Weekly Gaming Reports Recap: November 13 - November 17 (2023)

Warcraft Rumble earned $6M in the first week; only $1.1B of the Indian market is currently about non-RMG games; Newzoo provided the 2023 industry outlook.

Reports of this week:

Editorial: Warcraft Rumble earned $6 million in the first week

AppMagic: Top Mobile games of October 2023 by Revenue and Downloads

Lumikai & Google: The Indian Gaming Market in 2023 and Forecast until 2027

Newzoo: The Gaming Industry in 2023

Circana: The American gaming market in October 2023 fell by 5%

Famitsu: Super Mario Bros. Wonder became the leader of the Japanese chart in October 2023

InvestGame: Gaming Market investment activity in Q3 2023

Editorial: Warcraft Rumble earned $6 million in the first week

AppMagic provides net revenue data - after the store commissions and taxes.

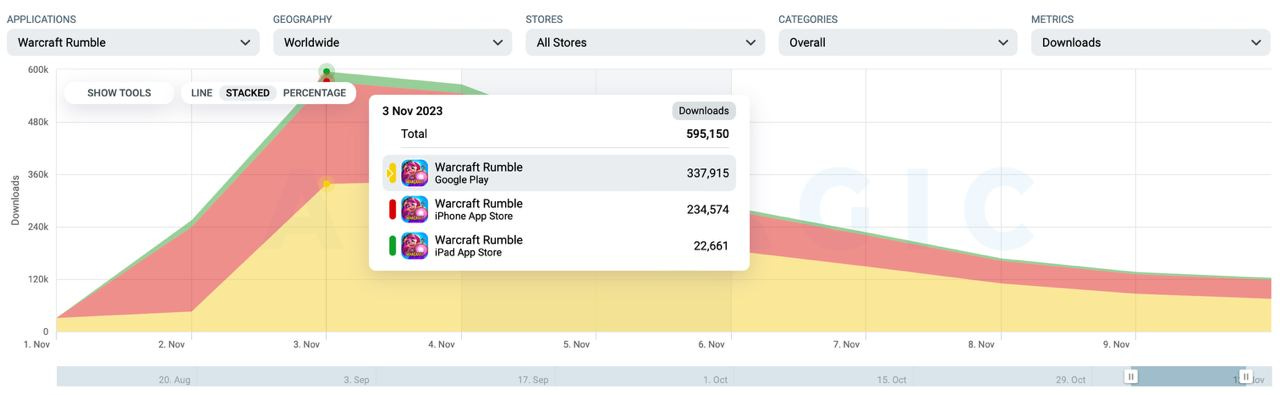

According to AppMagic, the game earned $6 million in the first week after release. Similar data is provided by data.ai - $5.68 million.

Currently, the total revenue of the project is $7.8 million - the game reached $900 thousand per day over the weekend. The game is steadily growing in revenue.

59% of the project's revenue came from iOS; 41% - from Google Play.

The majority of revenue - 44% - comes from the United States. Germany (10%), Taiwan (6%), South Korea (6%), and France (5%) follow.

The game was downloaded 2.8 million times in the first week. The peak was on the release day (November 3) - the game received almost 600 thousand installs.

Downloads are decreasing - currently, the game is downloaded by about 100 thousand users per day.

The cumulative RpD of the project is currently $2.61. But it's still too early to draw conclusions; the game has not had enough time to demonstrate its medium- and long-term mechanics.

Comparison with the launch of Clash Royale

Supercell's game earned $27.1 million in the first week after release (March 2, 2016 - March 9, 2016). This is almost 5 times better than Warcraft Rumble.

The number of downloads was 8 times higher - Clash Royale was downloaded 22.7 million times in the first week.

Currently, Clash Royale's RpD is $4.88. This is twice as high as Warcraft Rumble, but the data is collected for the entire existence of the project. Therefore, Blizzard Entertainment's game still has time to catch up.

💭 It's quite possible that the Clash brand from Supercell is stronger on mobile devices than Warcraft. This can be indirectly inferred from the initial results of the two games.

AppMagic: Top Mobile games of October 2023 by Revenue and Downloads

AppMagic provides revenue data net of store fees and taxes.

Revenue

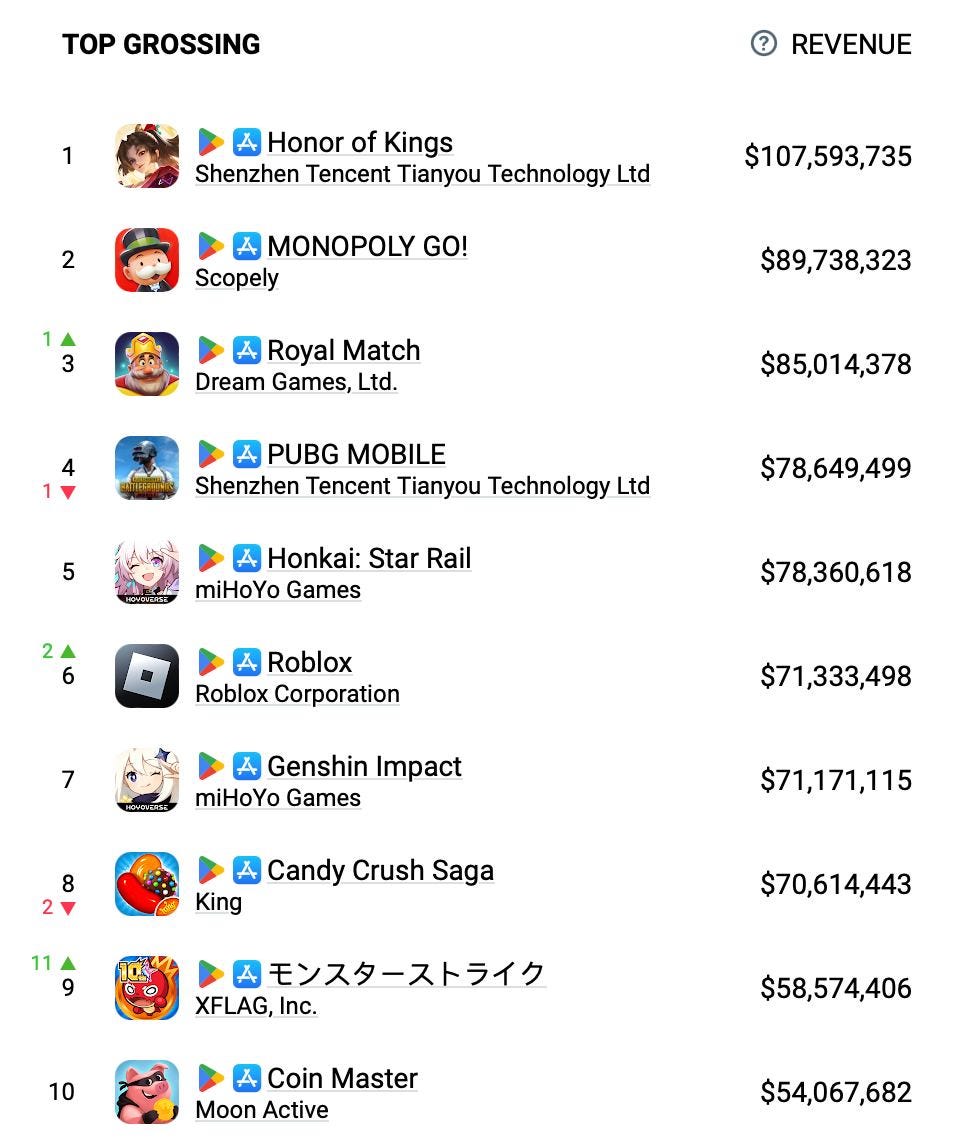

Honor of Kings - the leader. In October, the game earned nearly $108 million, excluding alternative stores.

MONOPOLY GO! holds the second position. In October, the game earned $89.7 million, and the project's monthly revenue continues to grow.

Monster Strike returned to the top 10 in the 9th position. The game earned $58.6 million in October, with 98% of the revenue coming from Japan.

