Weekly Gaming Reports Recap: November 6 - November 10 (2023)

The game investment market in Q3 2023 continues to struggle; Mistplay released a report about players' behavior in 2023; Newzoo shared insights into the IP/brand collaborations in games since 2021.

Reports of this week:

The audience of EA Sports FC 24 reached 14.5 million players in the first month

Omdia: Gaming subscriptions will grow to $22 billion by 2027

Sensor Tower: The Mobile Gaming Market in South Korea in 2023

SNJV: The State of the French Gaming Industry in 2023

Drake Star: The State of the Video Game Investment Market in Q3 2023

Mistplay: North American players behavior in Mobile Games in 2023

Sony: Over 46.6M PS5 units are sold worldwide

Newzoo: IP & Brand Collaborations in Games in 2023

Axios: 2023 is already a record year for games with 90+ ratings on Metacritic

The audience of EA Sports FC 24 reached 14.5 million players in the first month

Such a number of players was achieved on PC and consoles. EA notes that the numbers in terms of attracting a new audience are in the double digits.

The launch of FC Mobile set a record for the football franchise. Over 2 million users installed the game on the first day, over 5 million within the first 3 days, and over 11 million within the first 10 days.

Based on the results of September (the game was released on September 29), EA Sports FC 24 became the 14th best-selling game of the year.

💬 EA speaks positively about the launch results after parting ways with FIFA. The company expects that EA Sports FC 24 will show a slight increase in sales compared to FIFA 23.

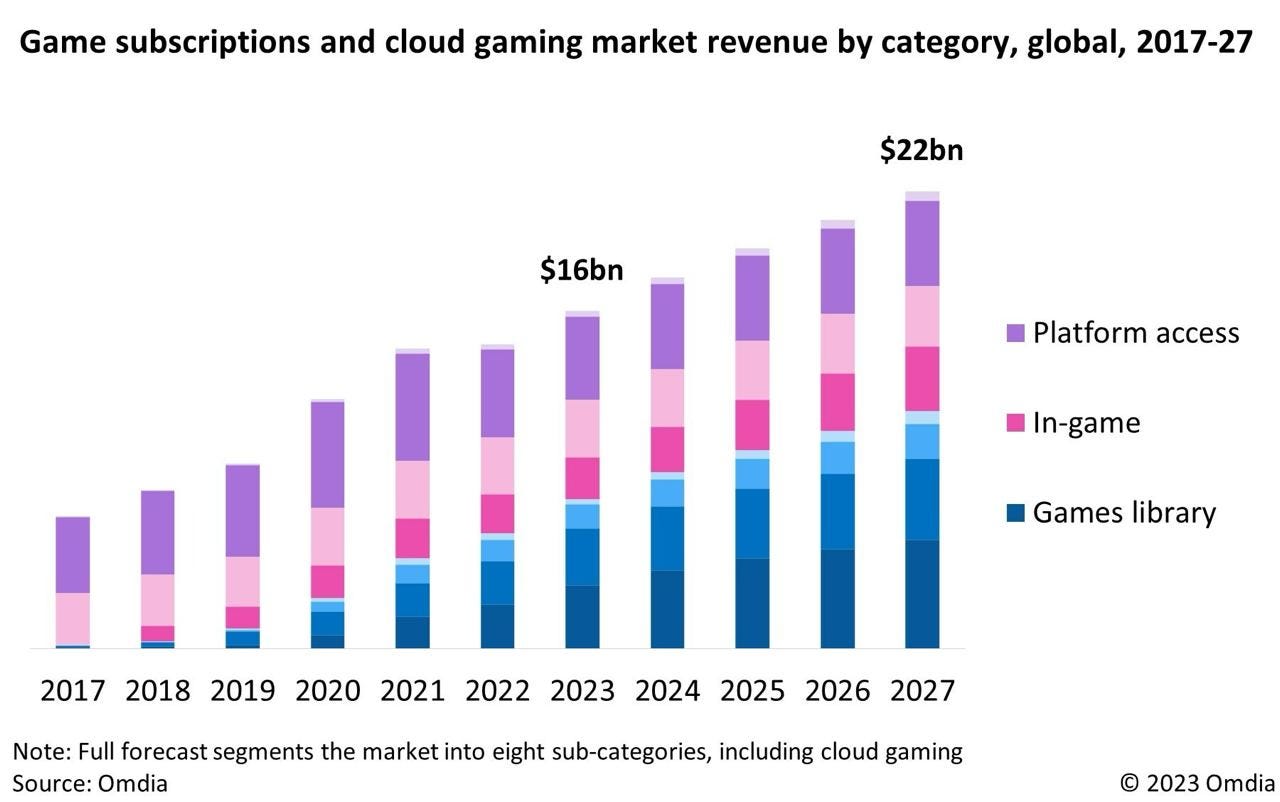

Omdia: Gaming subscriptions will grow to $22 billion by 2027

: Xbox Game Pass, PlayStation Plus, Nintendo Online | WIRED")

It is expected that by 2027, subscription services will account for 11.6% of the total gaming industry revenue.

The number of paying subscribers is projected to increase to 217 million by 2027, according to Omdia's forecasts, with 175 million by the end of 2023.

By the end of 2023, the revenue generated by subscription services will amount to $16 billion.

Omdia includes several types of offerings in subscription services:

Game library services (Xbox Game Pass, Netflix, advanced versions of PlayStation Plus subscriptions) are expected to account for 44% of total revenue in 2023 ($7.3 billion).

In-game subscriptions make up 30% of total revenue ($4.8 billion).

Subscriptions for access to platform functionality (online gaming) contribute 26% of total revenue ($4.3 billion).

Services offering cloud gaming are projected to earn $3.6 billion in 2023, with this figure increasing to $6.4 billion by 2027. Growth will be driven by subscriptions like Xbox Game Pass Ultimate and PlayStation Plus Premium.

The average annual growth rate of subscription services will be 6.58%.

Currently, Microsoft and Sony are the leaders in the subscription business, with a combined total of 51 million paying users.

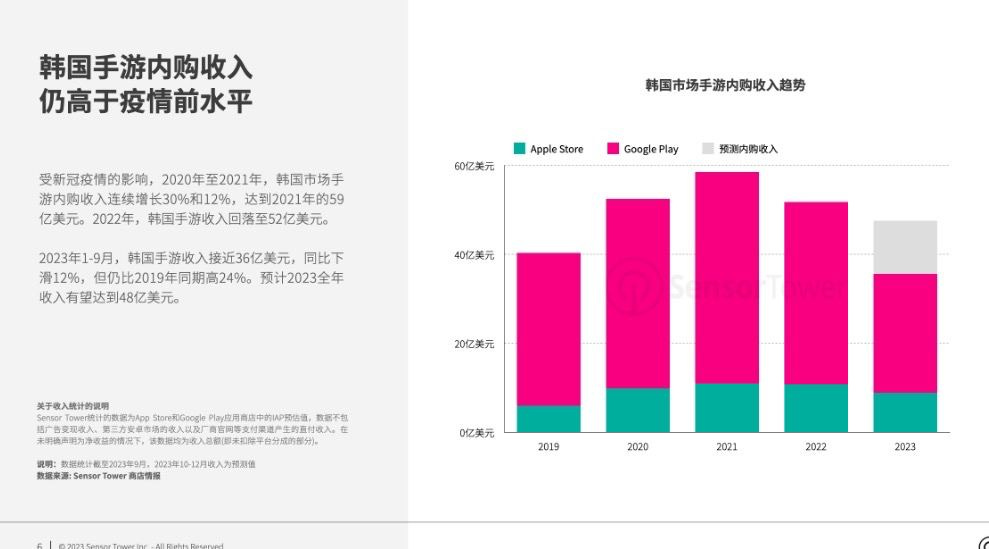

Sensor Tower: The Mobile Gaming Market in South Korea in 2023

The total volume of the mobile gaming market in South Korea in 2023 will reach $4.8 billion. 42% of this amount will be earned by foreign companies, most from China.

From January to September of this year, the mobile revenue of the South Korean market amounted to $3.6 billion. This is 24% more than in the same period in 2019.

The highest revenue the South Korean market reached was in 2021 - $5.9 billion.

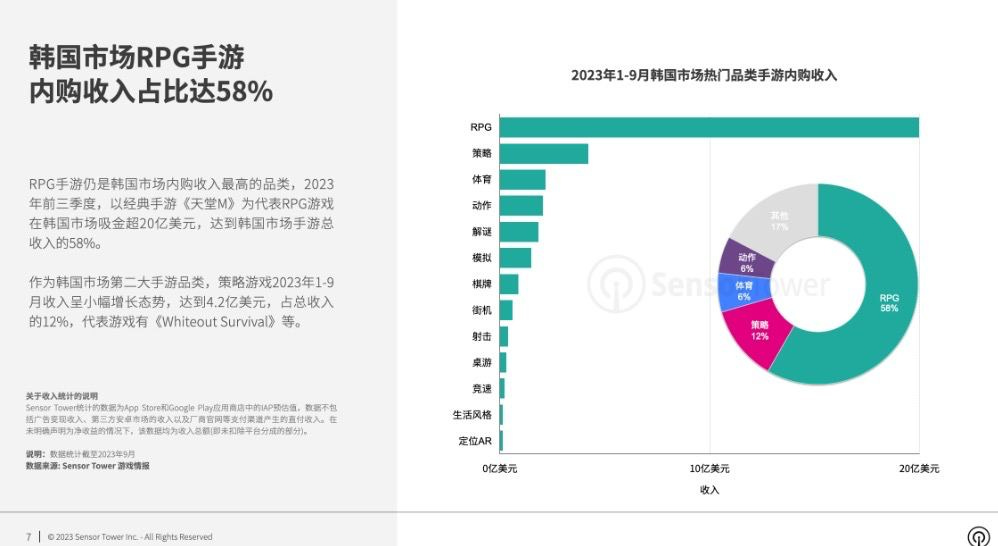

Key Genres

RPG is the main genre in South Korea. In 2023, it accounted for more than 58% of the total revenue ($2 billion).

Strategy games are in second place with $420 million (12% of the total).

Most Successful Games

From January to September 2023, Lineage M earned the most, almost $300 million.

The fastest-growing in terms of revenue is Night Crows - $130 million, a new MMORPG by Wemade.

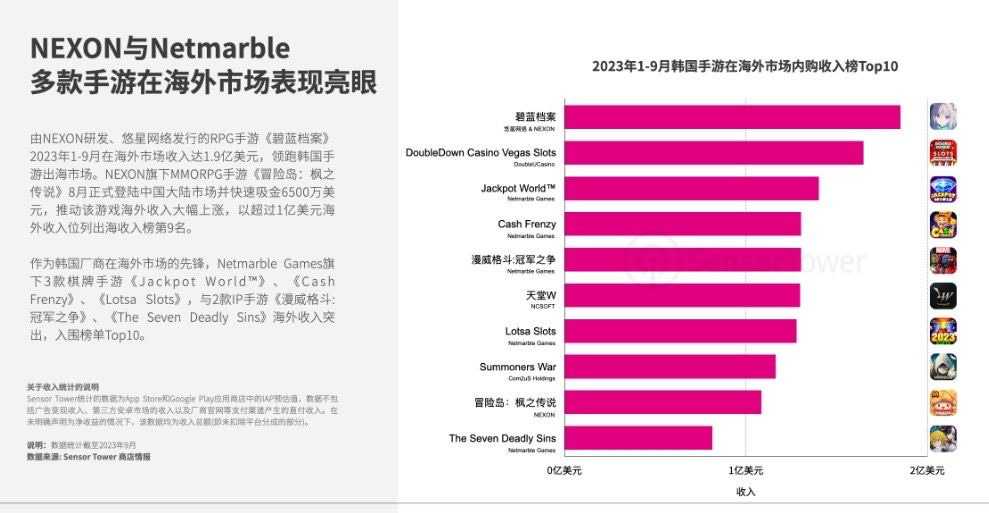

Results of South Korean companies on global markets

Blue Archive by Nexon ($190 million), DoubleDown Casino Vegas Slots by DoubleUCasino, and Jackpot World by Netmarble Games are the most profitable games from South Korean developers in international markets.

