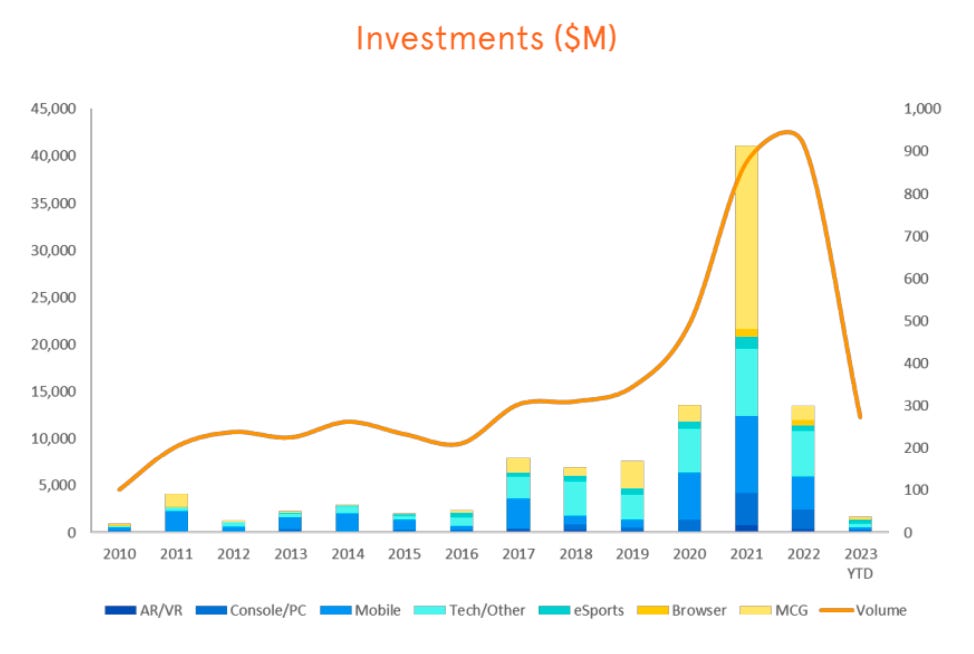

General Data

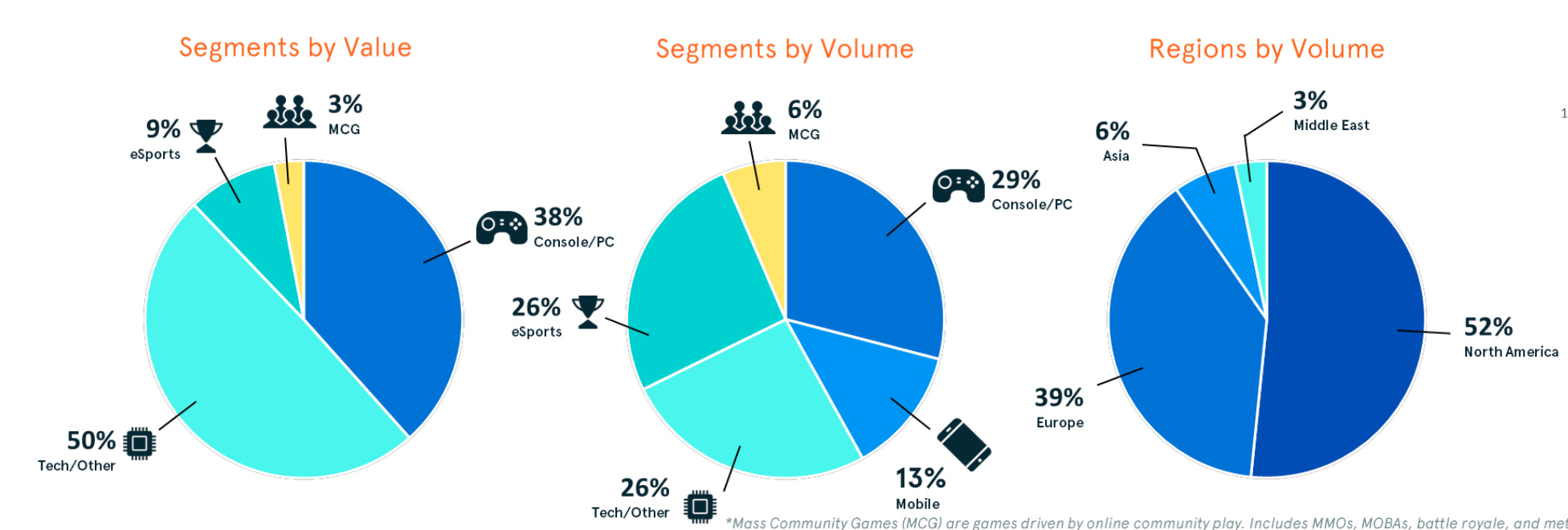

The most money in Q2 2023 was invested in technology gaming companies (24%); eSports (19%); mobile (19%).

The largest private investment deals in Q2 2023 were Everdome ($50M - blockchain game and metaverse development); Anzu ($48M - in-game native advertising); Mythical Games ($37M - blockchain-powered MMO development).

❗️However, there's a nuance - Everdome raised funds through token sales for $50M. This isn't a traditional fundraise in exchange for company equity.