Downloads

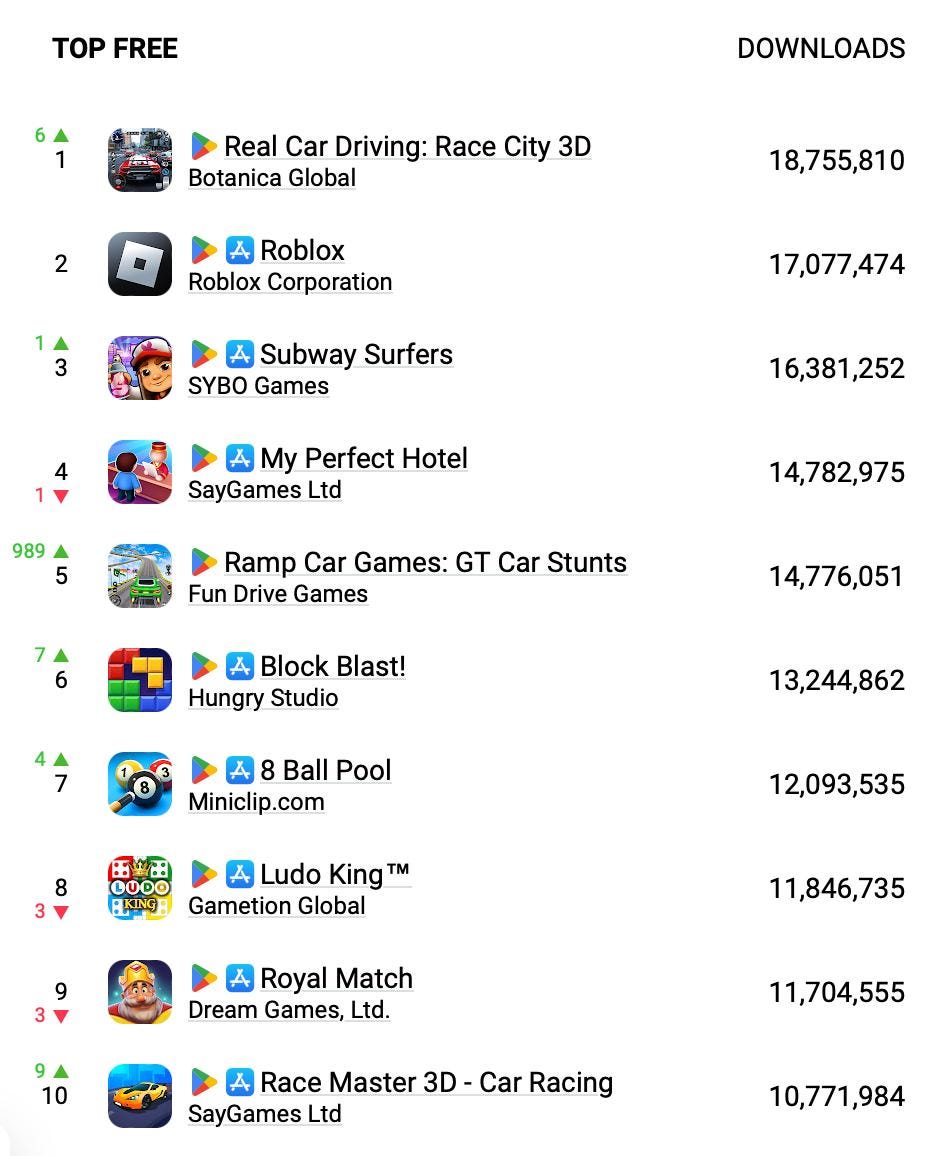

Real Car Driving: Race City 3D became the most downloaded game of the month with 18.8 million installations.

In the second place is Roblox (17 million downloads), and in the third place is Subway Surfers (16.4 million installations).

Among the newcomers on the chart is only Ramp Car Games: GT Car Stunts from Fun Drive Games. The game was downloaded 14.8 million times in October.

Lumikai & Google: The Indian Gaming Market in 2023 and Forecast until 2027

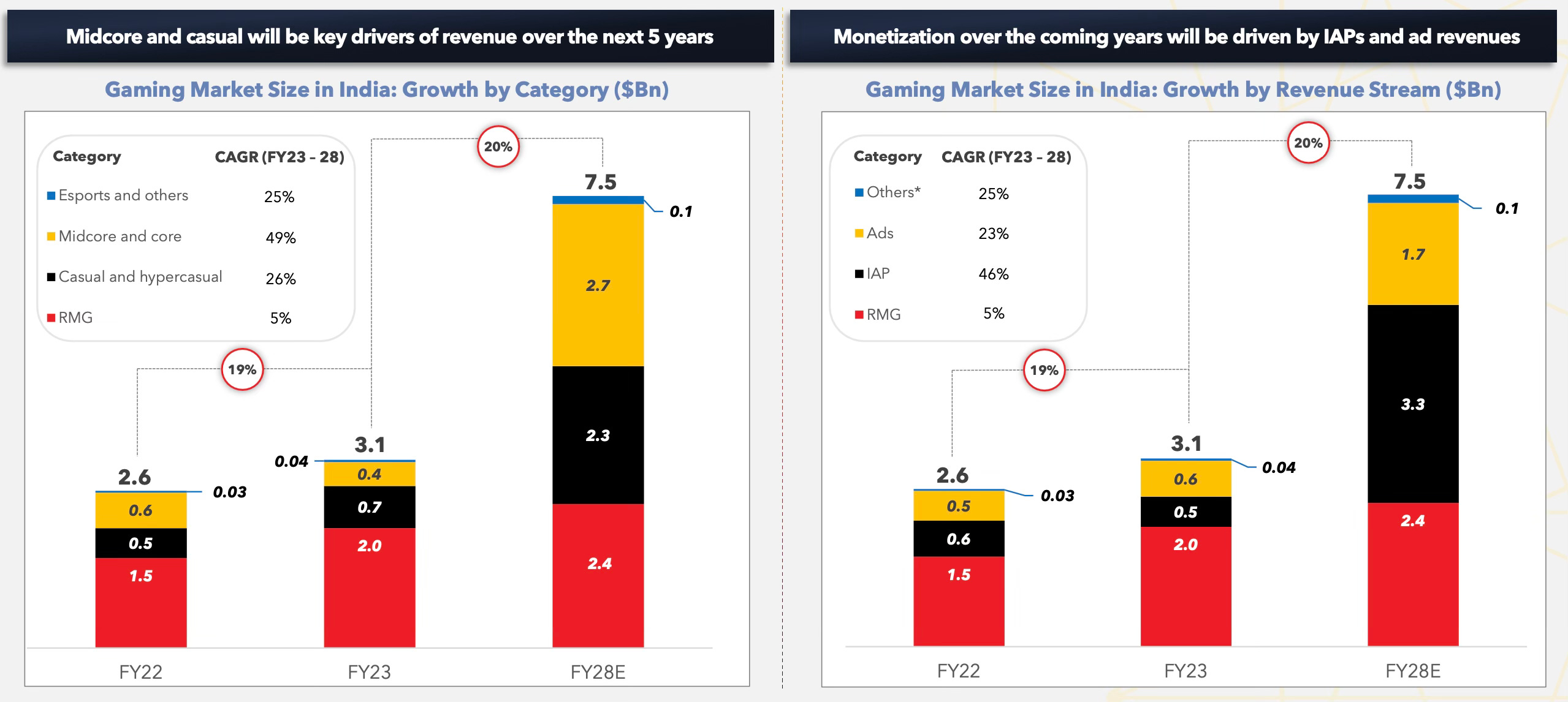

The size of the Indian gaming market in 2023 will reach $3.1 billion. Mobile games account for only $1.1 billion, with the remaining volume taken up by Real Money Gaming (RMG) games.

❗️ In October, India announced a 28% tax on deposits in RMG games, impacting the entire industry.

Therefore, Lumikai and Google forecast a very restrained annual growth of 5% for the entire segment until 2028.

However, mobile games are expected to show explosive growth. The growth of the casual games segment is projected to increase from $0.7 billion in 2023 to $2.3 billion in 2028 (26% average annual growth rate). In the case of mid-core and hardcore projects, growth is expected from $0.4 billion to $2.7 billion in 2028 (49% average annual growth rate).

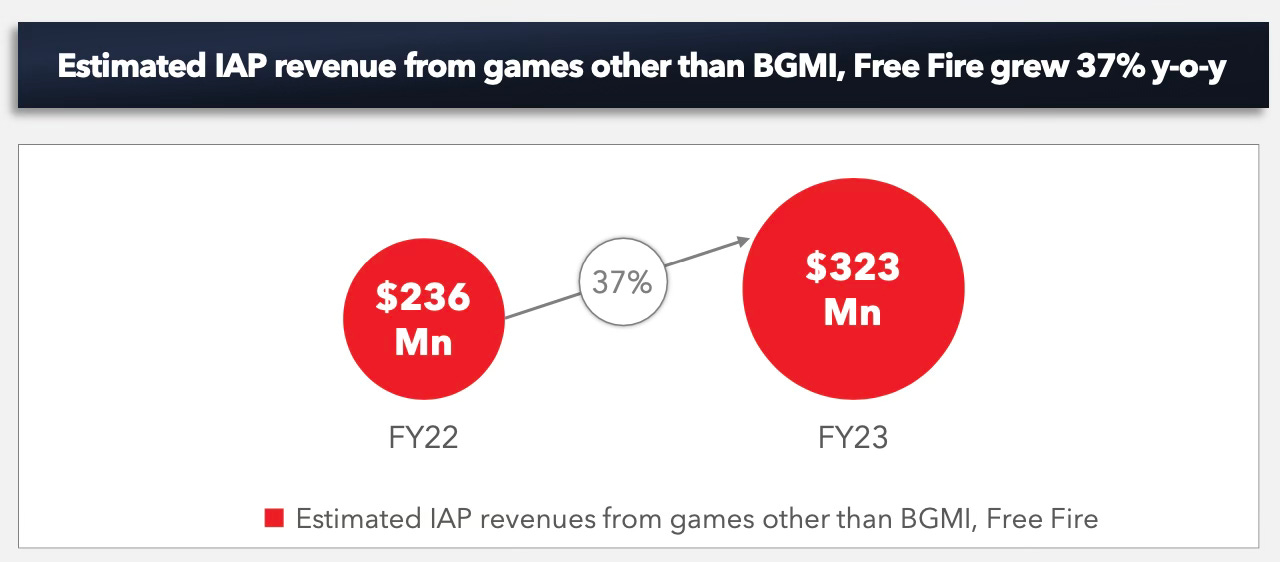

Interestingly, the growth of in-game payments beyond Battlegrounds Mobile India and Garena: Free Fire was separately calculated. In 2023, players spent $323 million on in-game purchases in other games, with a 37% growth compared to 2022.

❗️ If the data in the report is consistent, the two largest Battle Royale games in India account for approximately $180 million in revenue annually.

Lumikai and Google believe that the volume of in-game transactions in India will grow nearly sevenfold in five years, and advertising revenue will triple.

