Weekly Gaming Reports Recap: February 19 - February 23 (2024)

Steam & EGS shared their annual results; InvestGame released a great report about investments in games in 2023; Apptica shared the State of the Mobile Market.

Reports of this week:

InvestGame: Gaming Investments in 2023

Game sales Round-up (07.02.2024 - 20.02.2024)

Apptica: The State of the Mobile Gaming Market and Advertising in 2023

Steam: 2023 Results

Epic Games Store: Results of 2023

Newzoo: Palworld in January 2024

InvestGame: Gaming Investments in 2023

Private Investments

In 2023, 403 deals were made totaling $2.7 billion. This marks a 4-fold decrease in volume compared to the previous year and a 36% decrease in the number of deals.

Speaking specifically about developers and publishers, in 2023, there were 136 deals (+23.6% compared to 2022) in the early stages totaling $511 million (-70% compared to 2022).

In later rounds, there were 12 deals in 2023 (30% less than in 2022) totaling $367 million (2.4 times less than in 2022). This also covers only deals with developers and publishers.

Moreover, in January 2024 alone, two major deals occurred - a $1.5 billion transaction between Disney and Epic Games; and a $110 million round for Build a Rocket Boy.

InvestGame experts note that in 2024, we may see an increase in deals in later rounds, as well as the closure of companies that received investments in 2020-2022 (companies that fail to show results and/or cannot attract additional funding due to high valuations from previous rounds).

Corporate investment funds are more inclined to engage in joint deals with VC funds, which helps reduce financial risks.

The USA, Western Europe, Asia, and the MENAT region are the most active markets in terms of VC deals.

M&A

Taking into account the Microsoft and Activision Blizzard deal, the volume of M&A deals in 2023 amounted to $78.2 billion. This is almost twice the amount in 2022 ($40.8 billion). Excluding this deal, there were M&A transactions worth $9.5 billion in 2023, 4.3 times less than the previous year. The number of deals dropped from 231 in 2022 to 121 in 2023.

InvestGame's forecast for 2024 is an increase in business M&A activity. For instance, a deal has already occurred between CVC and Haveli to acquire Jagex.

Overall, large companies ended 2023 confidently, setting an optimistic tone. However, recession risks, platform regulations, and state interventions (such as laws on loot boxes) could impede growth.

Public Offerings

In 2020-2021, the gaming market witnessed a boom in public offerings amid active industry growth. However, in 2022, the situation changed drastically due to macroeconomic crises and corrections. Only 23 companies conducted public offerings, raising a total of $3.6 billion (almost 7 times less than in 2021).

Signs of improvement appeared in 2023. There were 43 public offerings (almost double the previous year) totaling $4.2 billion (+16% compared to 2022).

InvestGame believes that companies are increasingly considering public offerings. There's likely pent-up demand that could materialize if the industry situation improves.

AI Investments

Since 2020, there hasn't been a single quarter without deals with companies specializing in AI. However, the number of deals in 2023 doubled - 57 compared to 28 in 2022. Yet, the total investment volume hardly increased - $545 million in 2023 compared to $519 million in 2022. This refers specifically to AI solutions for games.

Investments in Platforms and Technologies

The number of deals in technological and platform solutions plummeted by 40% in 2023 to 82. Investments in platforms remained roughly the same ($0.6 billion compared to $0.7 billion in 2022), while investments in technological solutions plummeted 16 times from $7.9 billion in 2022 to $0.5 billion in 2023.

It's worth noting that the Unity merger with ironSource ($4.4 billion) occurred in 2022.

InvestGame analysts believe that the consolidation of the technical gaming market is nearing its end.

Blockchain Investments

The number of deals nearly halved from 278 in 2022 to 145 in 2023. The investment volume dropped almost 4.5 times from $3.95 billion in 2022 to $0.9 billion in 2023.

Nevertheless, InvestGame notes a positive trend. The market in 2023 is significantly higher than in 2020. Overall, the gaming Web3 market is becoming niche, with fewer developers, investors, and smaller checks.

