Weekly Gaming Reports Recap: December 2 - December 6 (2024)

Top November games by AppMagic; Mobile monetization by AppsFlyer & more.

Reports of the week:

AppMagic: Top Mobile Games by Revenue and Downloads in November 2024

Chinese App Store created a $531B turnover in 2023

Midia Research: Gamers watch games more than they play them

AppsFlyer: Mobile game monetization in Q3'24 in North America and T1 Western countries

AppMagic: Top Mobile Games by Revenue and Downloads in November 2024

AppMagic provides revenue data after deducting store commissions and taxes.

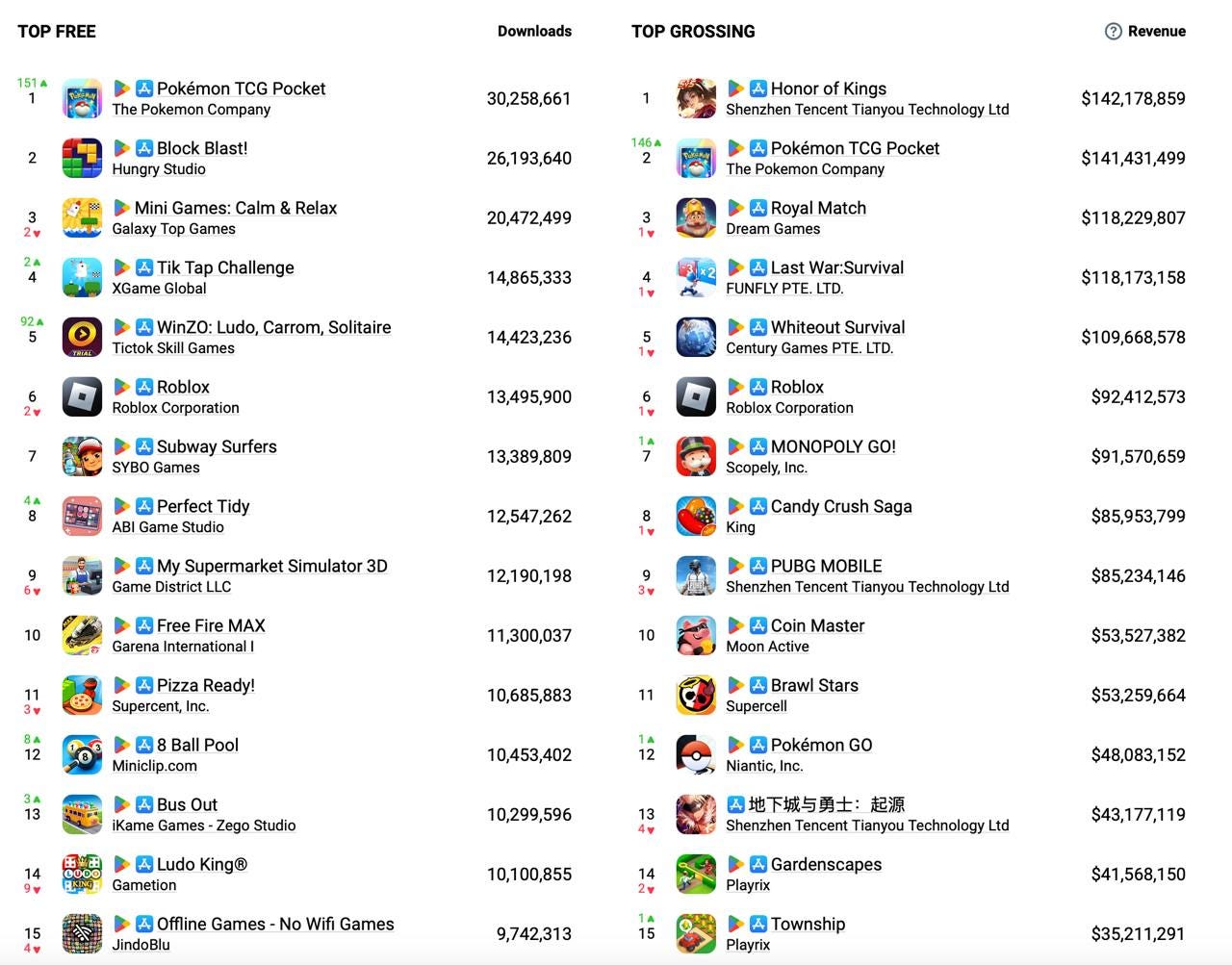

Revenue

Honor of Kings is the revenue leader for November. The game earned $142.2 million, 97% coming from iOS in China.