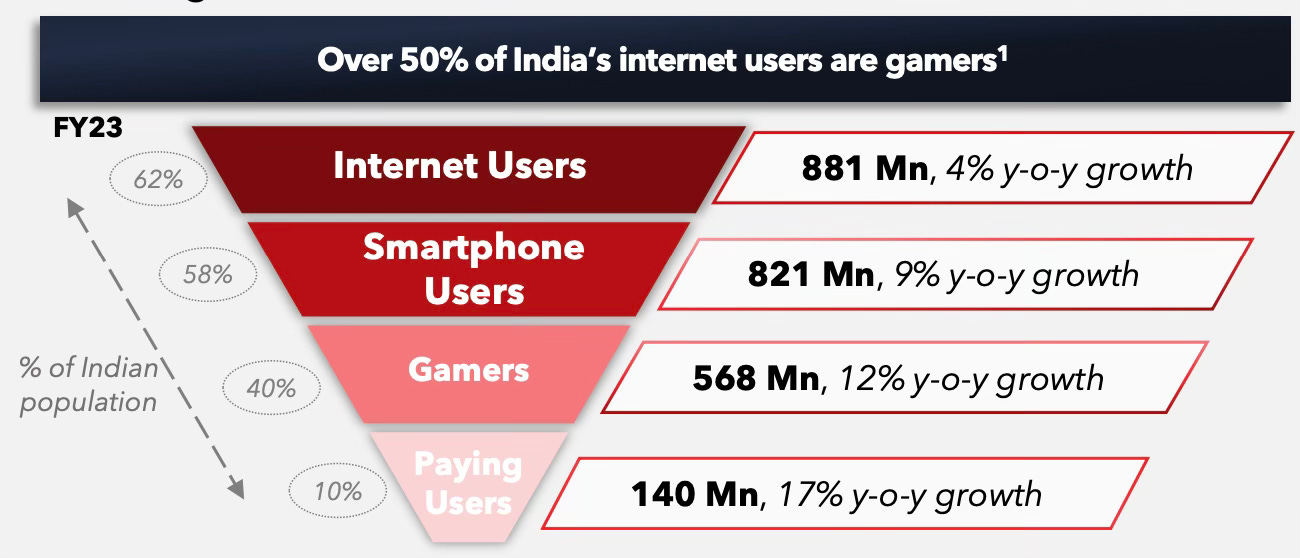

Currently, India has 568 million players, of which only 140 million are paying players. On average, they spend 10-12 hours per week on games.

59% of players are male, and 41% are female.

The majority of players (50%) are young people aged 18 to 30.

The number of players in India from non-major (by Indian standards) cities is growing. In 2023, they account for 66% of the entire audience.

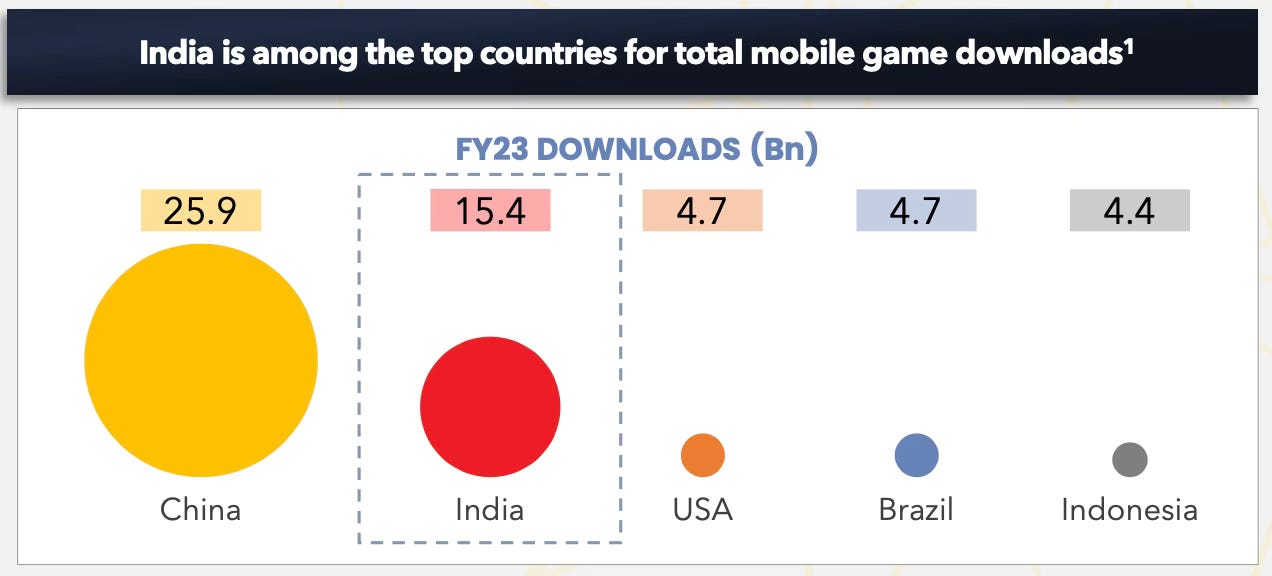

India is the second-largest market after China in terms of game downloads (15.4 billion per year).

Lumikai and Google note that in 2023, the average annual ARPPU (Average Revenue Per Paying User) for a user from India is $19.2. In 2019, this indicator was $2.

Newzoo: The Gaming Industry in 2023

The user research is based on a survey of more than 74,000 people from 36 countries around the world aged 10 to 65. Revenue data does not include taxes, advertising, and "hardware" sales.