Esports Investments

The number of investments in esports decreased by 20% in 2023 (37 deals). The investment volume dropped by 4.8 times to $471 million.

Despite esports existing for a long time, companies still struggle to establish an effective business model for fully monetizing their audience.

Game sales Round-up (07.02.2024 - 20.02.2024)

Chrome Valley Customs has earned $40 million since its release in June 2023. Space Ape expects the game to become the highest-earning in their portfolio. Previously, the studio released Beatstar ($120 million in 2 years).

Persona 3 Reload sold a million copies in a week. It's the fastest-selling game in Atlus' history.

Helldivers 2 is doing great. On February 11th, developers reported the first million copies sold, and on February 19th, the game reached a peak online of 411 thousand players on Steam alone.

Silent Hill: The Short Message has been downloaded over 2 million times. However, both critics and players received the project reservedly.

Kingdom Come: Deliverance has reached 6 million copies sold. It took 2 weeks for the first million and just over a year and a half for the sixth.

Granblue Fantasy: Relink surpassed 1 million copies in 11 days. Interestingly, the peak online at launch for a fairly niche project was 114 thousand people.

Marvel’s Spider-Man 2 reached 10 million sales in less than 4 months since release. The first 5 million were sold in a few weeks; total franchise sales exceeded 50 million copies.

Bandai Namco Entertainment is pleased with the results of Tekken 8 - the game sold 2 million copies in less than 3 weeks. The company reports that sales of the new installment are better than those of previous entries in the series.

Metro Exodus has entered the club of projects that have sold over 10 million copies. In 2022, there were reports of 6 million sales - impressive growth.

Alan Wake II sold 1.3 million copies. It's the fastest-selling game from Remedy; in the first couple of months, it outsold Control by 50% in 4 months. "You have no idea how difficult it is to make a game that will be bought a million times," Remedy said. We believe them.

Apptica: The State of the Mobile Gaming Market and Advertising in 2023

The company collected data on 37 countries from January 1 to December 31, 2023. Only the App Store and Google Play were taken into account. All revenue - Gross.

iOS Games

Downloads on iOS in 2023 decreased by 9.75%, with a total of just over 6 billion downloads. Casual projects, action, and Simulation genres are leaders.

Revenue from iOS games in 2023 was just over $35 billion (-6.7% from the previous year). The RPG genre saw the sharpest decline, by 12%, but it still remains the largest.

Android Games

The total number of downloads on Android in 2023 was over 51 billion. Puzzle games saw the strongest growth (+5.25%), Simulation genre (+5%), card games (+4.8%). Leaders in decline were RPGs (-12%), arcade games (-10%), and strategies (-8%).

Apptica counted the total revenue from Android games in 2023 at $20 billion.

Retention in Games

On average, Retention on Android is lower by 5-7 percentage points.

Casino games are leaders on iOS in R1 - 40.6%. This genre also leads in R30 on Android (9.1%) and iOS (13.6%). RPG games also show good figures in R1.

The average Retention for 1 day in games is 32.4%; for 30 days - 6.6%.

Downloads Leaders

Subway Surfers (225.4 million downloads); Candy Crush Saga (199 million) and Roblox (195 million) - leaders on Android in terms of downloads.

The situation is significantly different on iOS. Eggy Party (45.9 million downloads) is in first place, followed by MONOPOLY GO! (44.2 million), and Royal Match (42.8 million).

Eggy Party is not on the Android charts because Apptica does not take alternative stores in China into account.

Revenue Leaders

Coin Master ($425.9 million), MONOPOLY GO! ($415 million), and Candy Crush Saga ($369 million) - revenue leaders on Android.

Honor of Kings ($1.5 billion), Game for Peace, the Chinese version of PUBG Mobile ($611.5 million), MONOPOLY GO! ($609 million) - revenue leaders on iOS.

Advertising Market

According to Apptica's estimate, there are currently 109.8 thousand advertisers on the mobile market (-8.5% YoY). Of these, 53% are gaming advertisers.