Netmarble Games invested over $40 million in promoting Jackpot World in just the first 3 quarters of 2023.

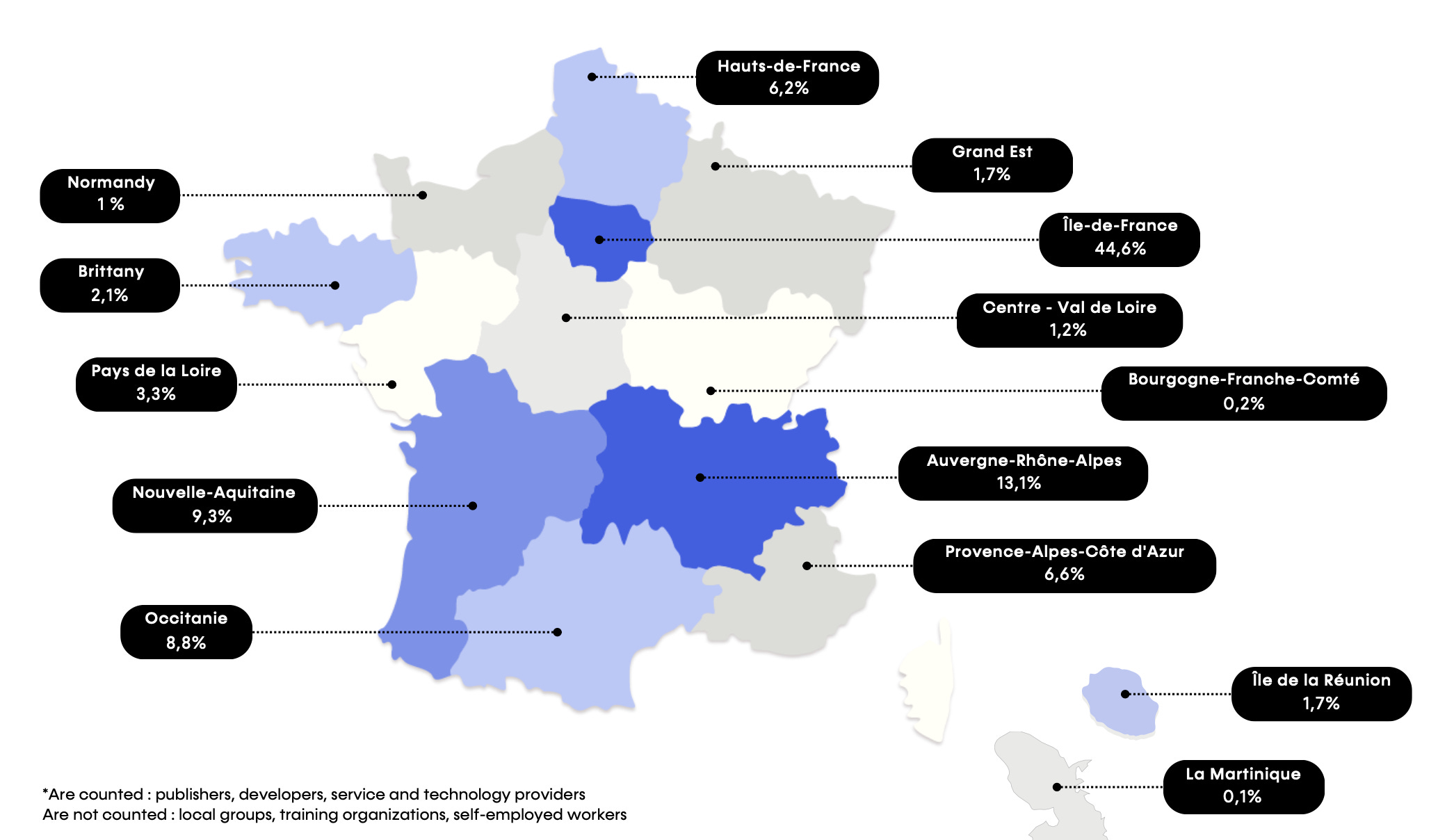

SNJV: The State of the French Gaming Industry in 2023

The survey was conducted from February 28, 2023, to June 26, 2023. It involved 577 French gaming companies and mainly covers the results of 2022.

In France in 2022, there were over 1,000 gaming companies, of which 580 were game developers.

In France, 1,257 new games are being developed, with 854 of them being new IPs (intellectual properties).

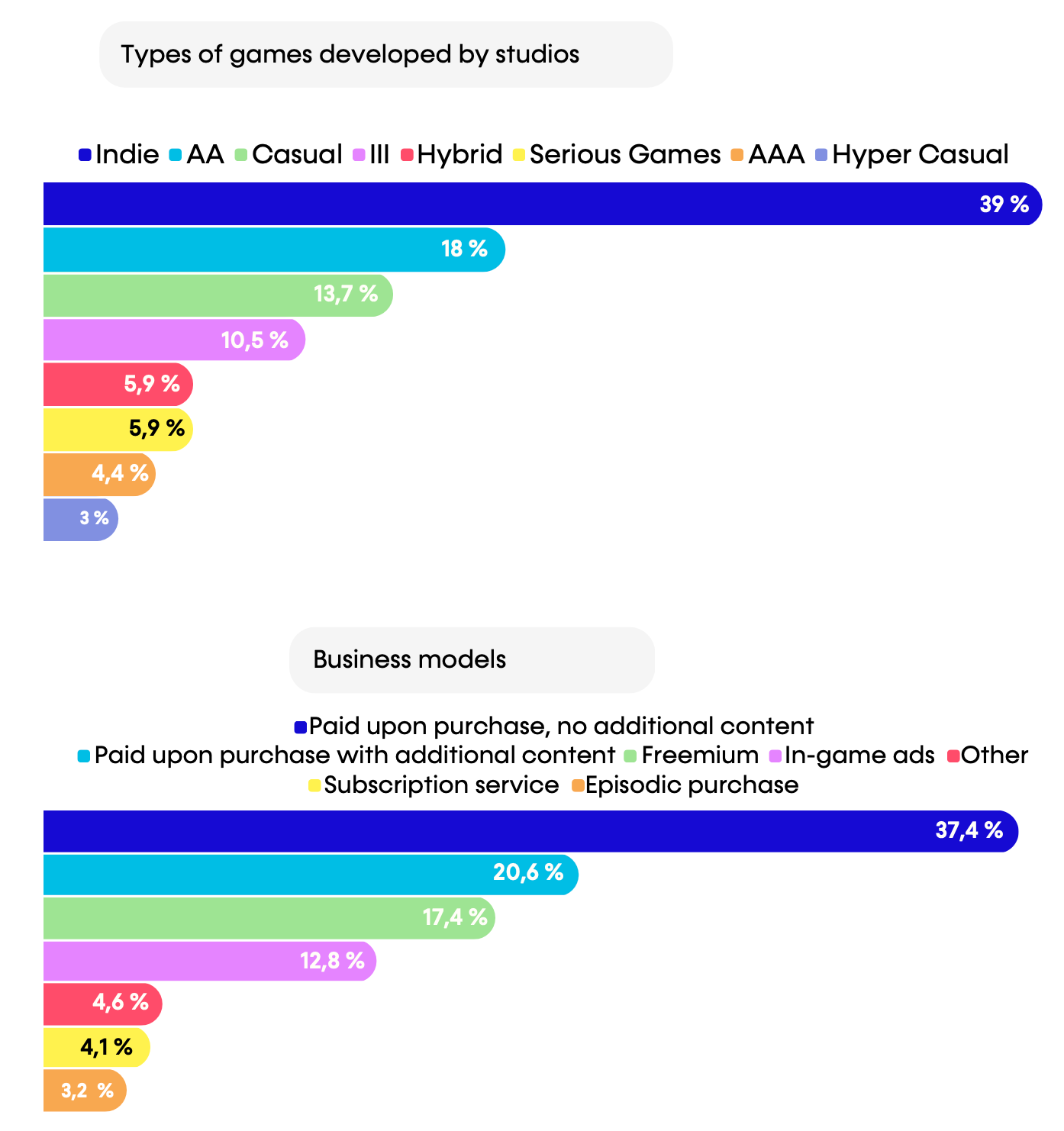

39% of games in development are indie projects, and 4.4% are large-budget AAA games.

37.4% of games are planned to be distributed using the B2P (Buy to Play) model without in-game payments. Another 20.6% will use the B2P model with in-game payments.

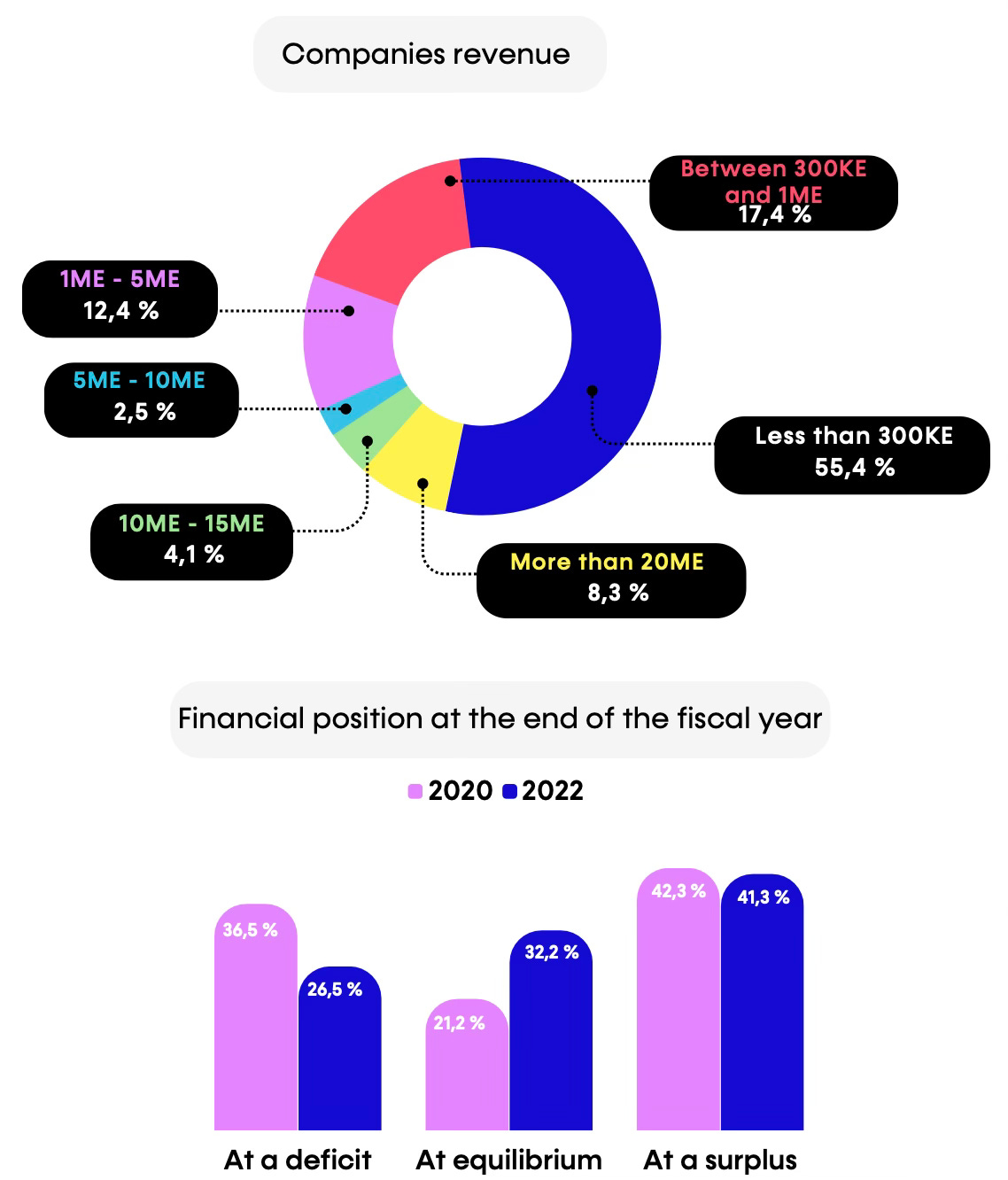

67.2% of games in development have a budget of less than €1 million, while 6.9% have budgets exceeding €10 million.