Revenue

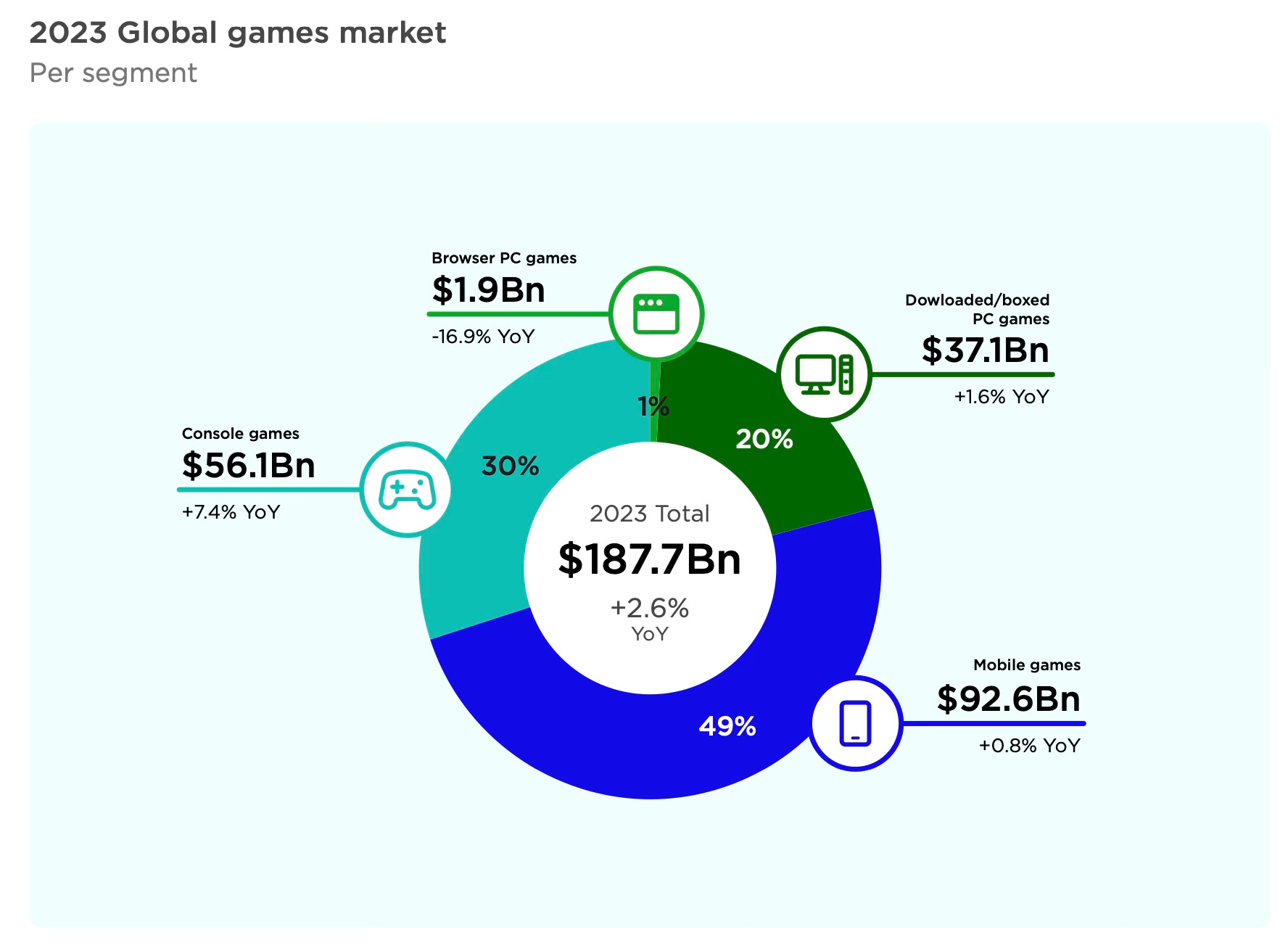

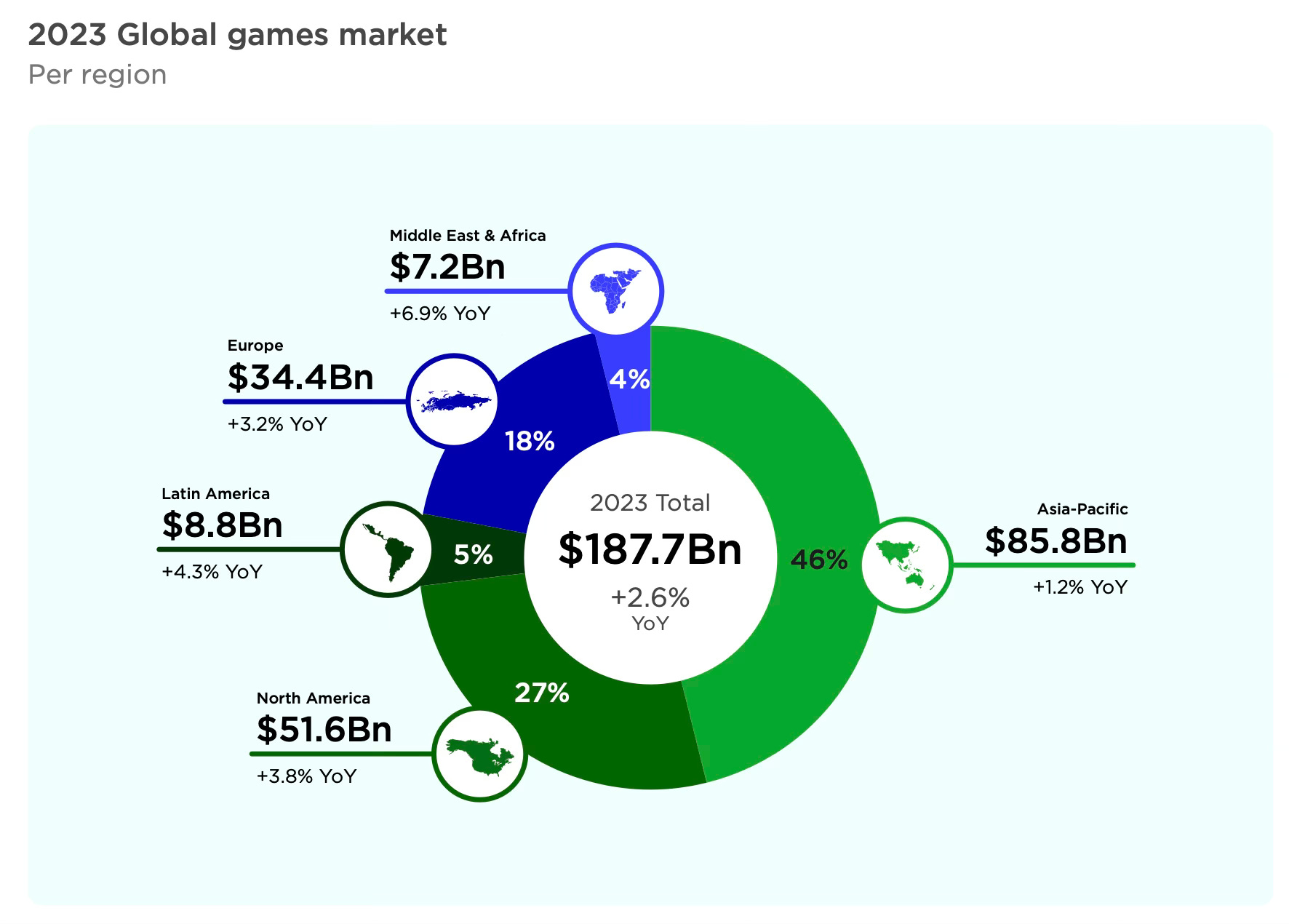

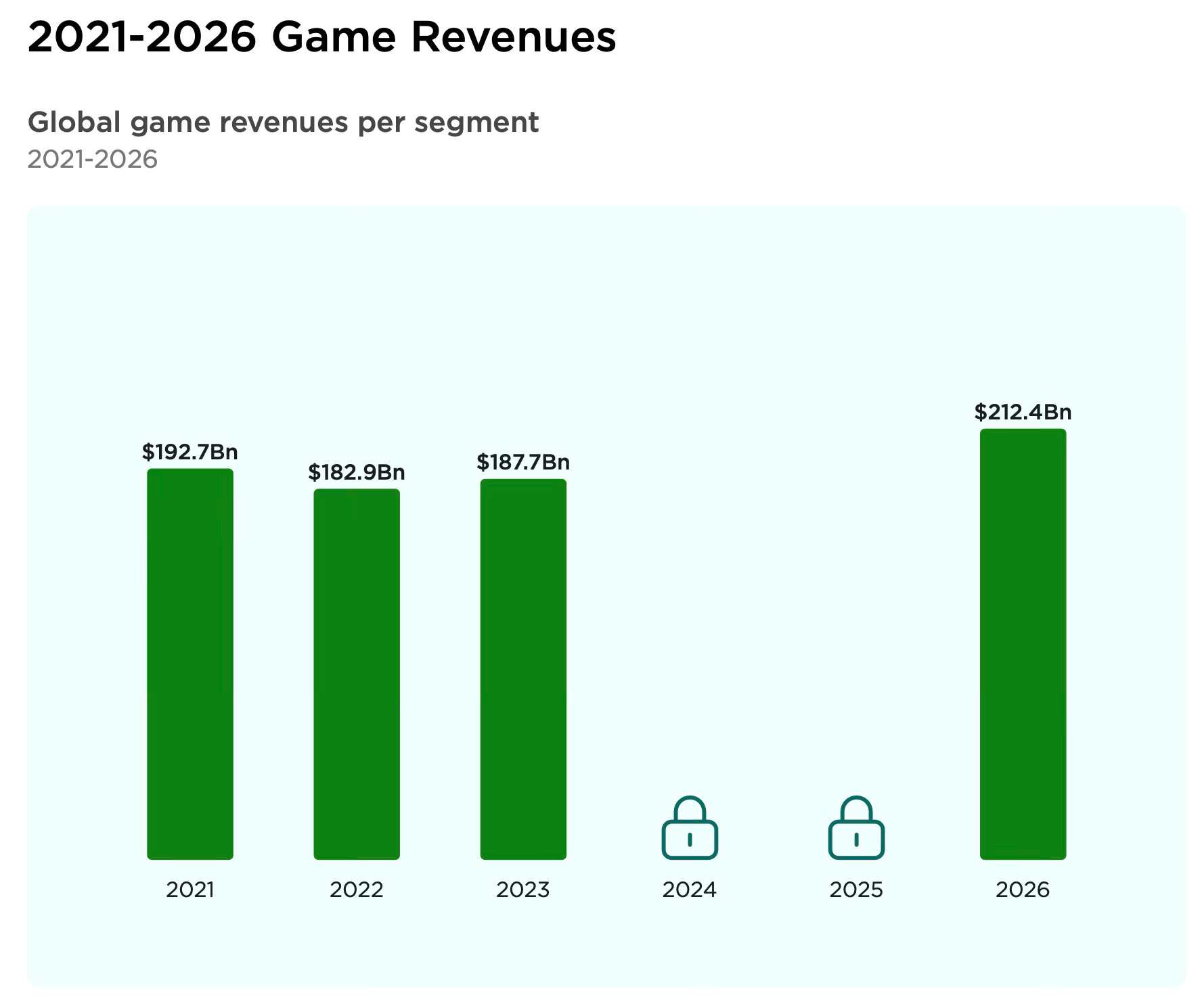

By the end of 2023, the gaming market will grow by 2.6% and reach $187.7 billion.

$92.6 billion (49%) - revenue of the mobile market. Newzoo believes that the growth of this segment will be limited due to platform policies regarding user data. By the end of 2023, it will grow by 0.8%.

The console market grew the most, by 7.4%, reaching $56.1 billion. Newzoo analysts note that this segment in 2022 underperformed in revenue due to delays in major releases and a shortage of consoles.

PC segment revenue by the end of 2023 will reach $37.1 billion. This is 1.6% more than the previous year. Browser PC games continue to decline rapidly, by 16.9% per year. The volume of this segment in 2023 will be $1.9 billion.

46% of gaming revenue ($85.5 billion) is concentrated in the Asia-Pacific region. 27% ($51.6 billion) in North America. 18% ($34.4 billion) in Europe. 5% ($8.8 billion) in Latin America. 4% ($7.2 billion) in the Middle East and Africa. This region is growing the fastest - by 6.9% per year.

Newzoo believes that the gaming market has stabilized after the pandemic growth and subsequent correction. By the end of 2026, the market volume will reach $212.4 billion.