Playrix is the most active advertiser on both iOS and Android.

The most mobile traffic is purchased for casual projects. For example, a quarter of all puzzle games on Android.

76% of all creatives on iOS are videos; 18.5% are static images; 5.5% are playables.

On iOS, only 4.6% of creatives last more than 30 days. The majority - 52.4% - last no more than 1-3 days.

In the case of Android, 75% of all creatives are videos; 23% are static; 2% are playables.

On Android, 3.9% of creatives last more than 30 days. 64% stop performing within the first 3 days.

It is noted that the popularity of UGC and influencers in advertising is growing. However, the use of misleads has decreased. In 2024, experts expect more AI-generated creatives.

Steam: 2023 Results

The company primarily focused on product updates, but there were several interesting figures.

More than 500 games on Steam earned over $3 million in 2023. This is twice as many as in 2018.

The company is proud that a quarter of the projects in the tops were released by developers whose games had not been released on Steam before.

However, this does not mean that the teams did not have such experience before.

Steam surpassed the 33 million CCU mark for the first time. Moreover, in 2024, the record has already been broken.

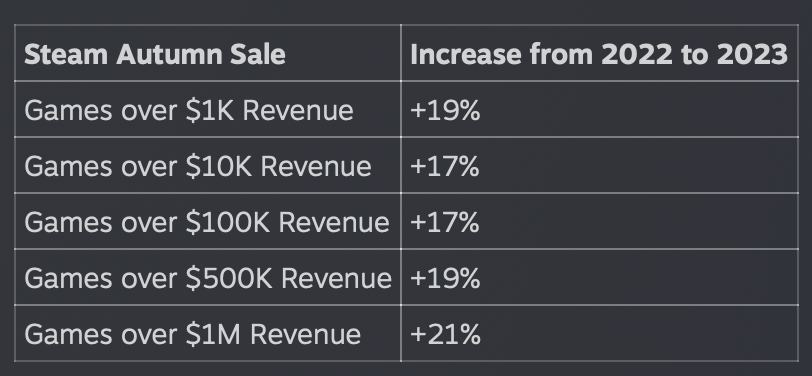

The company is very satisfied with its sales. For example, during the autumn sale of games earning over $1 million, there were 21% more than in 2022. Sales at such events are generally increasing.

Steam also notes that people actively use gift cards - both physical and digital. From December 20 to December 31, 2023, physical cards worth $80 million were activated.