7% of developers take more than 4 years to create a game, while the majority (60.6%) complete their games in 1 to 3 years.

Hiring

In 2023, between 400 and 600 new job vacancies will be opened in French game studios. 24% of the current workforce in companies are women.

52% of studios plan to hire in 2023, 40% want to retain their employees, and 7.5% plan layoffs.

33% of French companies have implemented a full remote workday, and 47.5% offer a hybrid work model.

Financial Situation

27% of studios have crossed the €1 million mark in annual revenue.

8.3% of French studios have earned more than €20 million, while the majority (55%) earn less than €300,000 per year.

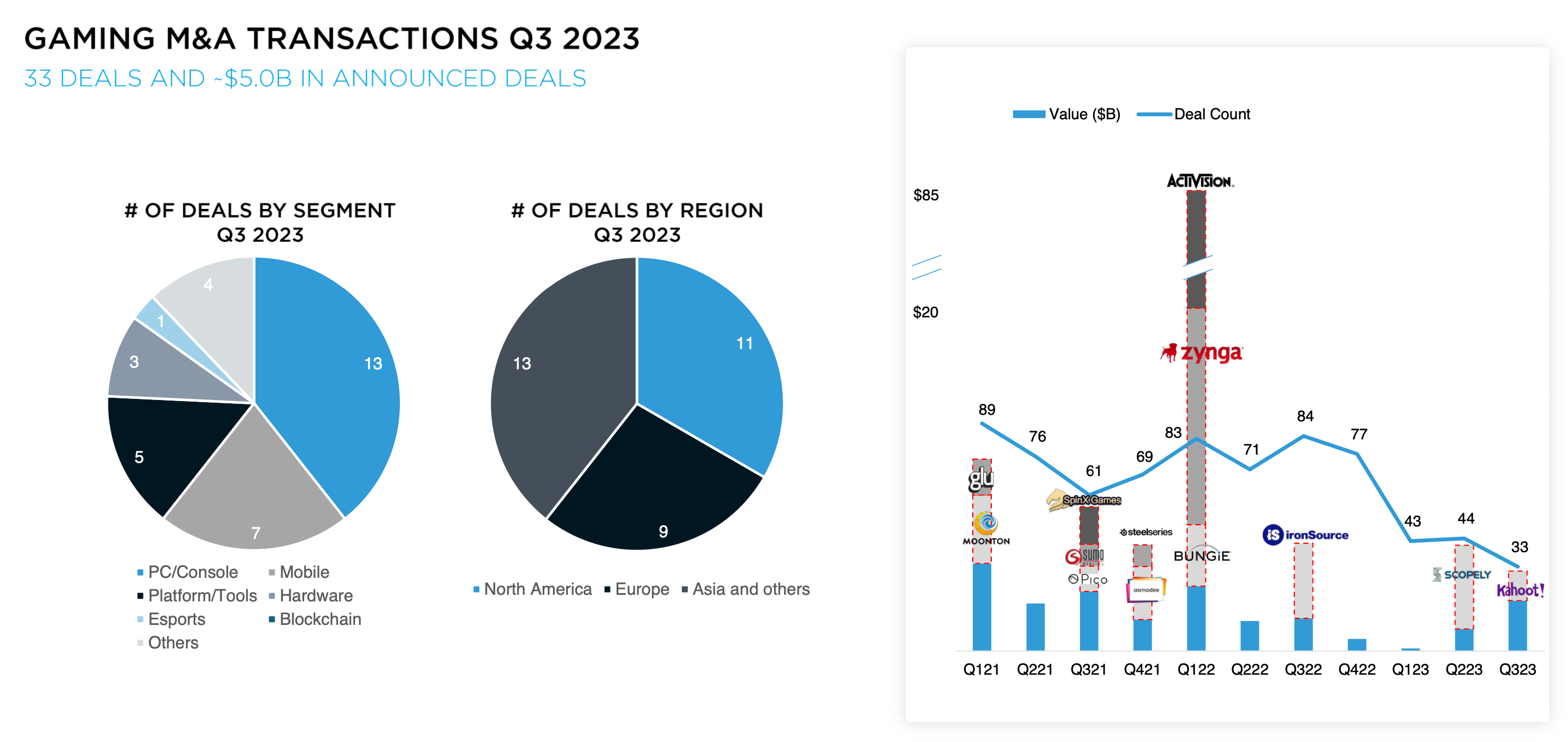

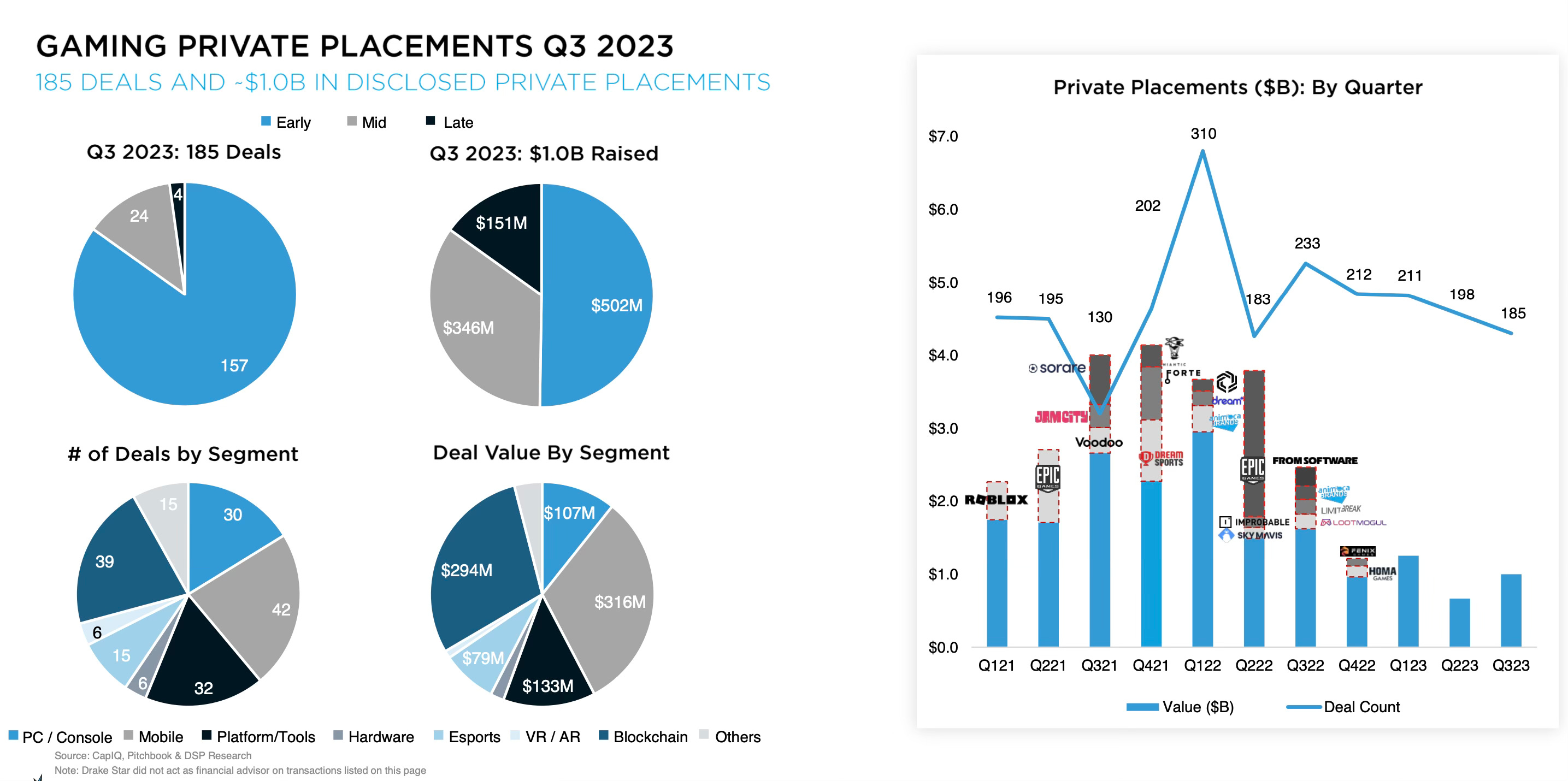

Drake Star: The State of the Video Game Investment Market in Q3 2023

In the third quarter, 33 M&A deals were announced with a total value of $5 billion. One such deal, worth $1.72 billion, was the acquisition of Kahoot!, an interactive learning platform. This deal has an indirect connection to games.

Among other significant deals, Playtika acquired Youda Games and Innplay Labs for $465 million; Tencent acquired Techland and Visual Arts; Sumo Group acquired Midoki; Supercell acquired a majority stake in Ultimate Studio; Capcom acquired Swordcanes Studio.

In the third quarter, private investments decreased to 185, with a total transaction volume of $1 billion.

In terms of the number of transactions, this is the lowest figure since the second quarter of 2022. In terms of volume, the only lower quarter in the last 2.5 years was the second quarter of 2023.

Among the most notable deals of this quarter are a $100 million investment in Candivore by Haveli Investments; a $90 million investment in Second Dinner by Griffin Gaming Partners and NetEase; and a $54 million investment in Story Protocol by a conglomerate of investors led by Andreessen Horowitz.

Bitkraft, Andreessen Horowitz, and Play Ventures are the most prominent funds of 2023 at the moment.