Users

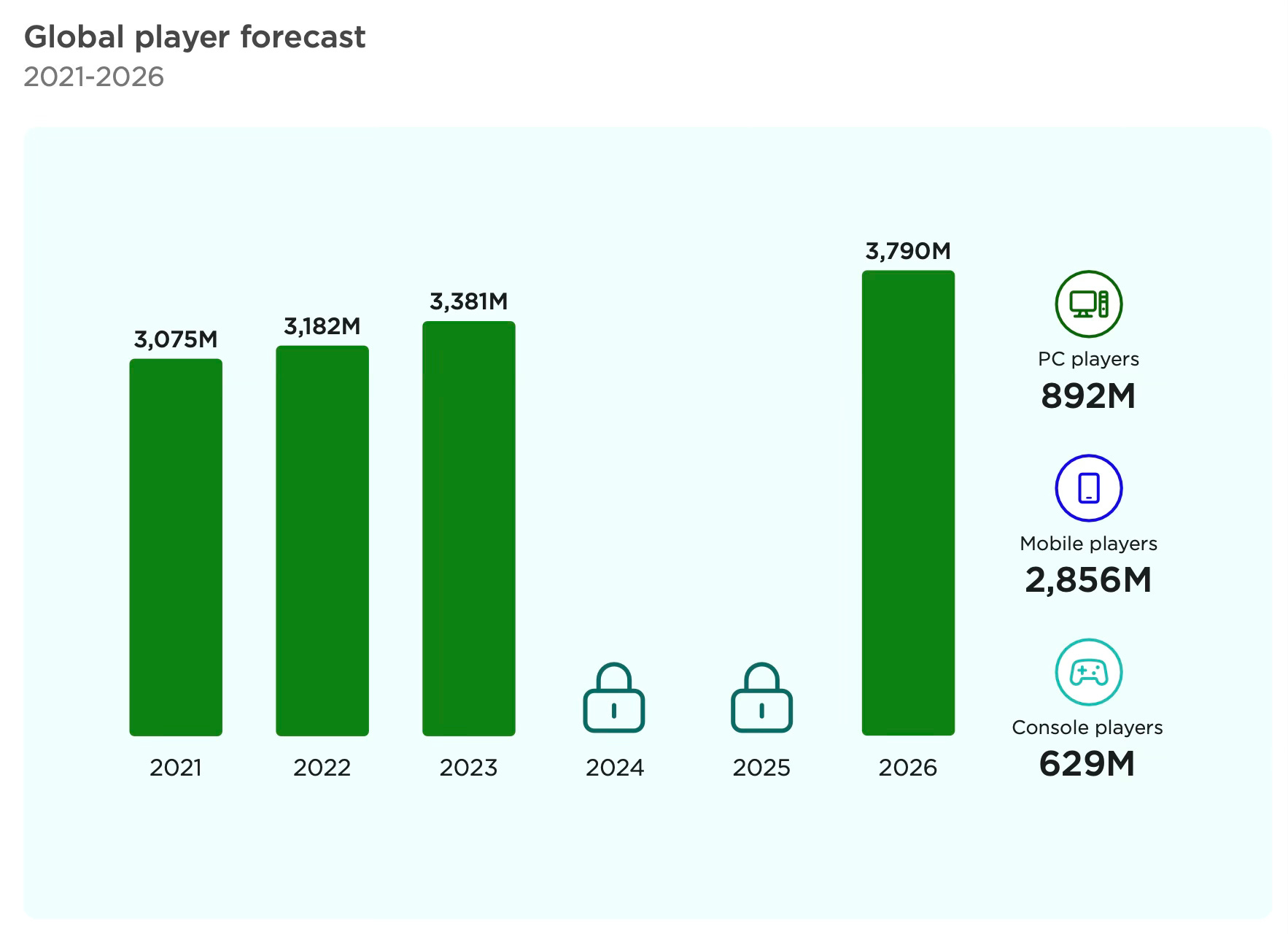

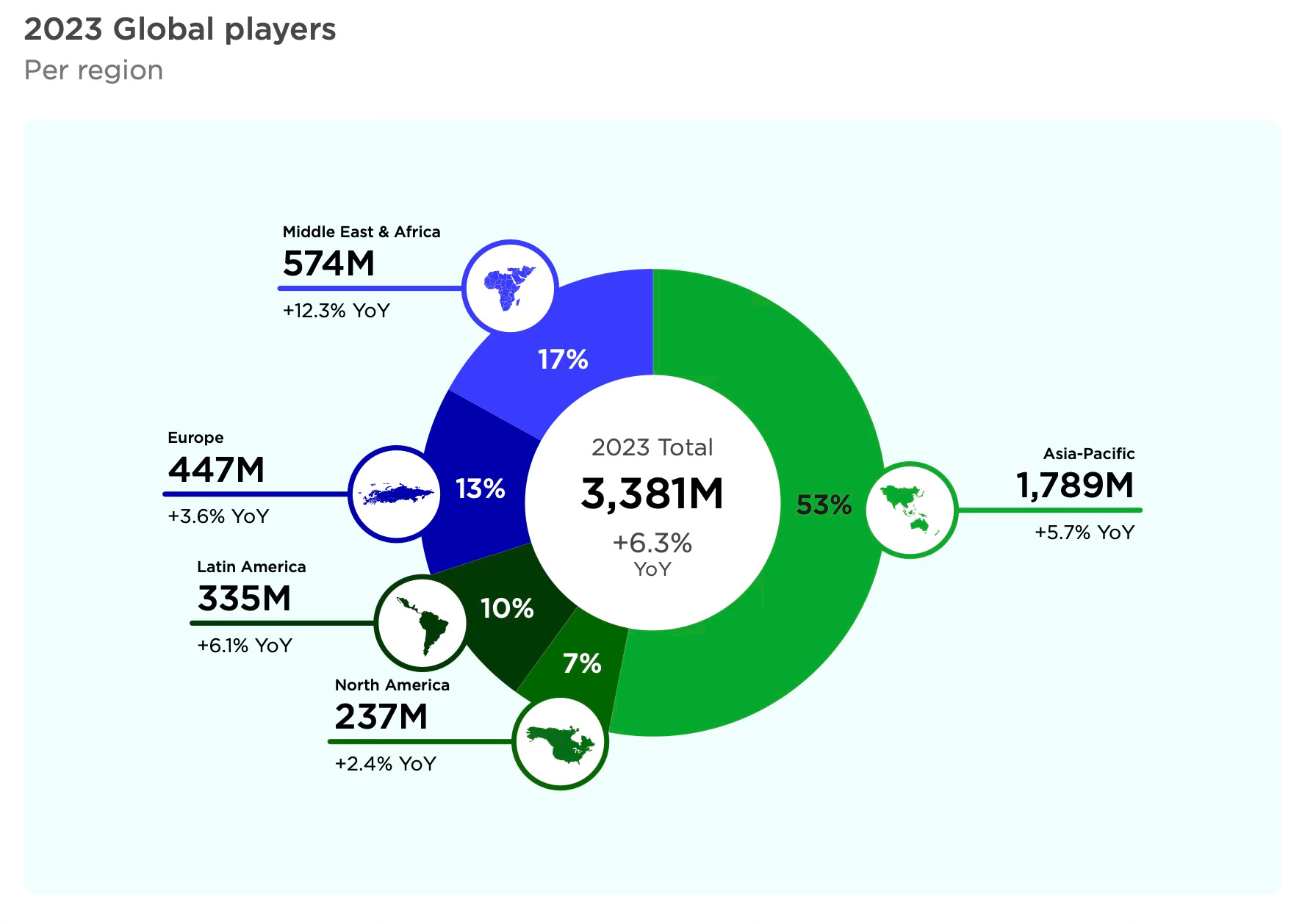

The number of gamers worldwide will reach 3.38 billion. This is 6.3% more than the previous year.

2.856 billion gamers play on mobile devices; 892 million on PC; 629 million on consoles.

53% of the entire gaming audience is concentrated in the Asia-Pacific region. 17% in the Middle East and Africa (also the fastest-growing region in terms of users - +12.3% per year). 13% in Europe; 10% in Latin America; 7% in North America.

The number of paying gamers by the end of 2023 will grow by 7.3% to 1.47 billion. The average annual growth rate from 2021 to 2026 is expected to be 4.7%, and by the end of 2026, there will be 1.66 billion paying gamers.

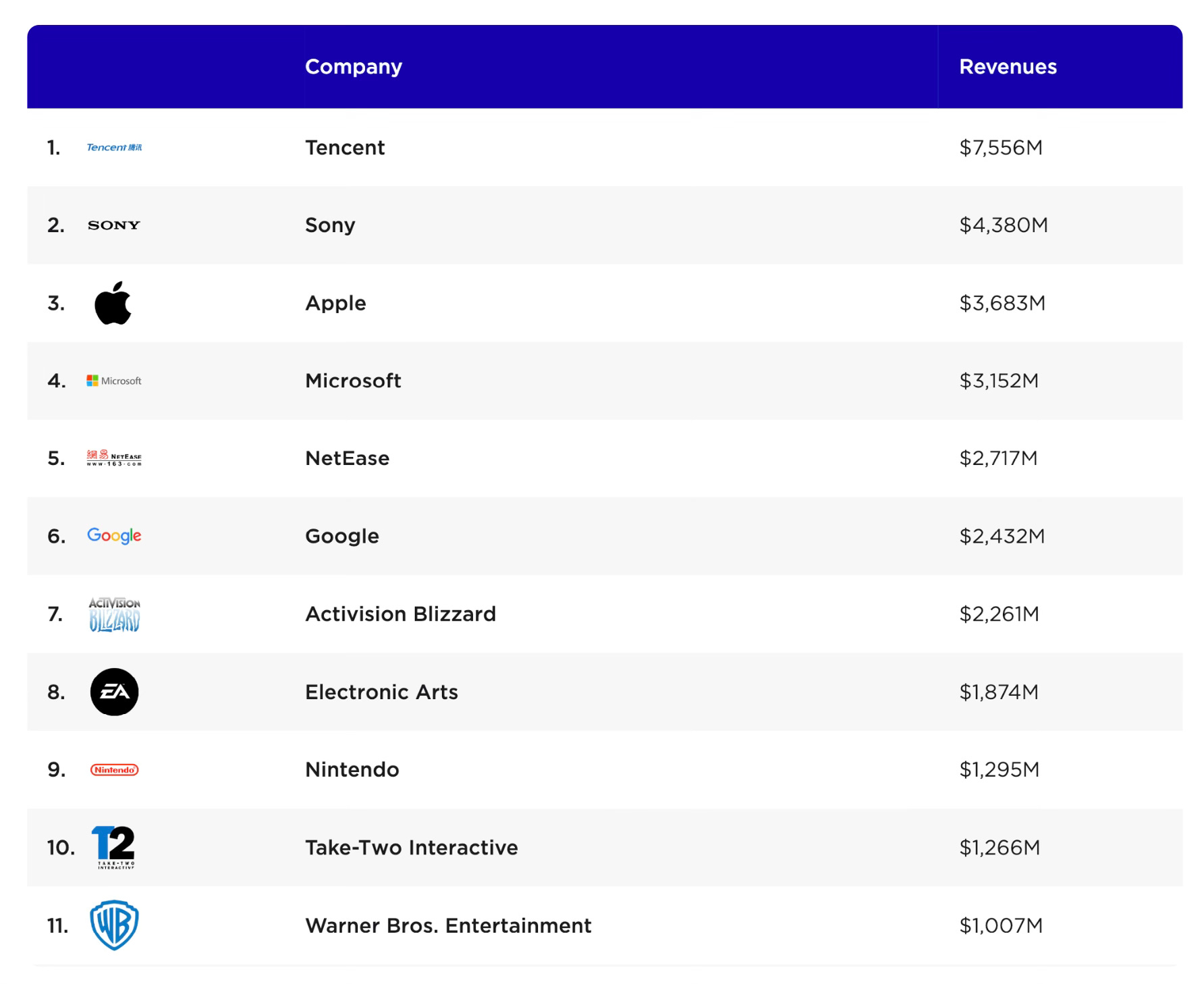

Companies

Tencent - the largest public company by gaming revenue. In 2023, it will earn $7.556 billion.

The combined revenue of Microsoft and Activision Blizzard will be $5.413 billion. This makes Microsoft the second company in the world by gaming revenue. Sony will have $4.38 billion in 2023.