Epic Games Store: Results of 2023

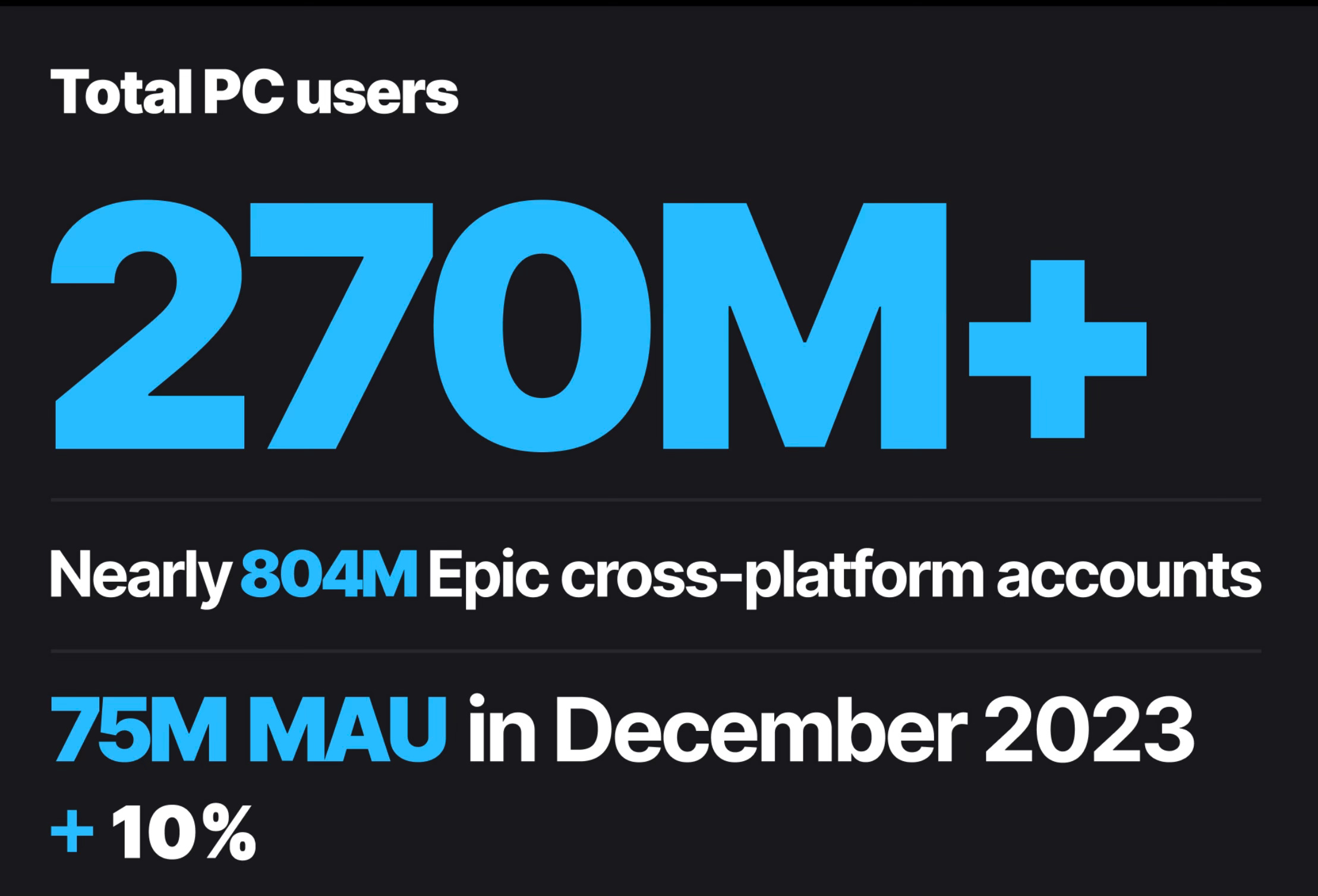

The number of EGS users has grown to 270 million - 40 million more than last year.

The total number of accounts in the Epic ecosystem reached 804 million.

The peak DAU on the platform in 2023 was 36.1 million users. MAU reached 75 million - last year it was 68 million.

In 2023, more than 1300 games were released on the Epic Games Store, bringing the total number to 2900 projects.

Users spent $310 million on games from third-party developers (-13% YoY). $950 million was spent on games from Epic Games (+16% YoY).