The main event in the revenue chart is the appearance of Pokemon TCG Pocket. The game earned $141.4 million in the first full month (just short of first place). 42% of the revenue comes from Japan; 27% from the USA. The RPD in Tier-1 Asian countries is $19.42; in Tier-1 Western countries, this figure is significantly lower at $3.79.

Otherwise, the November revenue chart can hardly be called dynamic. There are no major changes.

Downloads

Pokemon TCG Pocket became the leader in downloads in November - the game was downloaded more than 30 million times.

Block Blast! is in second place (26.2 million installs); Mini Games: Calm & Relaxis in third place (20.5 million).

WinZO: Ludo, Carrom, Solitaire burst into 5th place - this is a set of various games from an RMG (Real Money Gaming) developer, but without the need to play for real money. It is positioned as an app where you can hone your skills for free. 99% of downloads are from India.

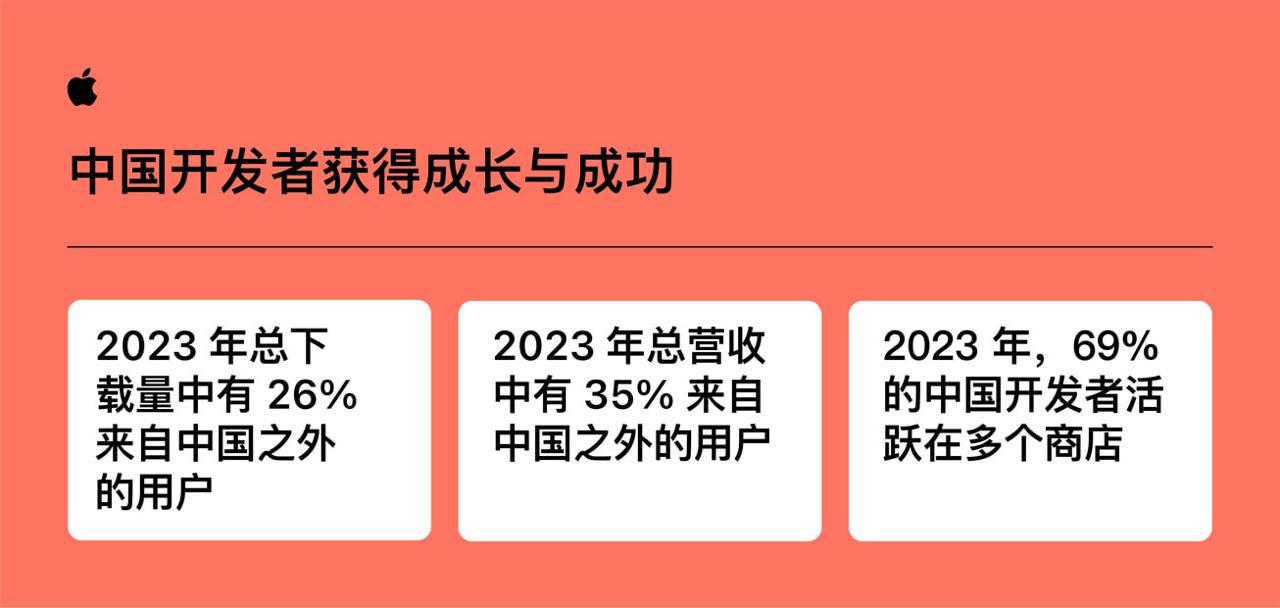

Chinese App Store created a $531B turnover in 2023

The research was shared by Ju Heng, an associate professor at the Shanghai University of Finance and Economics Business School. This includes all applications, not just games.

The turnover of the iOS app ecosystem is $531 billion (3.76 trillion yuan). This includes not only sales of in-game content but also sales of goods, services, and advertising within apps - for which Apple does not charge a commission. Retail apps earned the most (about 67% of this amount).

❗️For conversion to dollars, I used the average exchange rate for 2023.

91% of this amount ($483.2 billion) are purchases of physical goods or services through apps (not subject to commission). 5% ($26.55 billion) is advertising, also not subject to commission. Finally, 4% ($21.24 billion) is revenue from digital goods purchases and subscriptions (what Apple charges a commission for).