Cloud Gaming

In 2023, the number of paying users will be around 43.1 million. By 2025, this number is expected to almost double - to 80.4 million.

Trends

The boom in live-service games continues. But it's very difficult for new players to get started.

AI is changing approaches to development in the gaming industry.

Complementary gaming devices are becoming increasingly popular. Newzoo includes Steam Deck and Nintendo Switch in this category.

Mobile game studios continue to adapt to changing platform regulations.

User-generated content (UGC), the creative economy, and opinion leaders become a crucial part of the success of games and studios.

Apple enters VR; Meta still believes in the direction. There is growth.

Development of the gaming market in Saudi Arabia (thanks to Savvy Games Group). Strengthening positions of developers from China and Japan.

Circana: The American gaming market in October 2023 fell by 5%

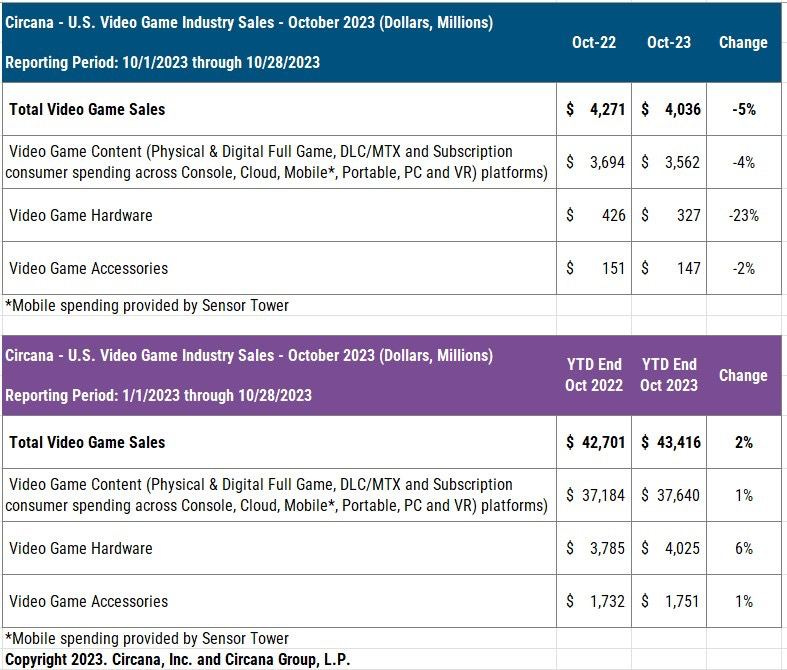

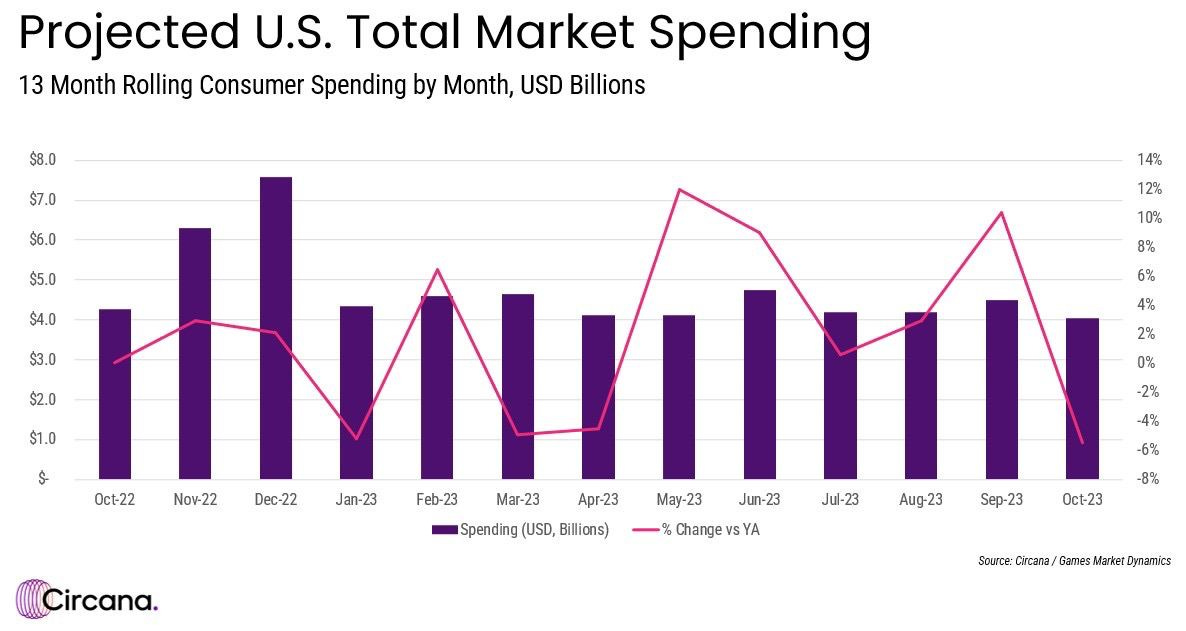

In October, the total revenue of the gaming market amounted to $4.036 billion. This is 5% less than the previous year.

Sales of gaming hardware dropped the most, by 23%, to $327 million.

PlayStation 5 remains the best-selling system both in terms of units sold and in dollar terms.

Content sales decreased by 4% to $3.562 billion. However, this is partially due to the fact that the release of Call of Duty last year took place at the end of September, and a large share of sales fell in October. This year, the new installment started on November 8.

Build games faster using Mudstack - The ultimate Digital Asset Management tool for game studios

Stop wasting money and make artist collaboration easier than ever with

Cloud storage

Integrated review & feedback

Version control

Try for free here -mudstack.com

Accessory sales fell by 2% to $147 million.

As of the end of October, the volume of the American market is $43.4 billion. This is 2% more than the same period last year.

Marvel’s Spider-Man 2, Super Mario Bros. Wonder, and Assassin’s Creed: Mirage became the best-selling games in October on PC and consoles.

Hogwarts Legacy remains the most successful game of the year. Marvel’s Spider-Man 2 rose to the 4th position in American sales in 2023.

Spending on mobile games in the USA in October grew by 2.1%. MONOPOLY GO!, Royal Match, and Roblox are the top 3 games by revenue.

Most popular games on platforms

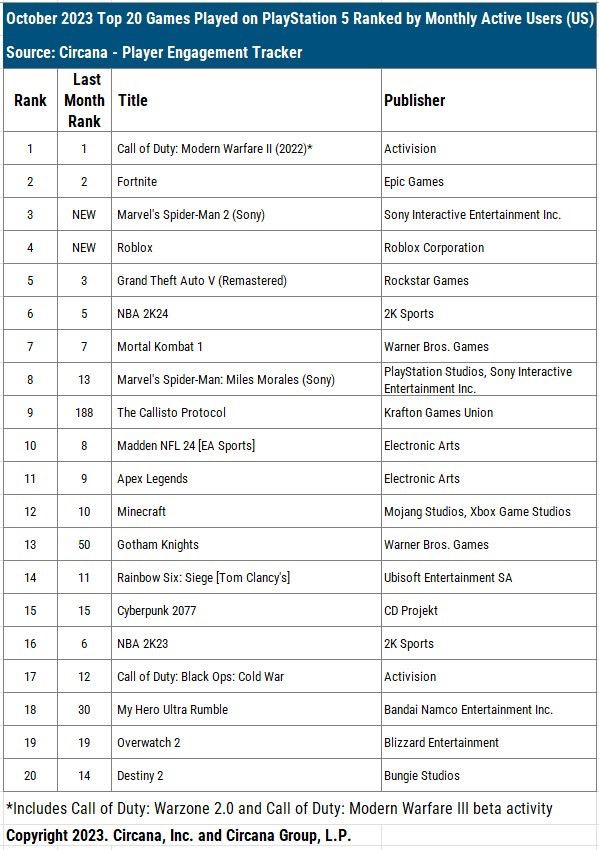

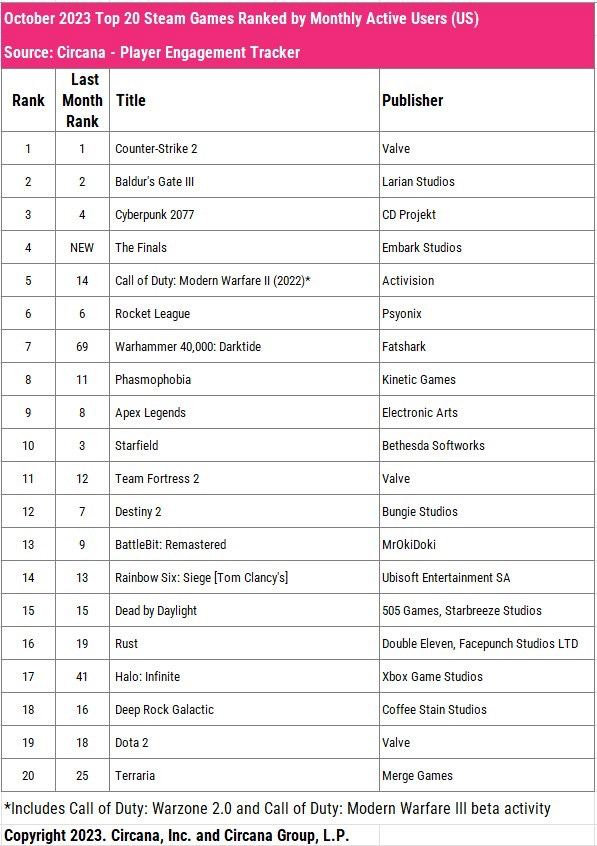

Call of Duty: Modern Warfare II (Call of Duty: Warzone 2.0); Fortnite and Marvel’s Spider-Man 2 - leaders in MAU on PlayStation platforms in October. Roblox immediately started from the 4th position.