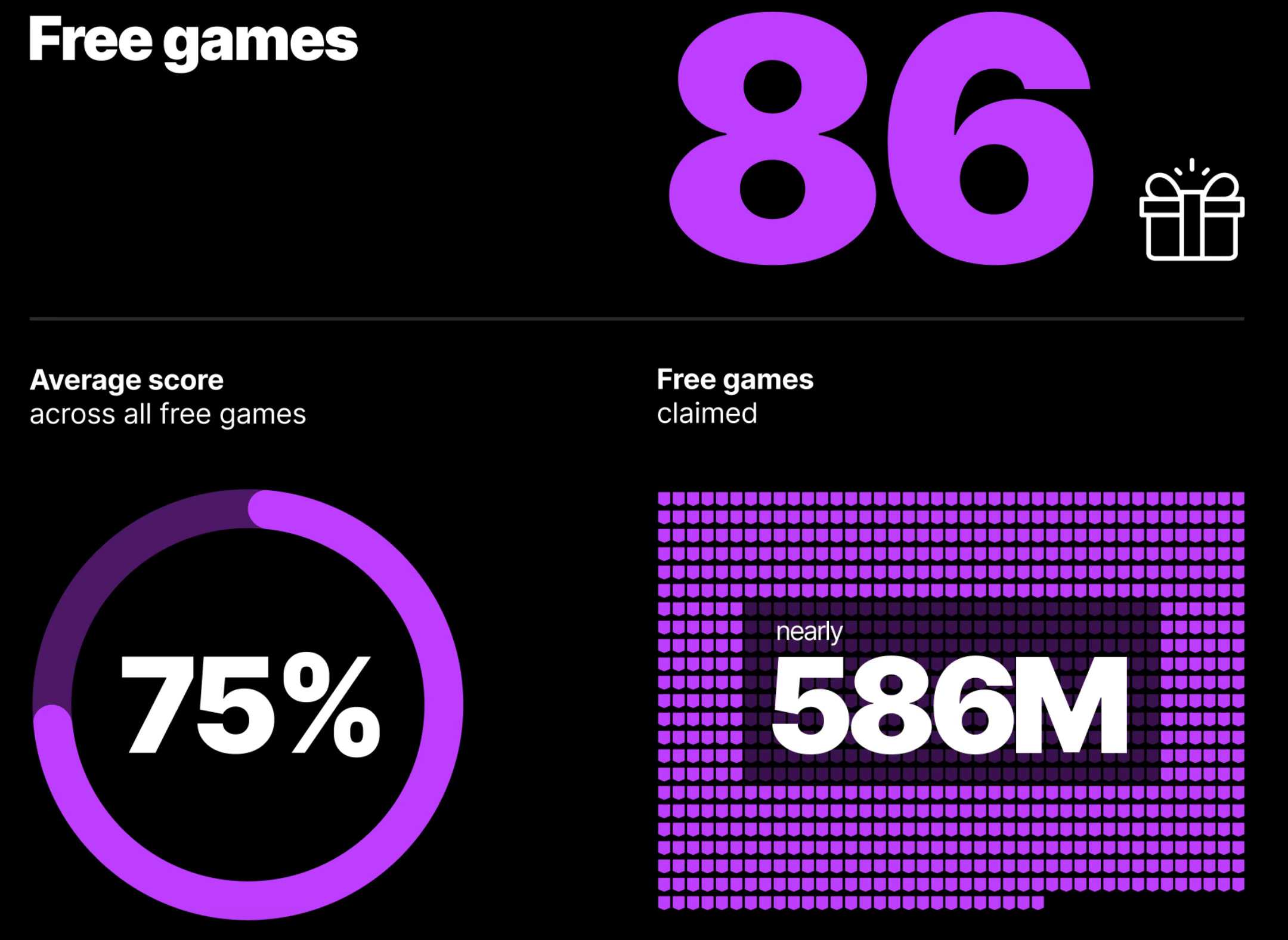

The company gave away 86 games in 2023 through the Free Games program. Their total retail value was $2055 with an average Metacritic score of 75. In 2023, users claimed 586 million copies of free games.