By the number of transactions in Q2 2023, mobile games lead (30 transactions); technology companies (22 transactions); and PC/console games (11 transactions).

Polygon (6 investments); BITKRAFT Ventures (5 investments); Animoca Brands (4 investments) are the most active in Q2 2023.

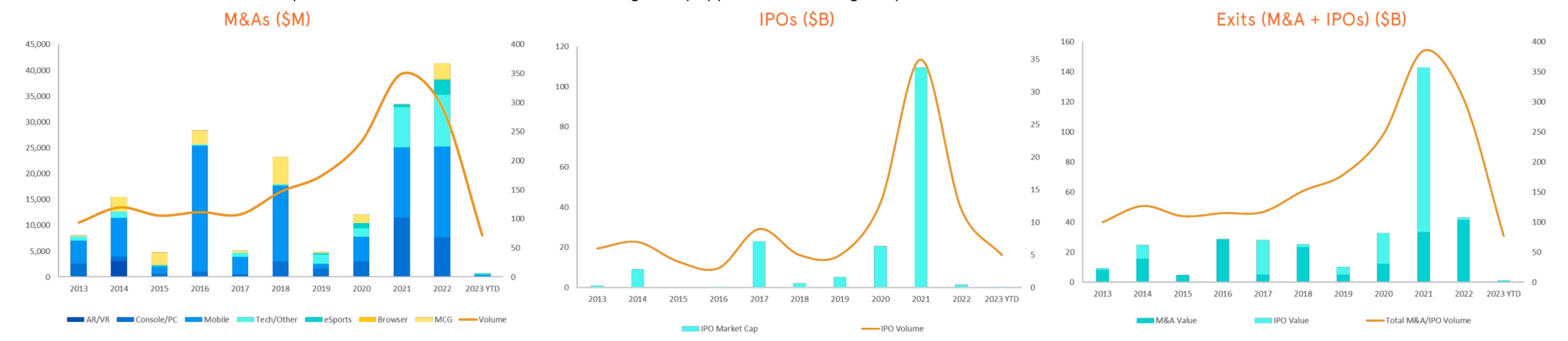

VRFabric had the only IPO of the quarter. It was listed on the Polish NewConnect exchange with a market capitalization of $11.4 million.