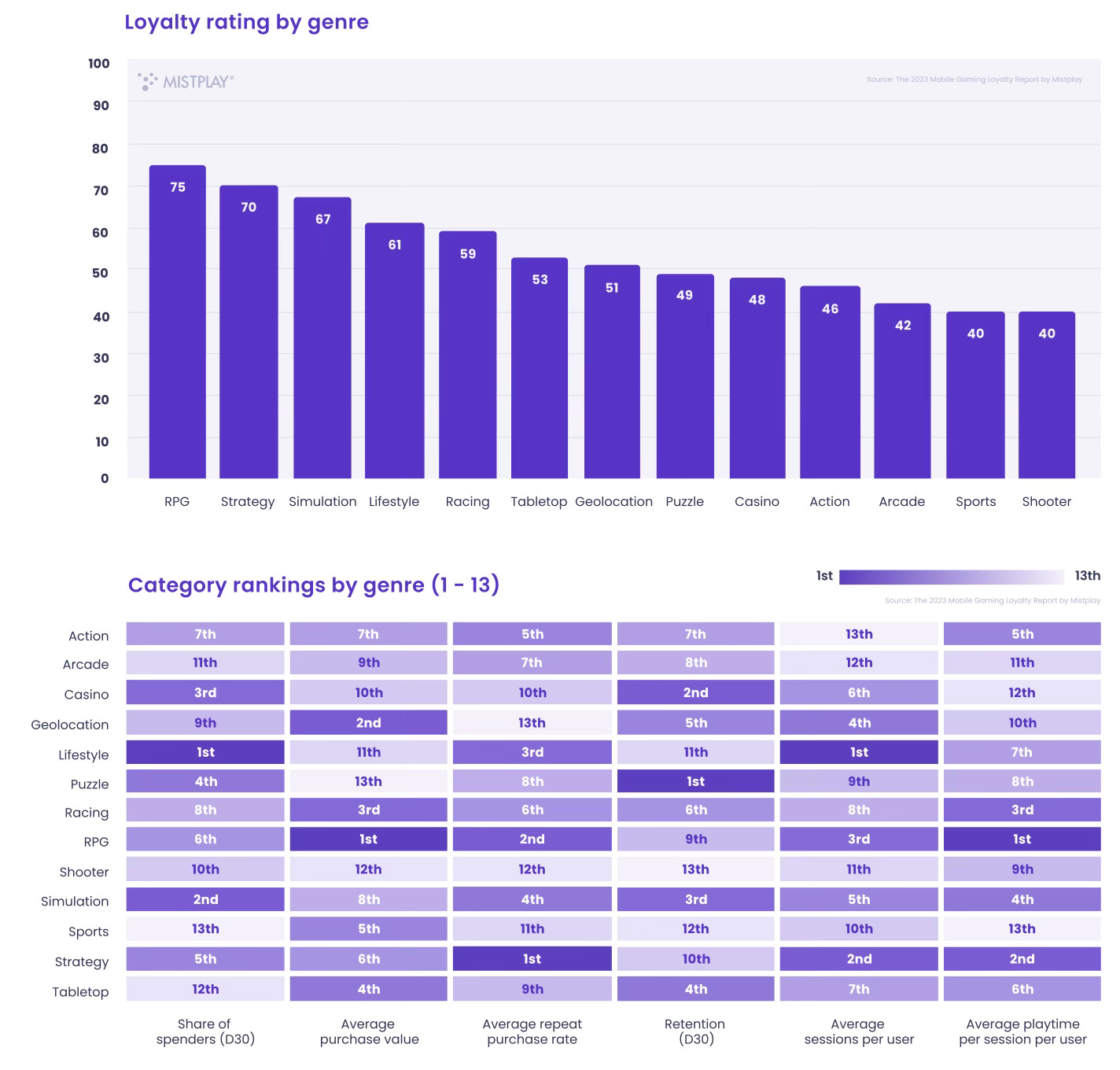

Mistplay: North American players behaviour in Mobile Games in 2023

The Mistplay Loyalty Index is based on several monetization indicators (the share of paying users in 30 days; average spending; average frequency of repeat purchases) and engagement (30-day retention; average number of sessions per user; average session duration).

The survey involved more than 3,000 mobile gamers aged 18 and older from the USA and Canada. The survey was conducted among Mistplay users in the third quarter of 2023.

Genre Overview

RPG, strategy, and simulation games have the most loyal audience. RPG games lead in average spending and average session duration.

Lifestyle projects have the highest number of paying users in 30 days. Strategies have the highest repeat purchase rate among all genres. RPGs, as mentioned earlier, lead in average spending.

Puzzle games are the strongest genre in D30 retention; RPGs lead in the average number of sessions per user; Lifestyle projects lead in average session duration.

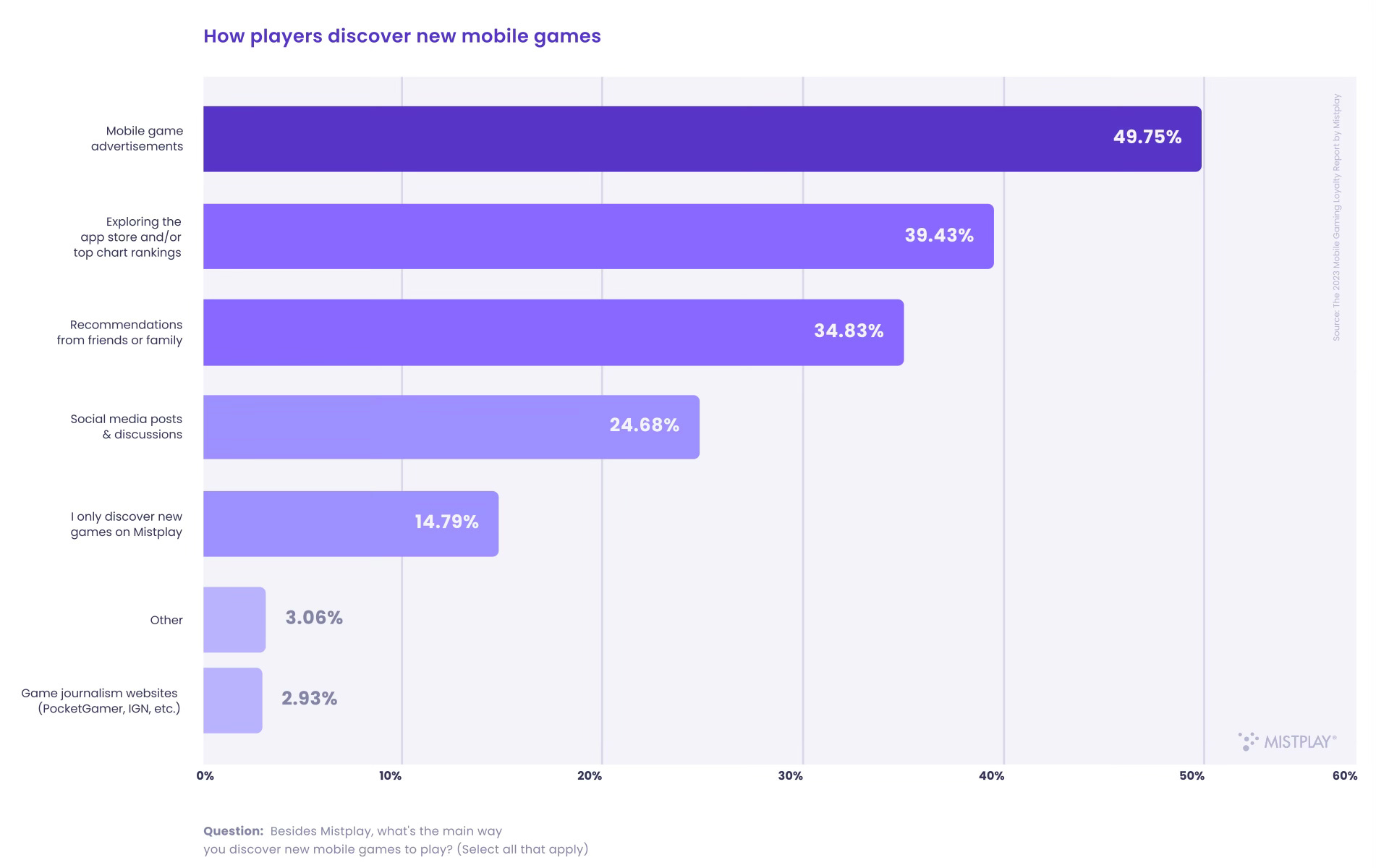

User Interaction with Advertising and Game Installation

49.75% of users discover new games through advertising; 39.43% find them through app stores and top charts; 34.83% rely on recommendations from friends.

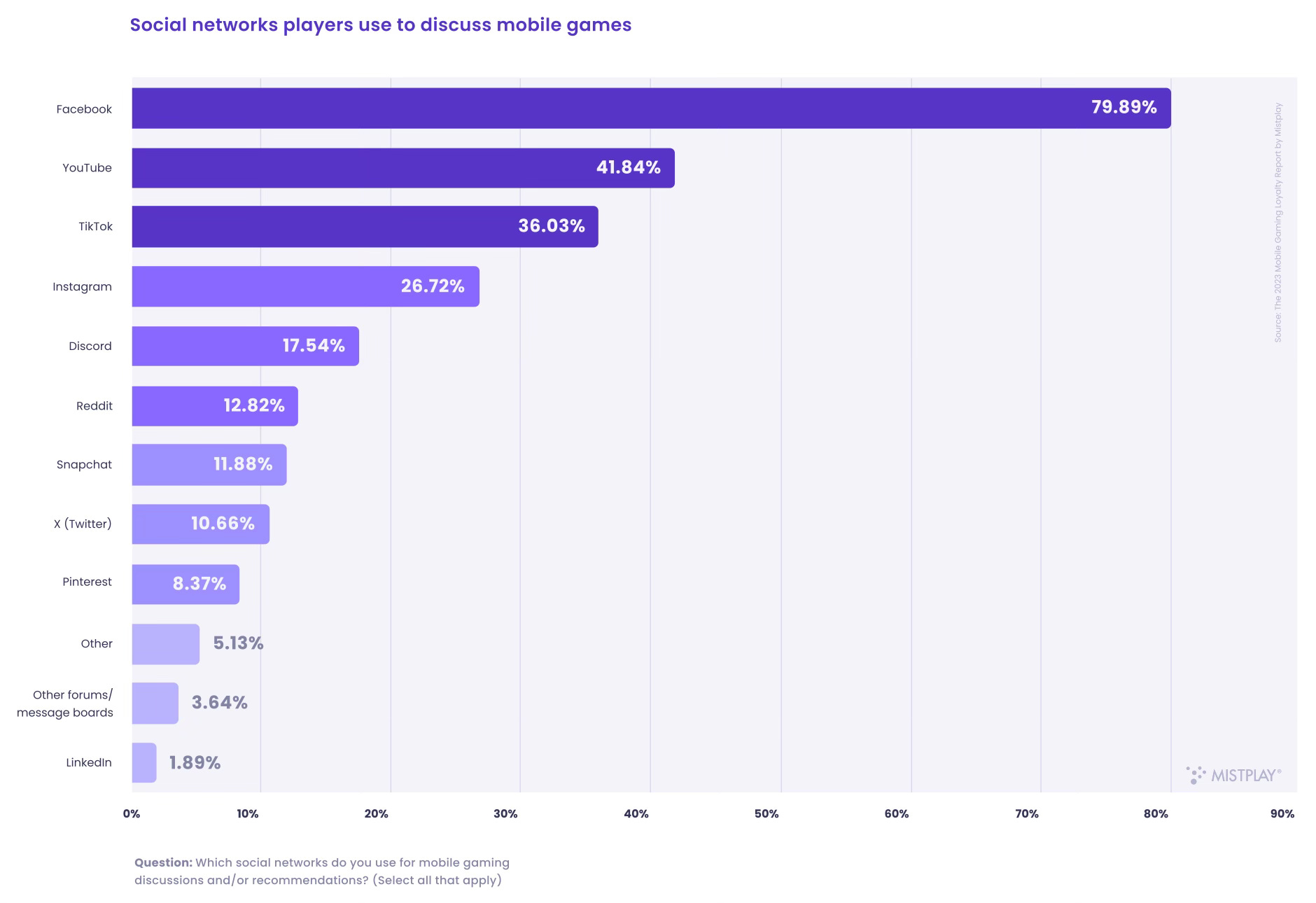

Facebook (79.89%), YouTube (41.84%), TikTok (36.03%) are the main platforms where players discuss mobile games.

36.7% of players do not interact with advertising at all, preferring to ignore it or hide it.

68.3% of users are willing to install a new game after seeing an ad within the first few weeks. 21.7% fundamentally do not install games they see in ads.