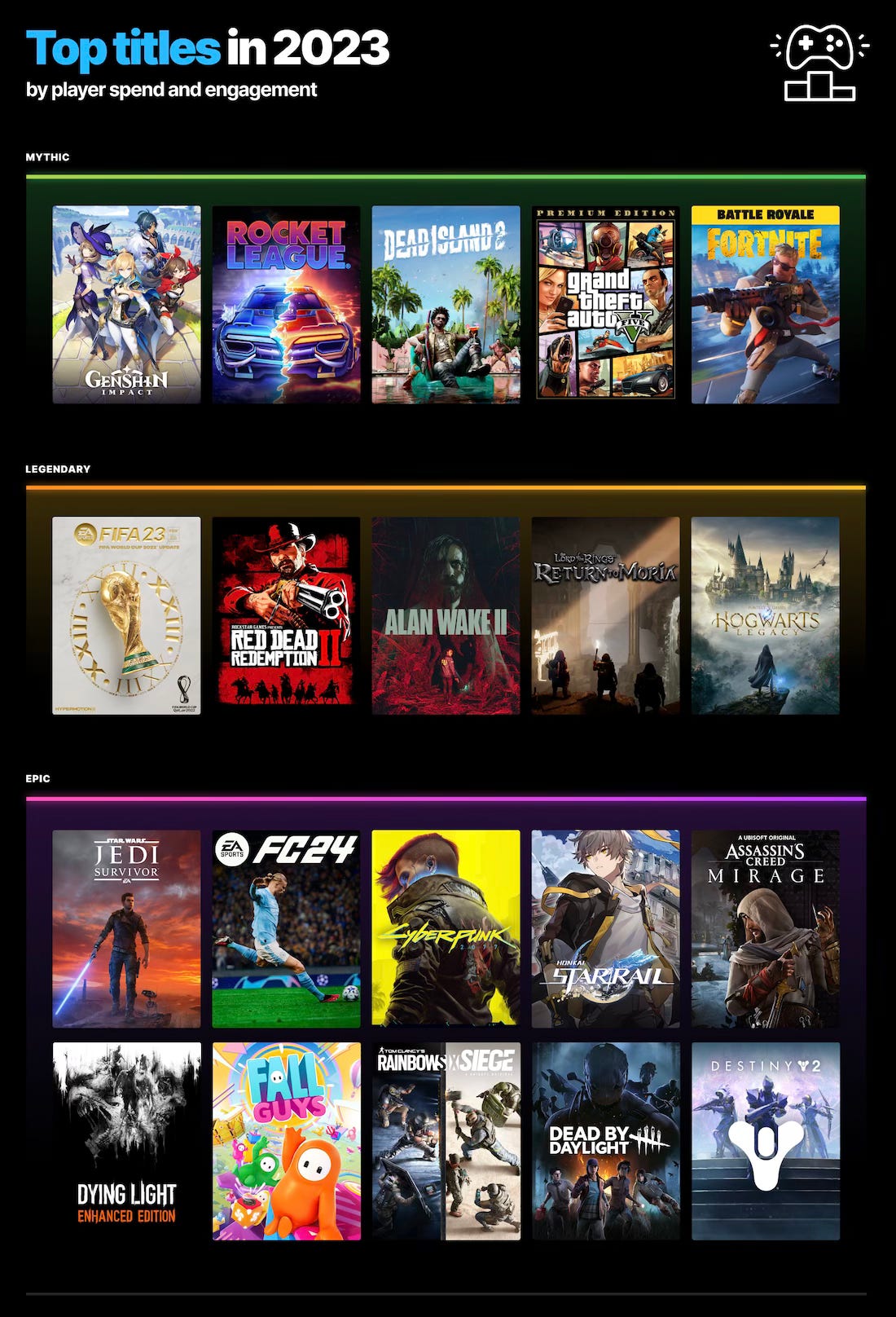

Genshin Impact, Rocket League, Dead Island 2, Grand Theft Auto V, and Fortnite were the most successful projects on the platform in 2023.

In 2024, the company promises to add preload for pre-orders; subscription support; dynamic bundles. And also - launch on iOS in Europe.