Comparison with Q1 2023

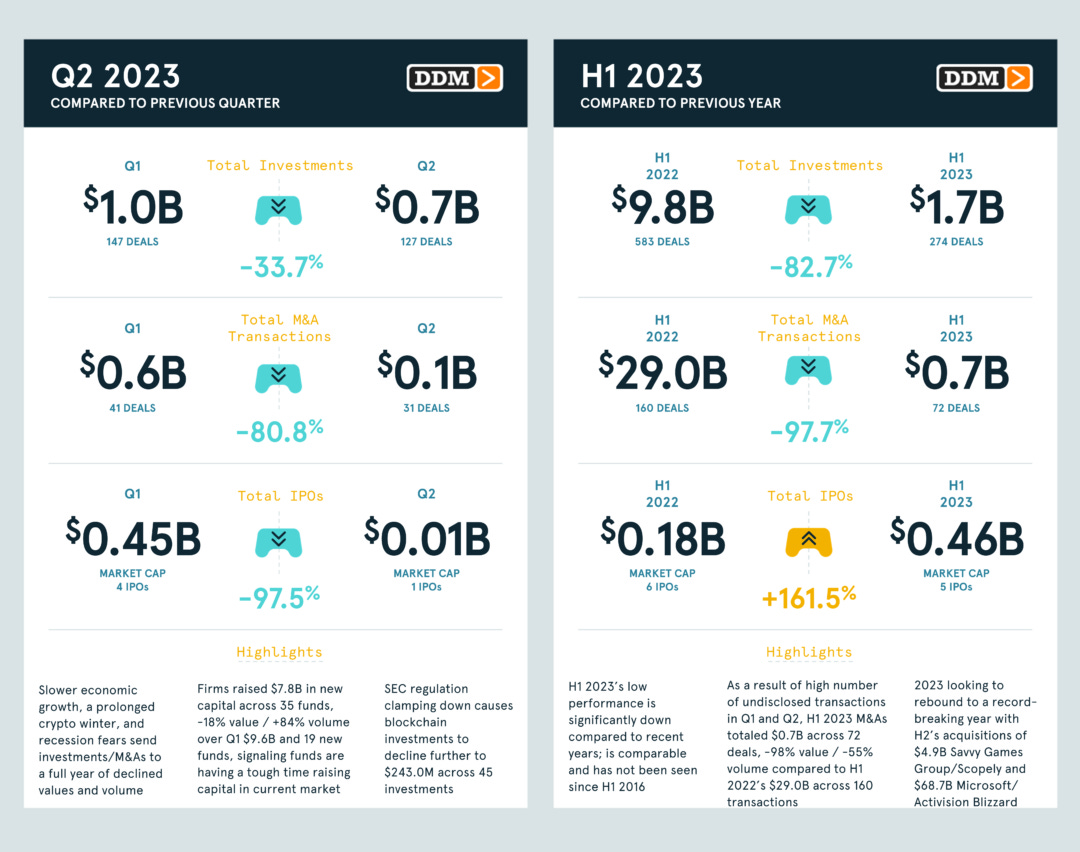

In the second quarter of 2023, there were 127 deals totaling $676 million. This is 33.7% less in volume compared to the first quarter (147 deals totaling $1 billion).

The number of M&A deals in the second quarter decreased from 41 (Q1 2023) to 31. The volume dropped from $565 million (Q1 2023) to $108.4 million.

Only one gaming IPO of $10 million happened in the second quarter of 2023. In the first quarter, there were 4, totaling $450 million.

Comparison with H1 2022

In the first half of 2023, there were 274 investment deals totaling $1.7 billion. This is 83% less in volume ($9.8 billion) and 53% less in number (583 deals) compared to the first half of 2022.

In H1 2023, the total volume of M&A deals was $673.4M with 72 transactions. This is 98% less in volume ($29 billion) and 55% less in number (160 transactions) compared to H1 2022.

❗️Deals involving SEGA and Rovio; Scopely and Savvy Games Group (Steer Studios); Microsoft and Activision Blizzard are expected in the second half of 2023, barring unforeseen events.

Mergers and Acquisitions (M&A)

The second quarter of 2023 ranks third from the bottom in terms of volume. Only the second quarters of 2010 and 2013 were weaker.

DDM notes that companies tend to "hold back" money.

The largest disclosed deals of the quarter were the acquisition of Wargraphs ($53.6 million - analytical service); Night Dive Studios ($19.5 million - developer); Hardsuit Labs (developer and service provider).

Blockchain and Web3

Investments in crypto projects continue to decline. In Q2 2023, they decreased by 38% in volume (from $390.7 million to $243 million) and 34% in number (from 68 transactions to 45).

46% of transactions by volume were from the USA; 25% from the Middle East; 19% from Europe.