Call of Duty: Modern Warfare II (Call of Duty: Warzone 2.0); Fortnite and GTA V - the largest games by MAU on Xbox.

Counter-Strike 2; Baldur’s Gate III, and Cyberpunk 2077 - leaders in MAU on Steam. The Finals beta was in 4th place.

Famitsu: Super Mario Bros. Wonder became the leader of the Japanese chart in October 2023

Famitsu only collects data on physical sales.

Games

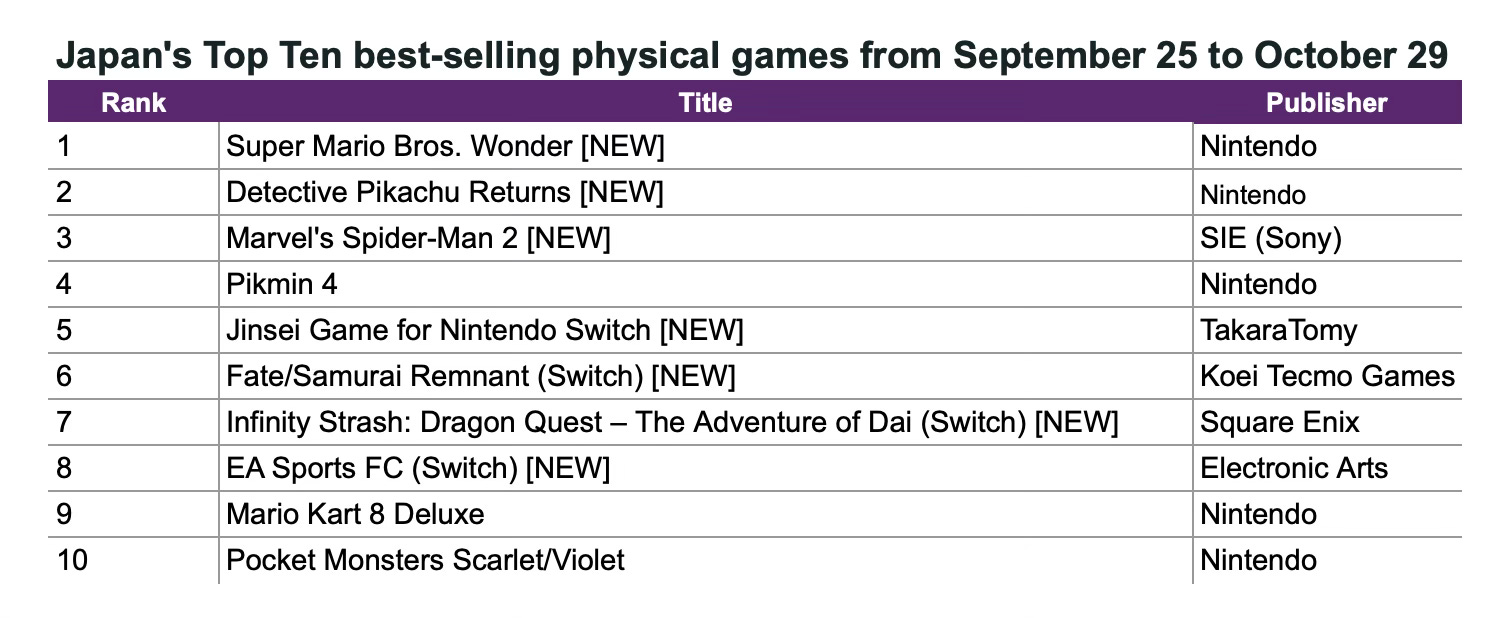

Super Mario Bros. Wonder, released on October 20, sold 801 thousand copies in just 11 days in Japan. This excludes digital sales.

In second place is Detective Pikachu Returns with 110 thousand copies.

Build games faster using Mudstack - The ultimate Digital Asset Management tool for game studios

Stop wasting money and make artist collaboration easier than ever with

Cloud storage

Integrated review & feedback

Version control

Try for free here -mudstack.com

A PlayStation 5 game entered the top 3 of the chart for the first time in a long time. Marvel’s Spider-Man 2 had an excellent start in Japan, with over 90 thousand copies sold monthly.

Physical game sales in Japan in October increased by 25% compared to the previous year, reaching $91 million. Last month, there were 7 new entries in the top 10.

Consoles

Nintendo Switch (with the most popular version being Switch OLED) accounted for 60% of all console sales in October.

PlayStation 5 had a 22% market share in October.

Hardware sales in Japan in October increased by 15% compared to the previous year, reaching $115 million. However, this is the lowest figure in the last six months.

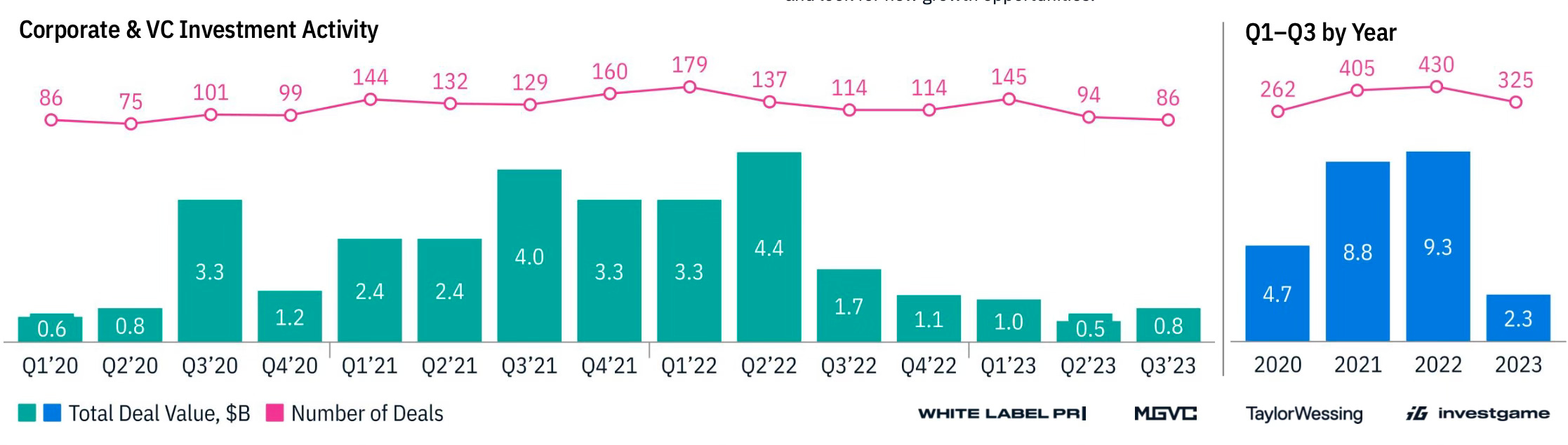

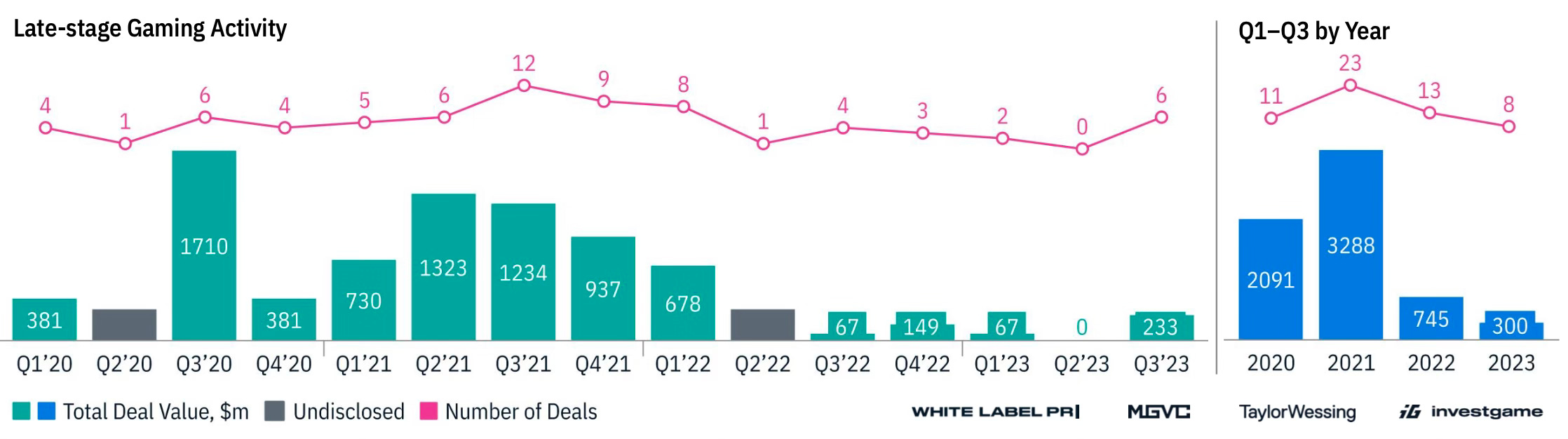

InvestGame: Gaming Market investment activity in Q3 2023

This year, at the current moment, has the lowest business activity in the last 3 years.

Private Investments

By the end of the first three quarters of 2023, the volume of private capital raised amounted to $2.3 billion. This is 4 times less than the average in 2021-2022.

The number of deals also decreased by 23%.