44.6% of the audience is satisfied with a 3-star app rating. 29.95% do not install apps with a rating below 4 stars; 6.36% only want to see a 5-star rating.

User Motivation

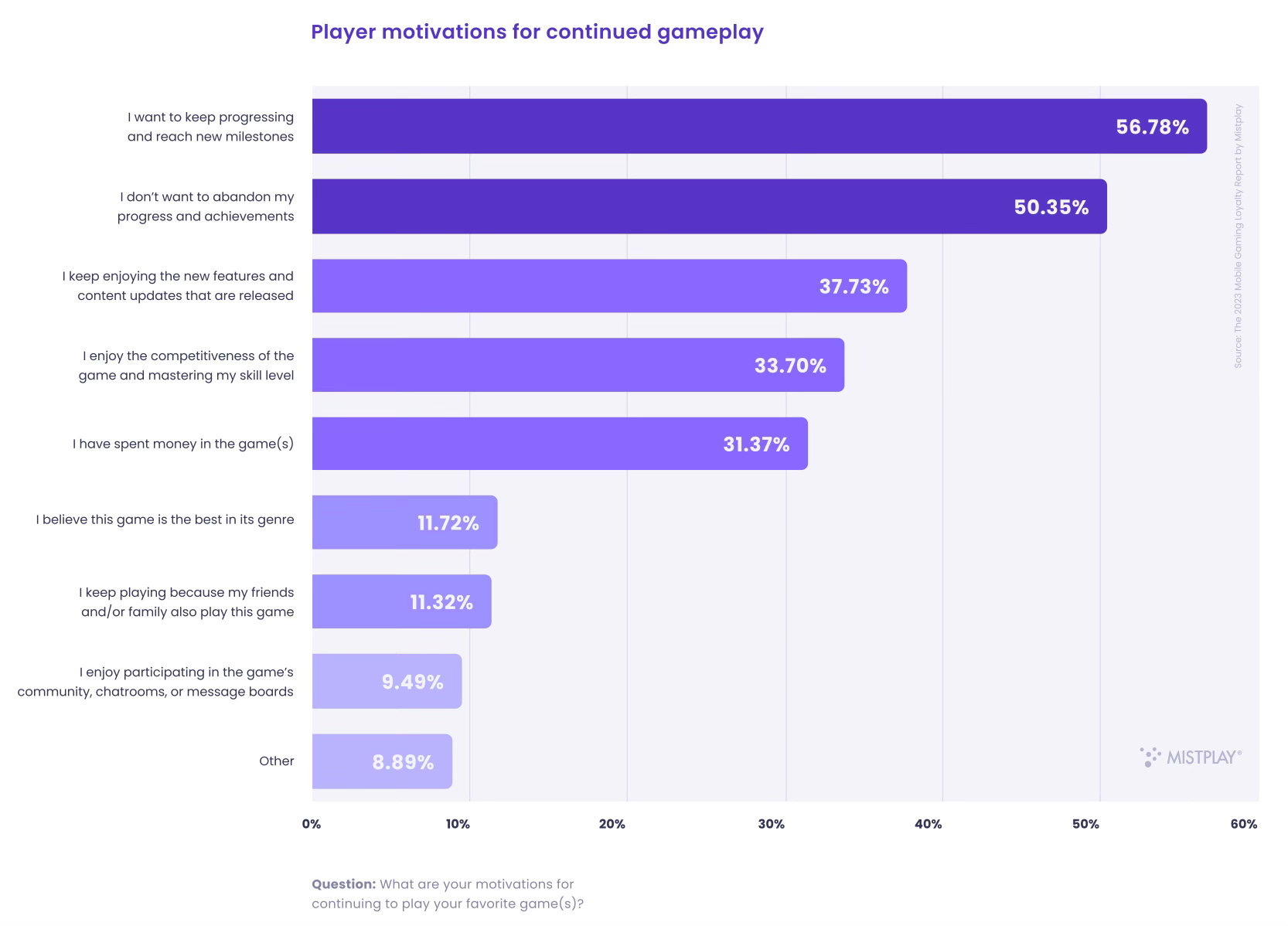

56.78% of players continue playing for progress and achieving new results; 50.35% do not want to lose their accumulated progress and achievements; 37.73% like new updates and content.

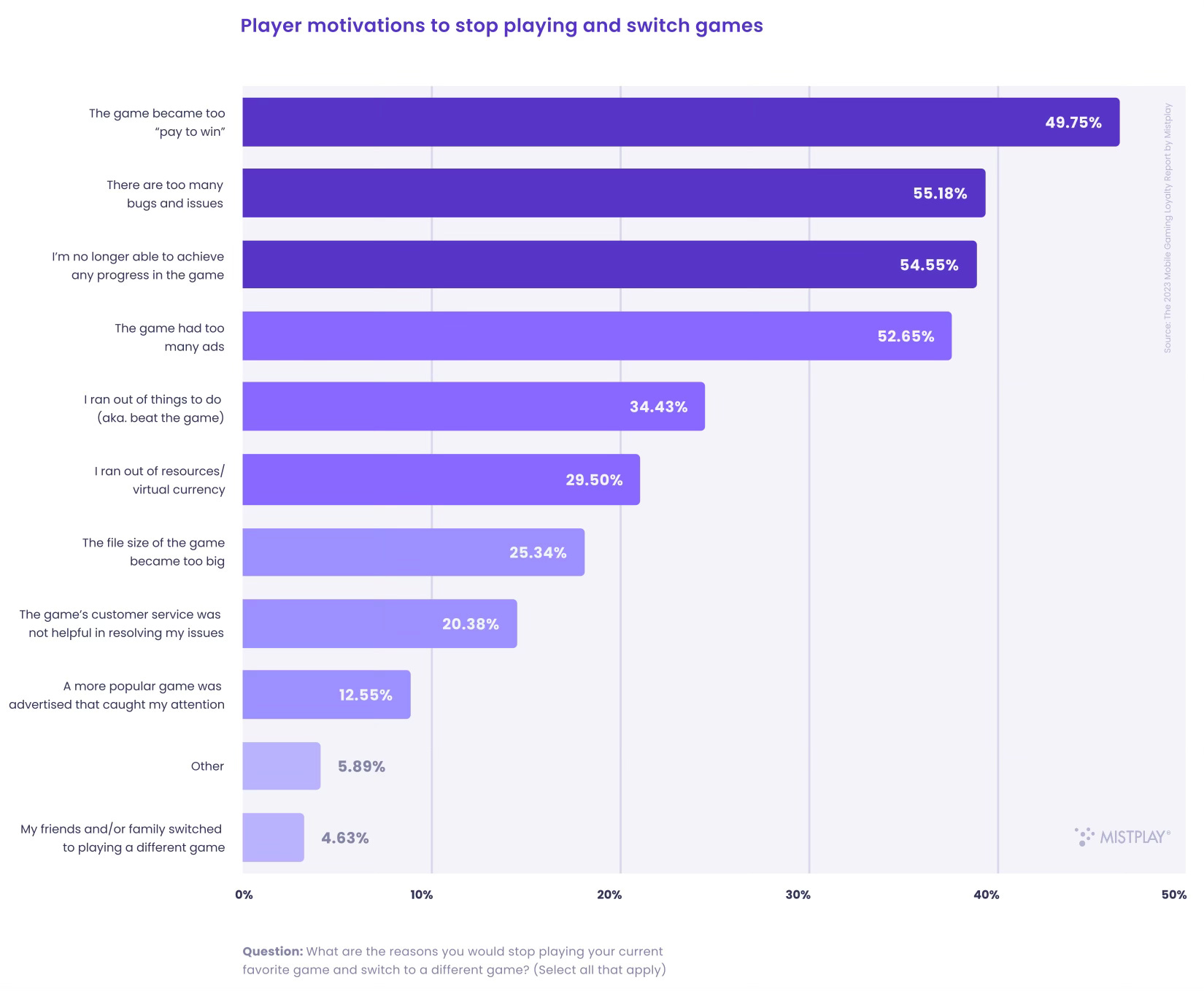

On the other hand, 59.75% of users stop playing because the game becomes "pay to win"; 55.18% quit due to bugs or errors; 54.55% do not feel a sense of progress.

25.64% of people will not leave the game if there is a bad update, knowing that the issue will be fixed. On the contrary, 4.7% will stop playing immediately. The majority, around 70%, is willing to give the game from 1-3 days to 2 months to fix issues.

The publisher's name is important to players. On a scale from 1 to 5, only 6.39% of players chose a rating of 1 or 2, which means that survey participants are unlikely to try games from the same publisher.

Player Purchasing Preferences

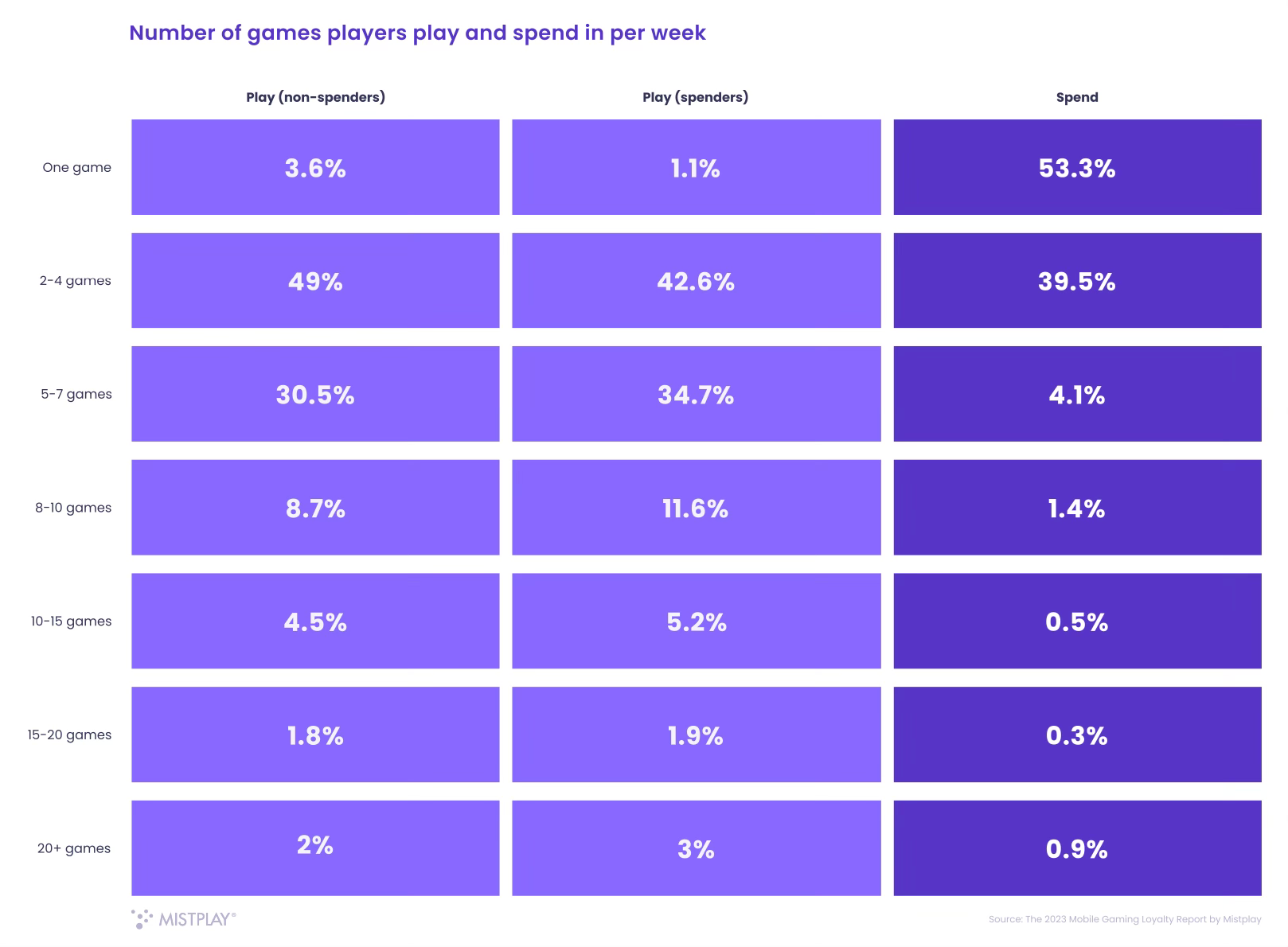

92.8% of the paying audience simultaneously makes purchases in 1-4 projects. 53% spend on only one game per week.