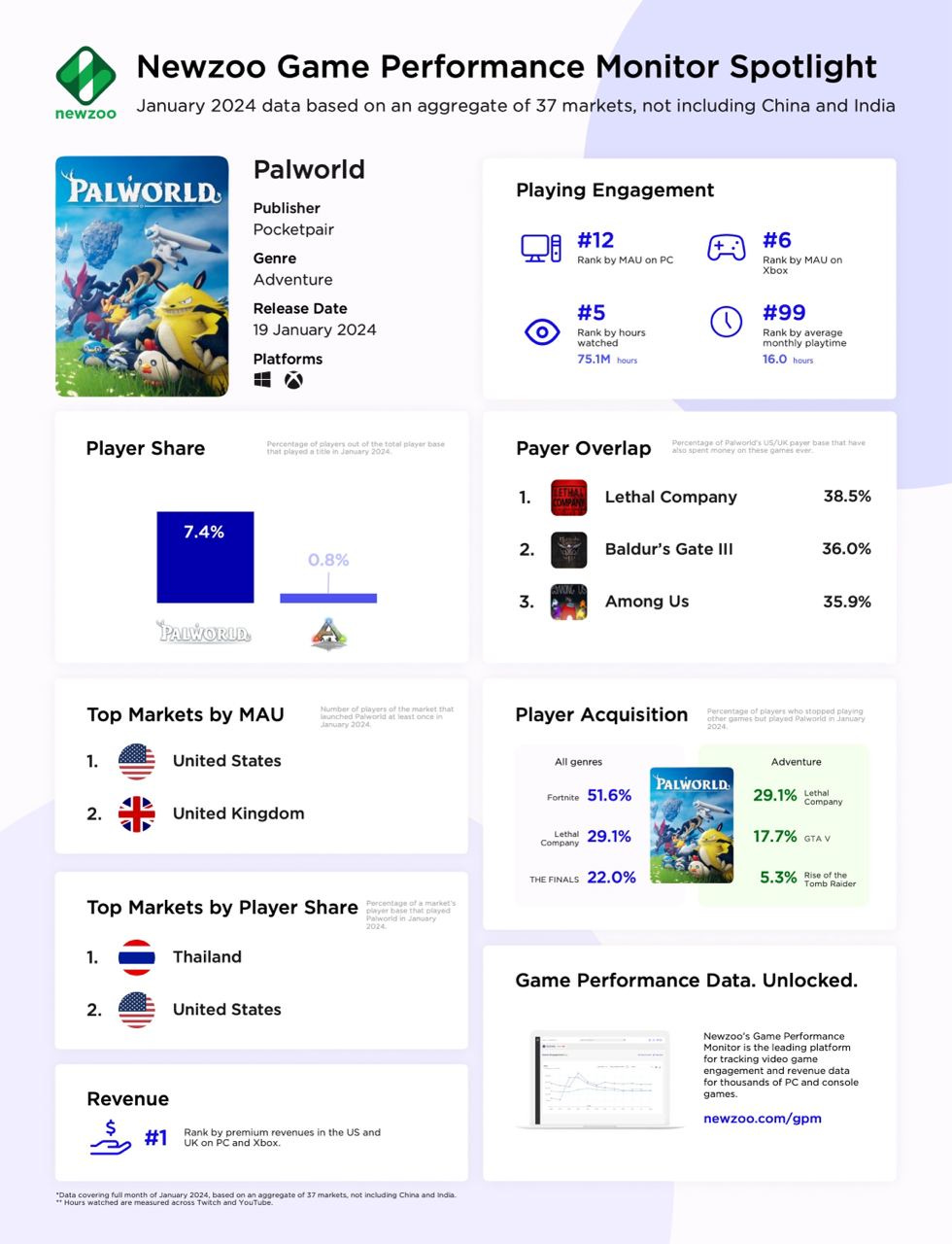

Newzoo: Palworld in January 2024

The game was released on January 19, 2024. Within the first 13 days, the game was purchased by more than 12 million people. Newzoo considers 37 countries excluding China in its report.

In January 2024, Palworld became the 11th game by MAU on PC and Xbox. Among adventure games, it ranks second.

7.4% of the gaming audience on PC and consoles played Palworld. On average, they spent 16 hours in the game.

Palworld was watched for over 75 million hours on Twitch and YouTube. It ranks second among adventure games and fifth among all games.

Palworld became the best-selling paid game in the USA and the UK. 38.5% of those who bought the game also purchased Lethal Company.

29.1% of those who stopped playing Lethal Company in January 2024 switched to Palworld. Additionally, 51.6% of those who stopped playing Fortnite and 22% of The Finals audience joined the game.

The USA and the UK are the main markets by MAU for Palworld. If we consider the percentage coverage of countries, the leaders are the USA and Thailand.