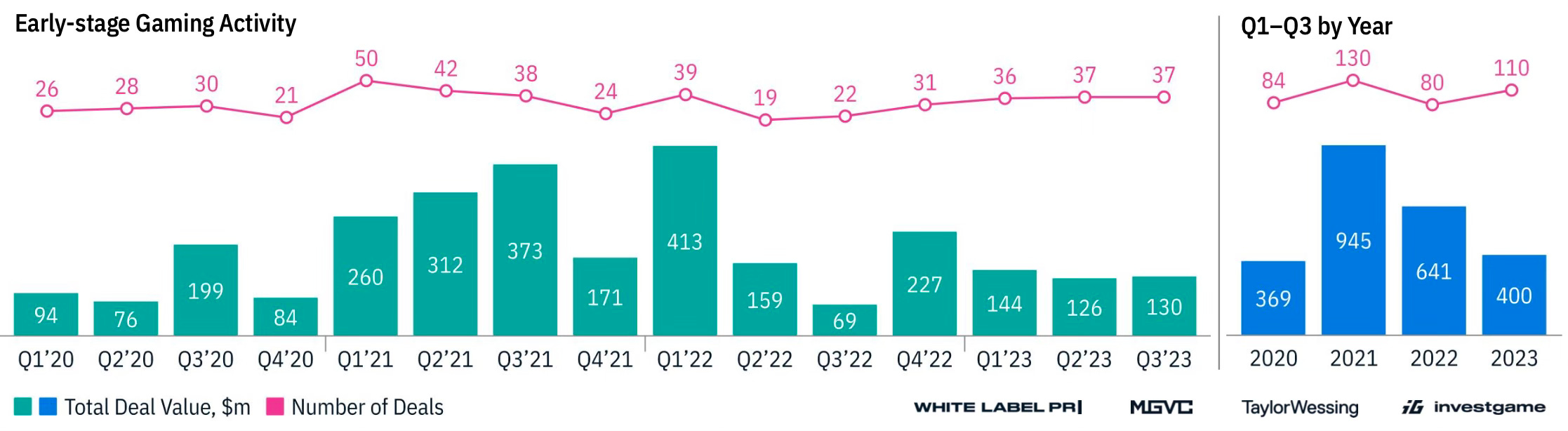

Early-stage deals were less affected by the crisis. In the first 3 quarters of this year, there were 110 deals (compared to 80 in 2022) - totaling $400 million (compared to $6.41 billion in 2022).

It became more challenging at later stages, with fewer follow-up rounds due to unclear exit prospects. In the first 3 quarters, there were 8 deals (compared to 13 in 2022) totaling $300 million (compared to $745 million in 2022).

Despite the negative picture, business activity has returned to pre-COVID levels. There is hope for future growth.

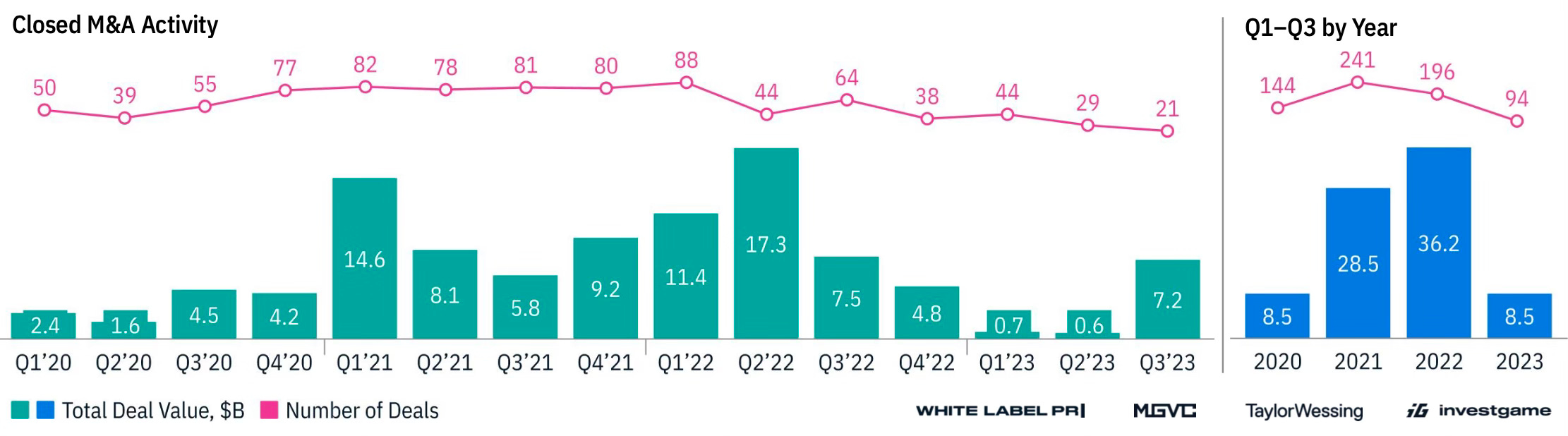

M&A

In the first three quarters of 2023, the total volume of M&A deals amounted to $8.5 billion. This is 3.8 times less than the average in 2021-2022.

Three deals contributed more than 75% of the total volume - the acquisition of Scopely ($4.9 billion), Rovio ($0.8 billion), and Techland (amount undisclosed).

Build games faster using Mudstack - The ultimate Digital Asset Management tool for game studios

Stop wasting money and make artist collaboration easier than ever with

Cloud storage

Integrated review & feedback

Version control

Try for free here -mudstack.com

The deal between Microsoft and Activision Blizzard for $68.7 billion, which closed in October (4th quarter), is not included in the statistics.

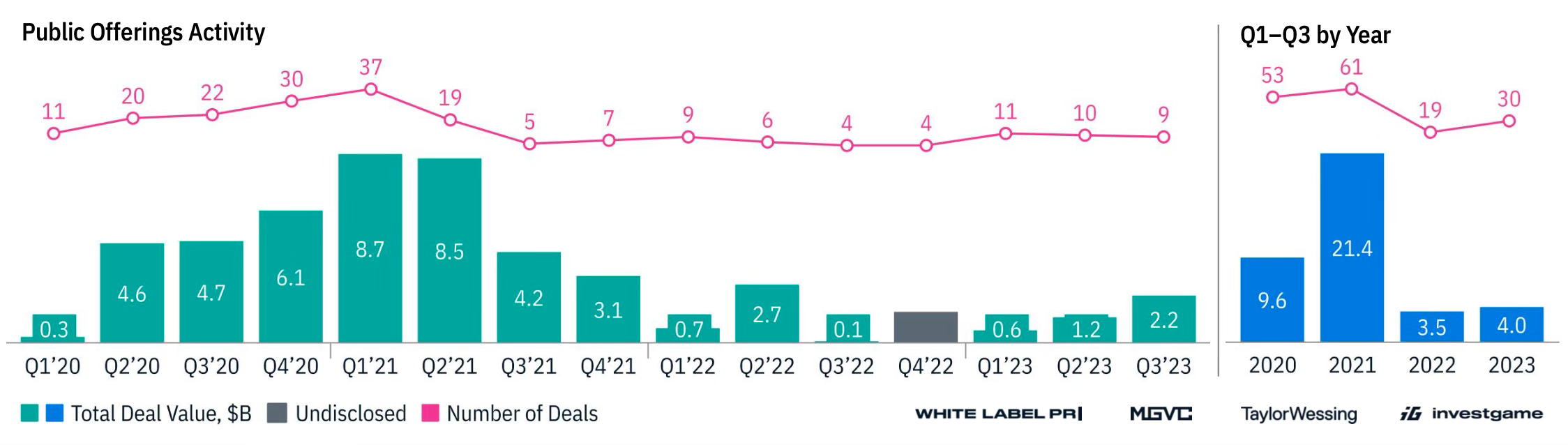

Public Offerings

Excluding the $1.5 billion debt refinancing of AppLovin, the volume of public offerings in the first three quarters of 2023 fell by 29%.

High-interest rates, the poor performance of companies that went public, low valuations, and the crisis make public offerings unpopular options for companies.

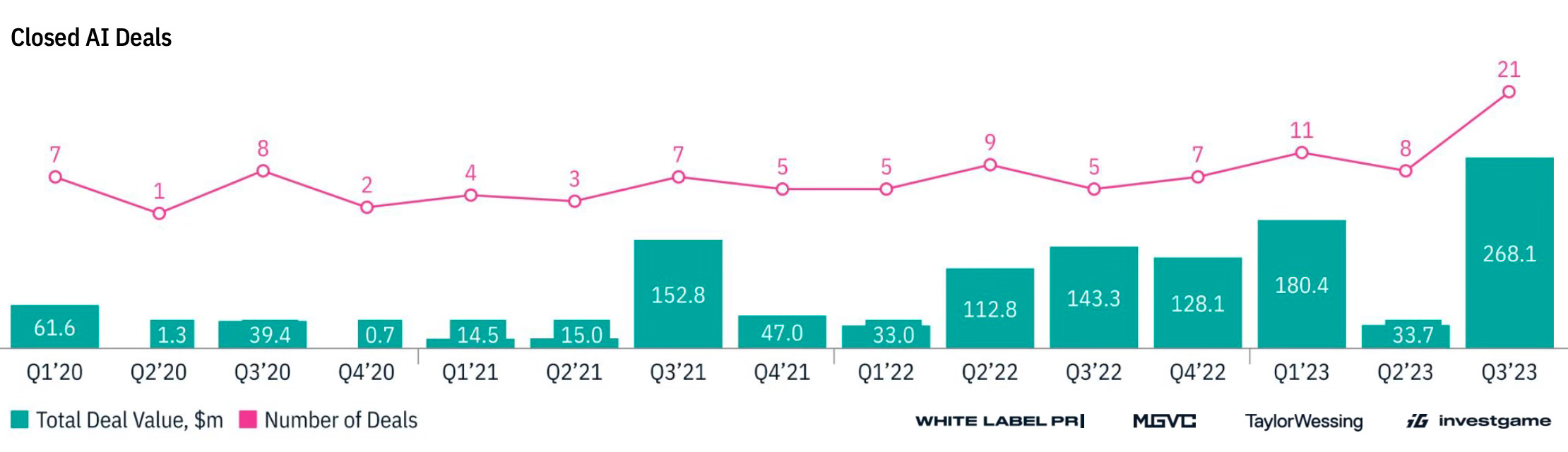

Investments in AI

In the third quarter of 2023, there was a significant increase in investments in AI startups. 21 deals were made totaling $268.1 million - more than the first half of this year.

Subscribe to the InvestGame newsletter to receive digests and detailed deal reviews.