61.96% of users spend money to achieve new progress; 30.71% for rare or unique content; and 29.27% to play without ads.

59.55% of players prefer bundles with a larger number of items; 45.95% prefer one-time profitable offers; 28.64% want to buy in-game currency to spend as they see fit.

Sony: Over 46.6M PS5 units are sold worldwide

Sony reported on the second financial quarter of 2023 and shared some new figures.

Over 46.6 million PlayStation 5 units have been sold worldwide. 4.9 million of them were sold from July to September of this year.

The company predicts that the sales momentum will only accelerate with the release of the Slim version of the PS5 and PlayStation Portal. The maximum target is to sell 25 million PlayStation 5 units in this fiscal year. Currently, the PS5 is performing 25% better than the year when the PS4 sold 20 million consoles.

During the second financial quarter of 2023 (July-September), 67.6 million games for PS4 and PS5 were sold. This is 7.5% more than in the same period in 2022.

4.7 million copies sold were games from Sony's studios, which accounts for 7% of the total.

Sales of Marvel’s Spider-Man 2 exceeded 5 million copies. The game achieved this milestone in just 11 days. Only God of War: Ragnarok reached this mark faster (5 days). God of War (2018) took 31 days to reach it, and Ghost of Tsushima took 118 days.

MAU on PlayStation platforms reached 107 million in September, which is 5 million more than in September of the previous year. On the other hand, this is 1 million MAU less than in the peak month of the first financial quarter of 2023. But such comparisons should consider seasonality.

Sony noted that it has halved its plan to release game services. By March 2026, there should be 6 of them, not 12 as previously planned. The company has decided to focus on quality rather than quantity.