At the same time, the study notes that most apps pay a 15% commission under the Small Business Program. This means their revenue from digital goods is no more than $1 million per year.

Ju Heng notes that the App Store ecosystem has grown 2.3 times in turnover since 2019.

In 2023, more than 70% of Chinese developers worked for the global market.

Apps from Chinese developers were downloaded more than 8 billion times in 2023. 26% of this number were international downloads. In 2018, the share of international downloads was 12%.

90% of all downloads and 95% of turnover in China came from apps by local developers in 2023.

Midia Research: Gamers watch games more than they play them

The survey included players from the USA, Canada, UK, Germany, France, Sweden, Brazil, South Korea, and Australia.

Gamers spend about 7.4 hours per week playing games.

However, they spend 8.5 hours per week watching game-related video content on YouTube and Twitch.

At least once a month, 24% of PC/console gamers watch videos about games. Paying users watch more content about games - among them, 48% have watched gaming content at least once in the last month. This may be because they are generally more engaged.

AppsFlyer: Mobile game monetization in Q3'24 in North America and T1 Western countries

AF analyzed aggregated data based on $130 million IAP revenue; $40M subscription revenue, and $900M advertising revenue. All data is for Q3’24. North America and Tier-1 Western countries were considered.

D90 ARPU by monetization models and genres

AF data for Tier-1 Western markets shows that projects with hybrid monetization demonstrate the best results in D90 ARPU on iOS. Their D90 ARPU is $9.69 (iOS) and $1.54 (Android) in mid-core projects. For comparison, mid-core projects with only IAP monetization have a D90 ARPU of $7.31 on iOS and $3.11 on Android.

IAP monetization currently performs best in casual games with the same set of parameters (Tier-1 Western countries; D90 ARPU). On iOS, D90 ARPU is $3.15; on Android - $2.15. In projects with hybrid monetization, the metric on iOS is $2.38; on Android - $2. Games with IAA monetization show the weakest results - $1.26 (iOS) and $0.81 (Android).

Interestingly, in hyper-casual projects, it’s not clear that hybrid monetization works better. D90 ARPU in projects with hybrid monetization is $0.82 on iOS and $0.6 on Android. Meanwhile, in projects with only advertising monetization, the metric is $0.71 on iOS and $0.47 on Android.

❗️ Most likely, this difference is related to taxonomy. Hybrid-casual games might be counted in the casual games category.

ROAS by genres and monetization types

AppsFlyer shows that casual projects with only IAP monetization achieve 215% D90 ROAS on iOS in T1 Western markets. Or they note that mid-core projects with hybrid monetization demonstrate 122% D30 ROAS on Android.

❗️This section raises more questions than answers. Such returns may occur in exceptional cases - in the best projects or the most successful campaigns. Based on the projects and metrics I’ve seen (hundreds of games in different genres), I’ve hardly seen such metrics from almost anyone. Therefore, I recommend treating the figures in this particular section skeptically.

Revenue accumulation in the first 90 days by genres and monetization types

65-66% of all revenue in casual projects with IAP monetization comes in the first 30 days. In mid-core games, 84-85% of all revenue comes in the first 30 days.

❗️The simple conclusion is that if your users don’t pay in the first weeks of the game, there’s a very high probability they won’t pay later.

In projects with advertising monetization, regardless of genre, about 85-95% of all revenue for 90 days comes in the first 30 days.

Similarly in projects with hybrid monetization. Regardless of genre, 81-86% of all revenue for 90 days accumulates in the first 30 days.

Consider subscribing to the GameDev Reports Premium tier to support the newsletter. Get access to the list of curated articles & archive of Gaming Reports that I’ve been collecting since 2020.

Revenue distribution between organic and paid traffic by genres

Purchased users bring 72-76% of all revenue for 90 days in hyper-casual and casual genres - regardless of the type of monetization.

In mid-core projects with IAP monetization, most of the cohort revenue for 90 days comes from organic users (56-61%). Where the focus is on IAA monetization, the share of organic in the revenue structure is from 28% to 37%.

If we consider all revenue for 90 days, without breaking it down by cohorts, the share of revenue from paid users grows in casual projects with IAP monetization. Conversely, it decreases in hyper-casual and casual games with advertising monetization.

But in mid-core games on Android, changes are visible. In terms of total revenue (not cohort), the share of purchased users in revenue grows to 64%. On iOS, the same 61% of organic users make the cash.