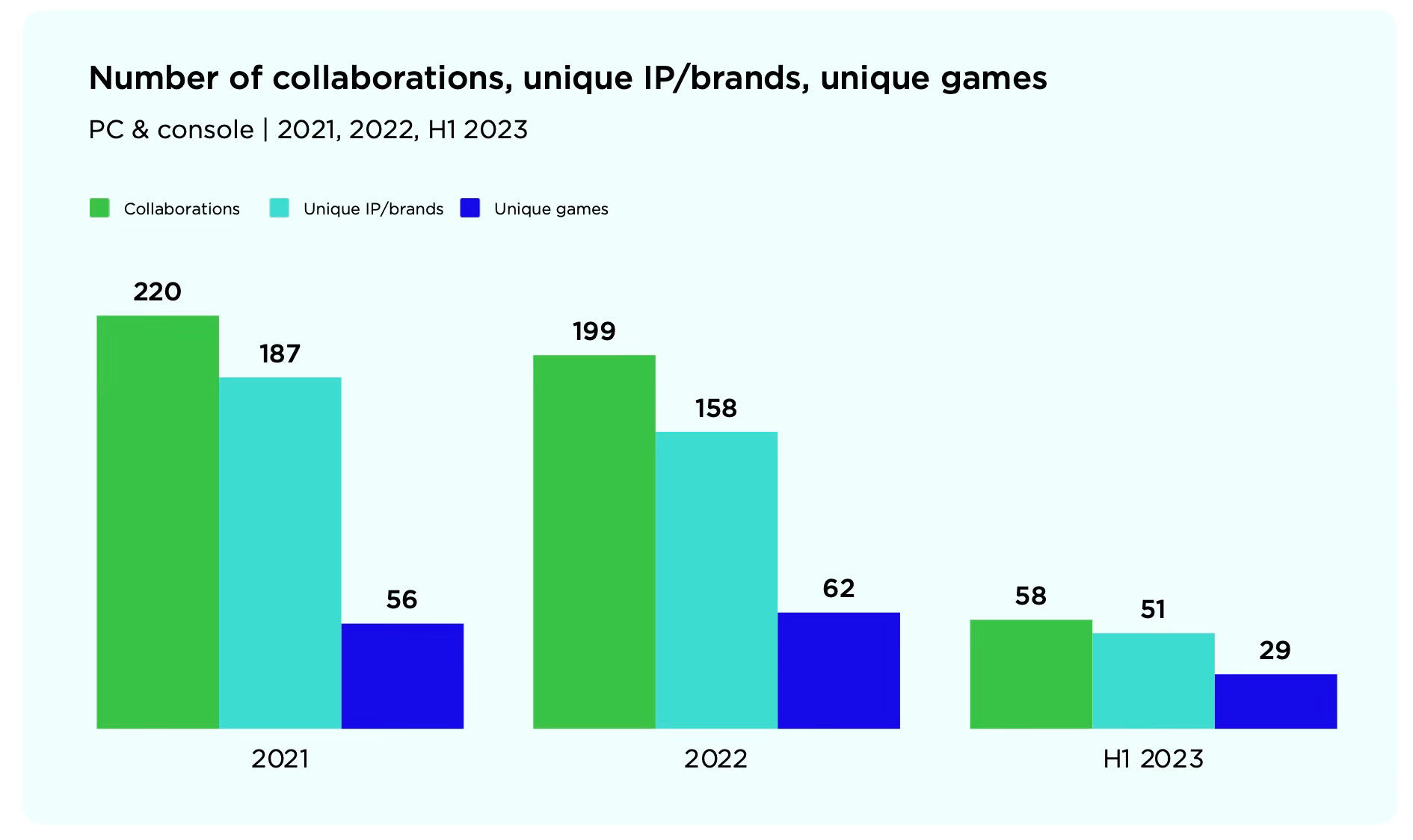

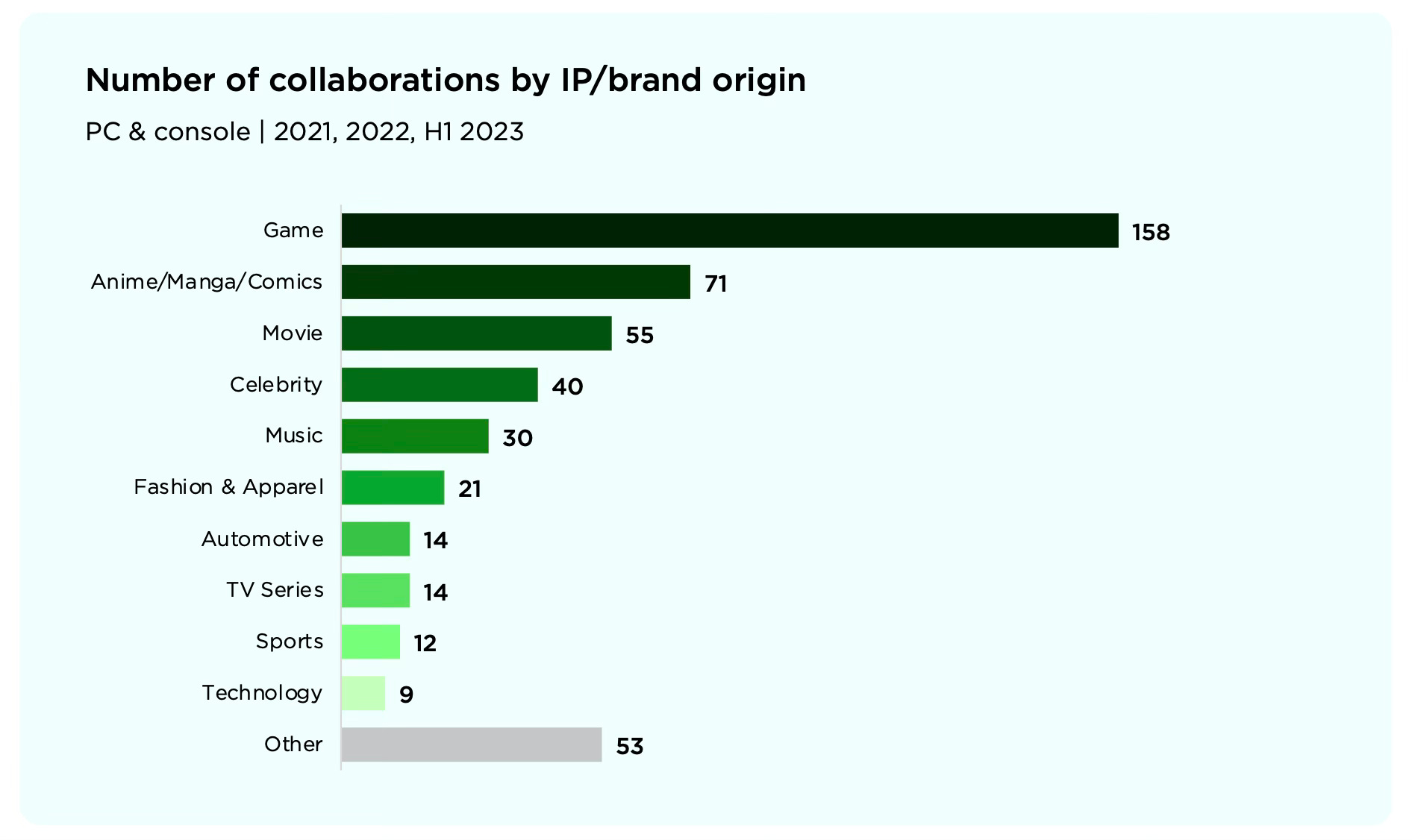

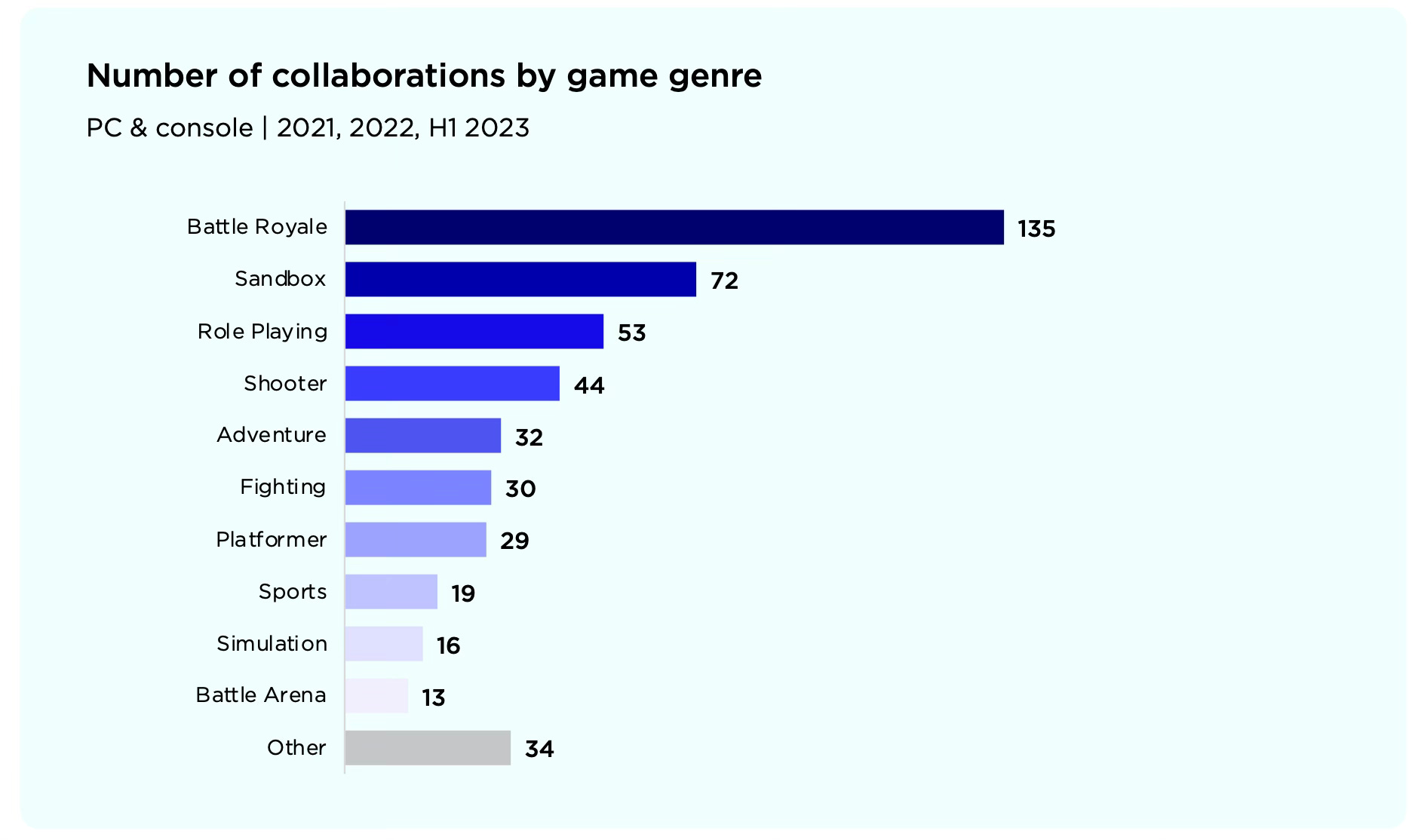

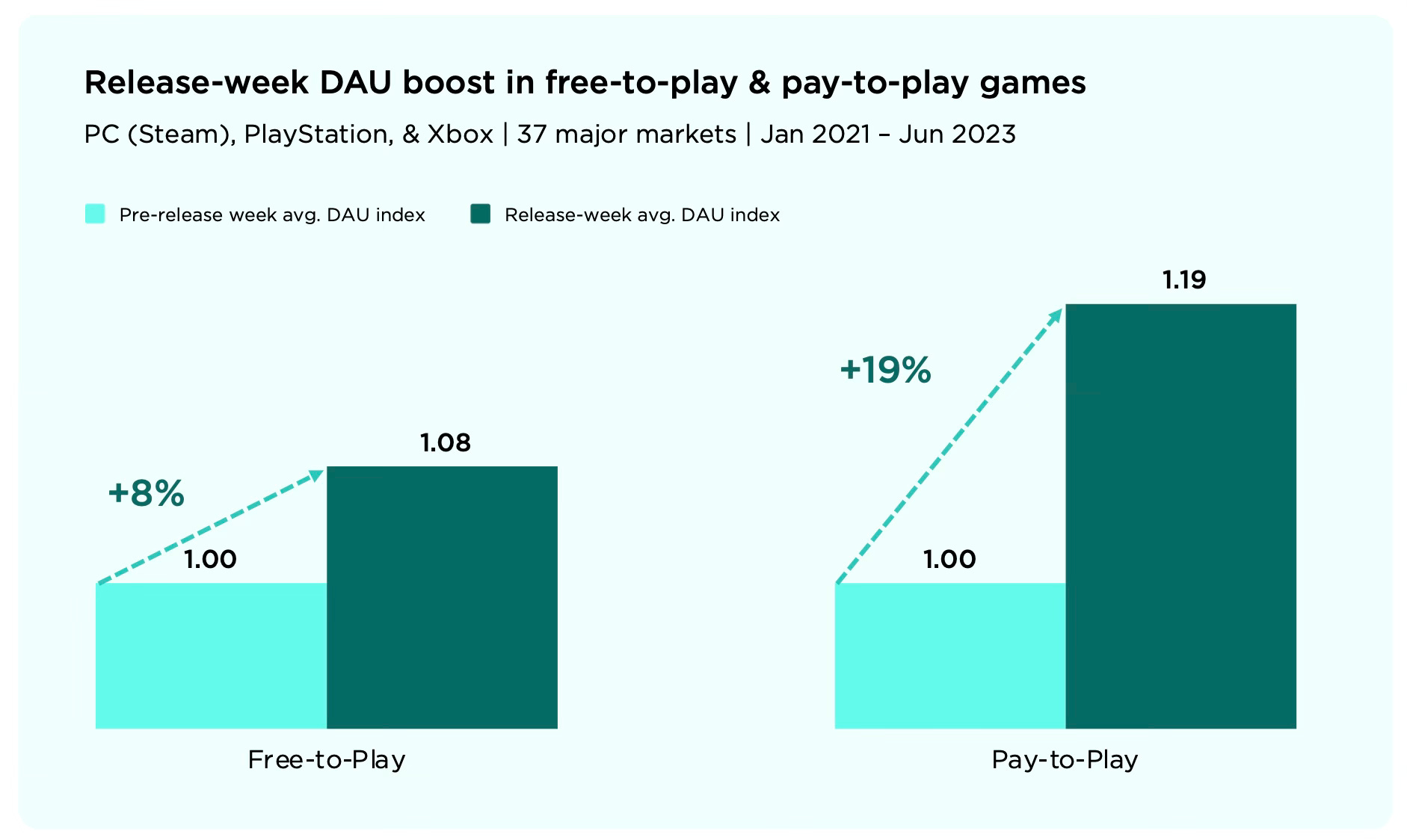

Newzoo: IP & Brand Collaborations in Games in 2023

The company examined 477 integrations from January 2021 to June 2023 as part of its research.

The number of collaborations and joint projects has been decreasing since 2021, attributed to the deteriorating situation in the gaming market.

158 out of 477 integrations were between gaming IPs. In second place were anime (manga) with 71 cases, followed by movies with 55 cases.

Battle Royale is the most popular genre for collaborations, accounting for 135 out of the 477 cases studied. Sandbox games rank second with 72 collaborations, and RPGs are third with 53.

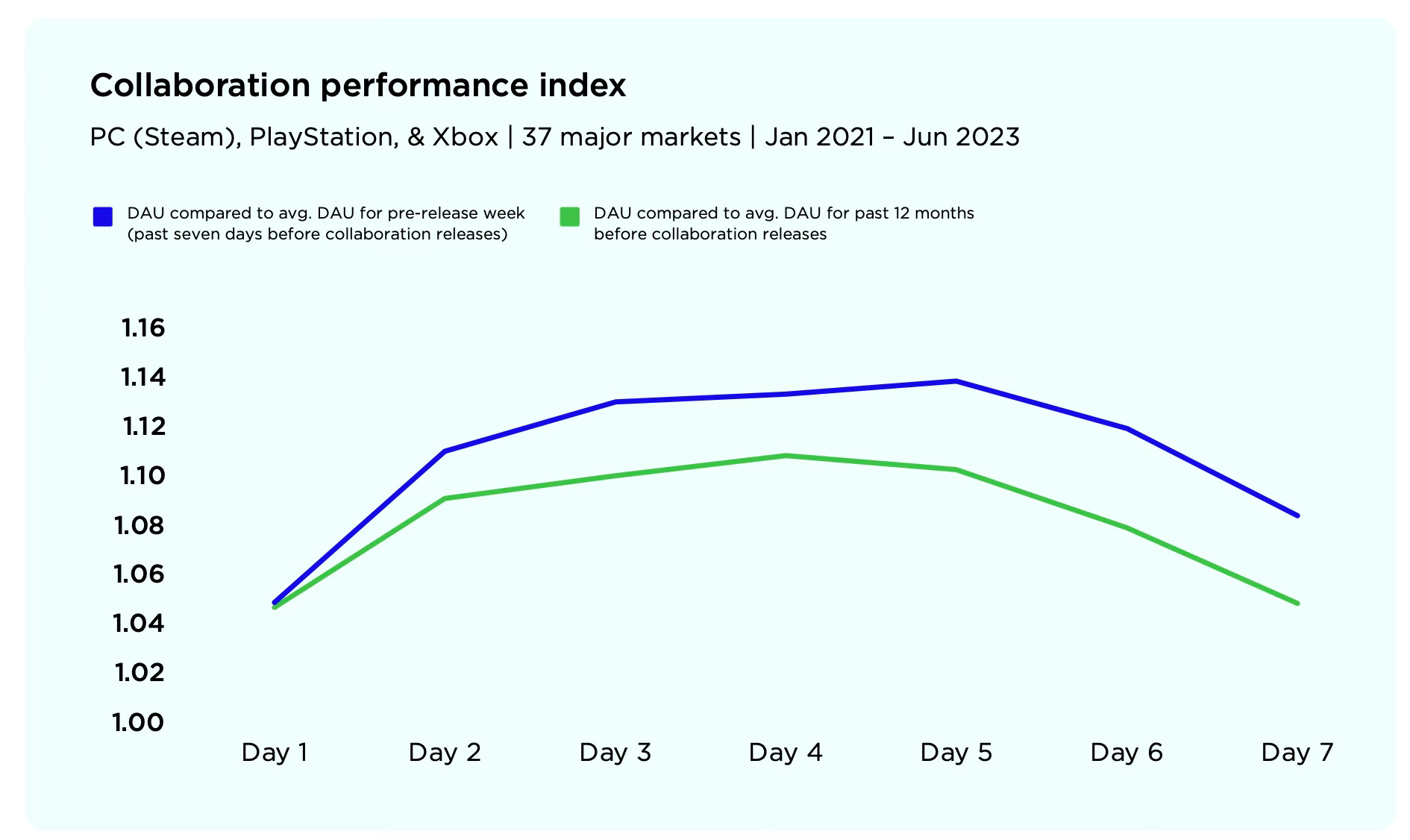

The average growth in Daily Active Users (DAU) during the first 7 days after collaboration is 11%, peaking on the 4th or 5th day after release. However, Newzoo does not assess the monetization results.

The effect is more noticeable for games distributed under the buy-to-play model, with a 19% increase in DAU. Free-to-play projects experience an 8% growth.

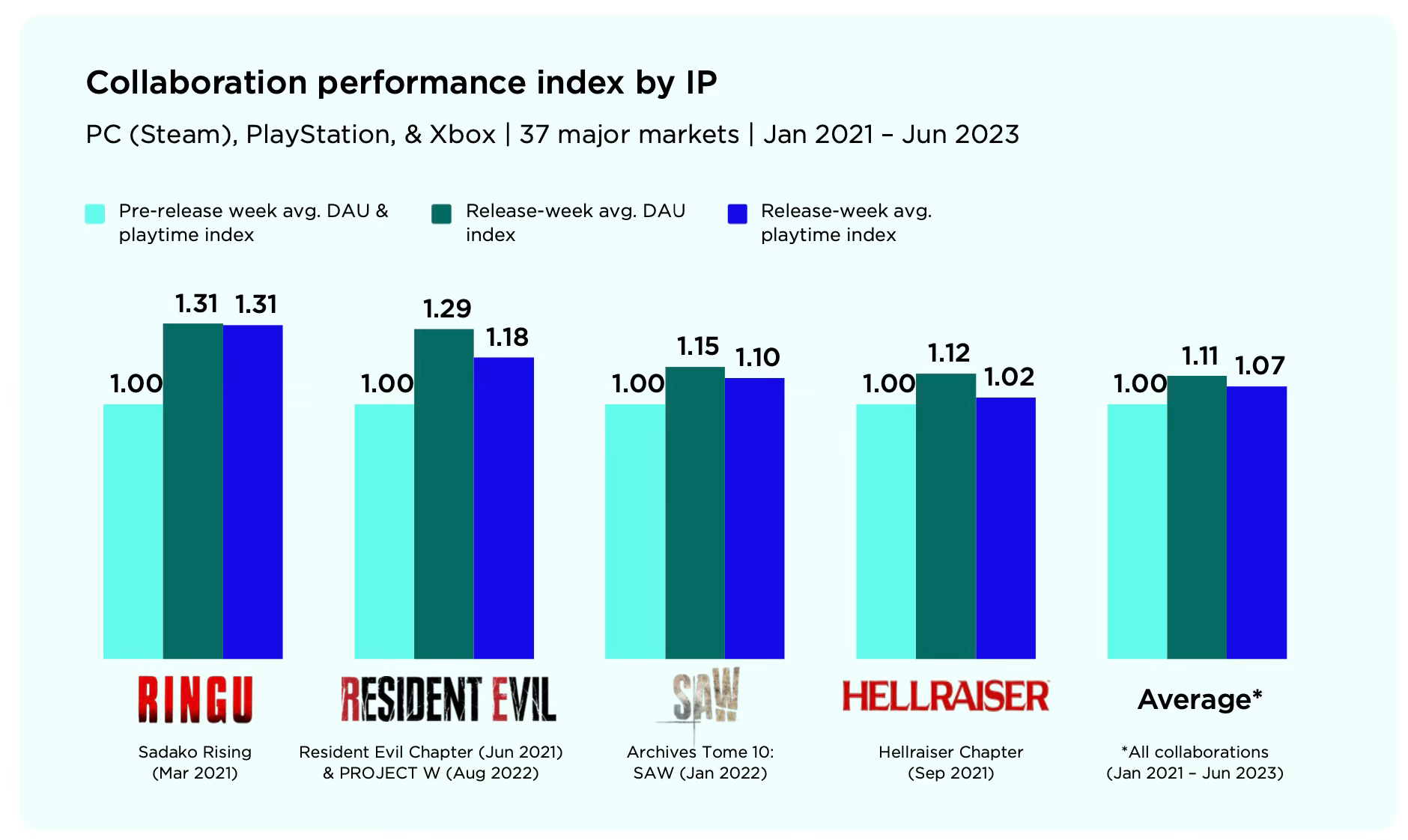

Case Study: Dead by Daylight

The game developer successfully collaborates with various popular horror franchises.

Thanks for reading GameDev Reports! Subscribe for free to receive new posts and support my work.

Subscribed

The most successful collaboration was with the movie "The Ring." DAU and average time in the game increased by 31% in the first week.

In second place was the collaboration with Resident Evil. DAU increased by 29%, and game time increased by 18% in the first week.

The average growth in DAU for all collaborations is 11%, and the growth in time spent is 7%.

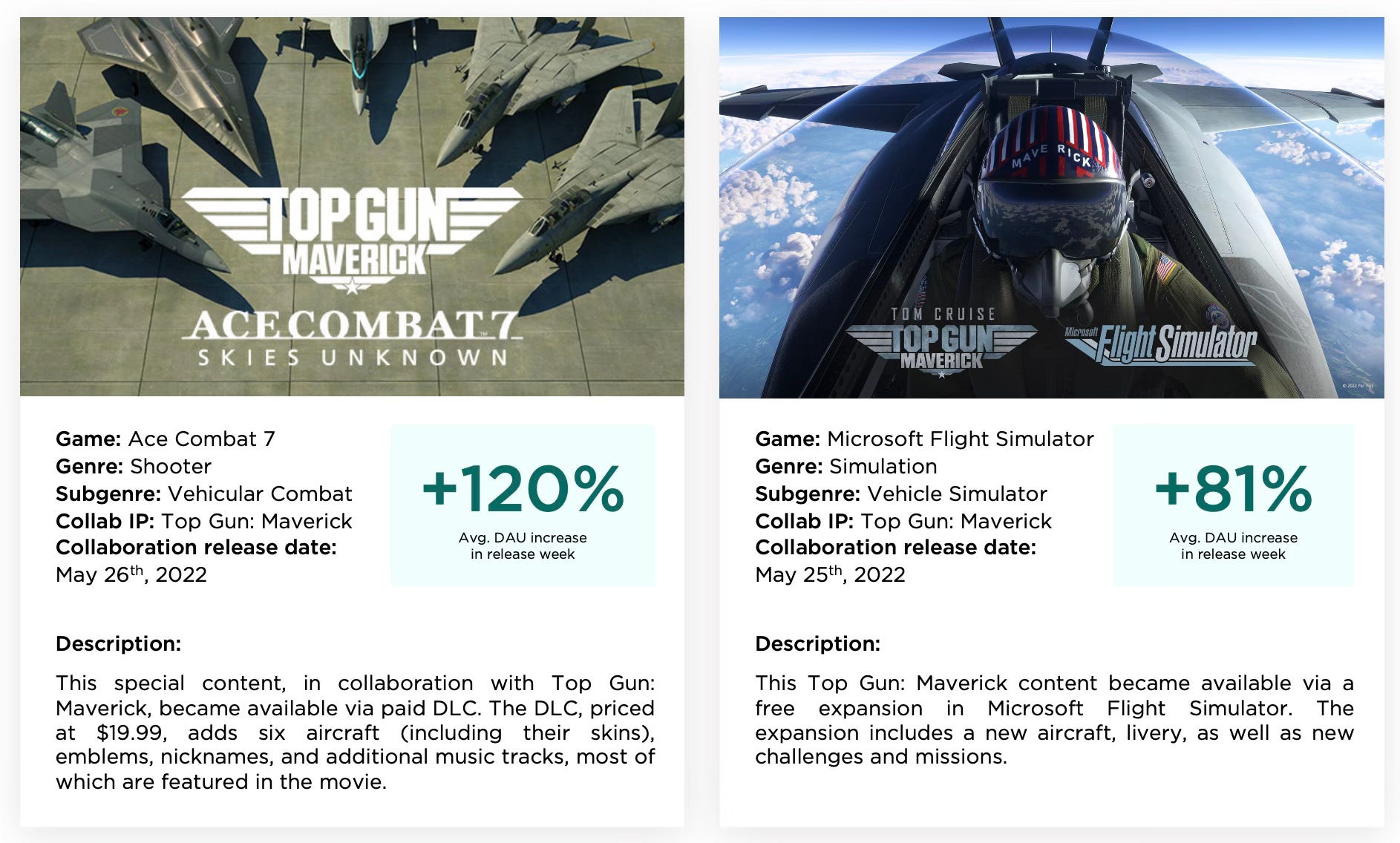

Case Study: Top Gun Maverick

Two collaborations with games were announced for the movie release - with Ace Combat 7: Skies Unknown and Microsoft Flight Simulator.

In the case of Ace Combat 7: Skies Unknown, a paid DLC priced at $19.99 was released. It added 6 new combat vehicles, emblems, music, and other in-game items. DAU of the game increased by 120% in the week after the release.

In the case of Microsoft Flight Simulator, a free add-on was released, including an aircraft, cosmetic items, new trials, and missions. The DAU growth in the week after the release was 81%.

❗️ It is important to note that Newzoo looks at collaborations in terms of audience growth. However, in reality, the goal of collaborations is not only to expand the potential audience but also to maximize the conversion of the existing audience into payments. Key success markers for collaborations should include a combination of engagement and monetization metrics.

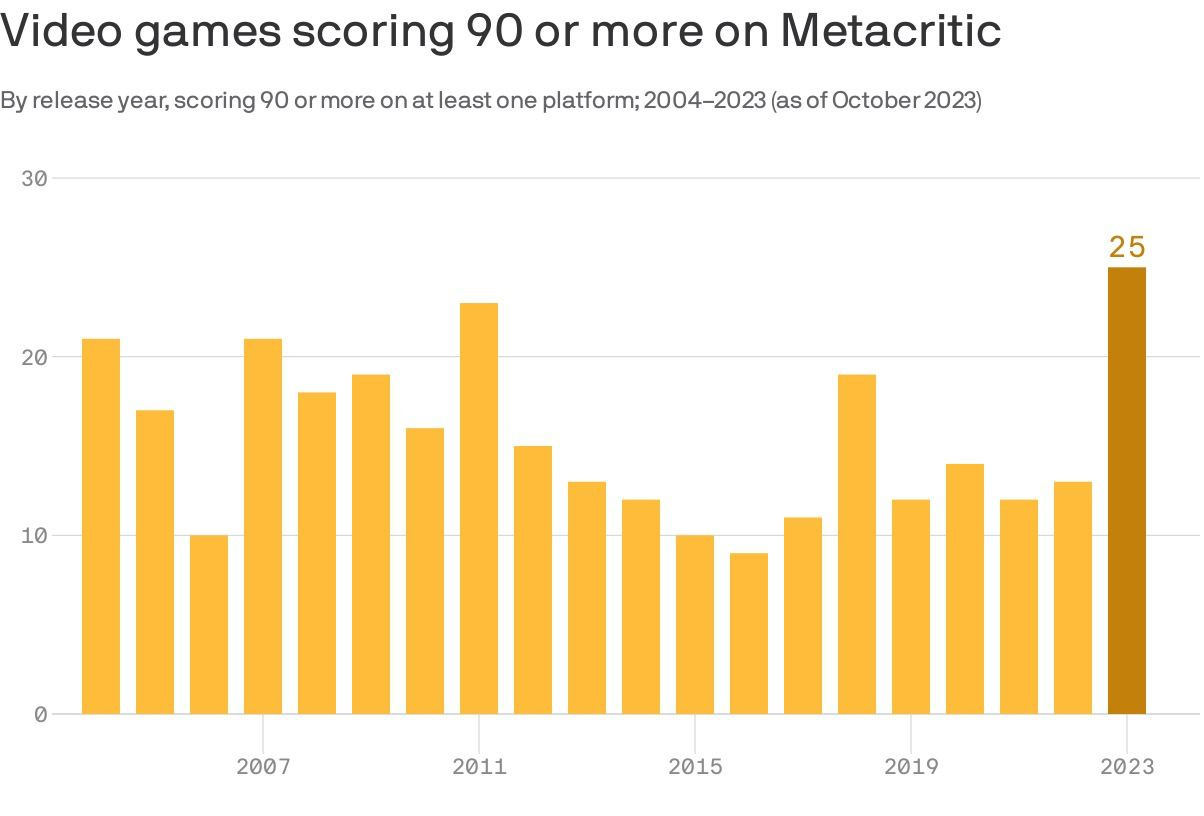

Axios: 2023 is already a record year for games with 90+ ratings on Metacritic

As of the end of October 2023, there have been 25 games with a rating above 90 on Metacritic. The most notable projects include The Legend of Zelda: Tears of the Kingdom, Baldur’s Gate III, and the remake of Resident Evil 4.

The industry has come closest to these results in 2011 when 23 games with a rating above 90 were released.

In 2023, many projects came close to reaching the required rating. These include the remake of Dead Space (89 points), the indie project Pizza Tower (89 points), Armored Core VI: Fires of Rubicon (88 points), and Hi-Fi Rush (87 points).

So, if you've found yourself thinking that 2023 is one of the best years for the gaming industry in terms of games, there is now statistical confirmation for that. Ironically, it's in this year that game studios have actively carried out layoffs.