Weekly Gaming Reports Recap: November 20 - November 24 (2023)

51.9% of the British gaming workforce works for foreign companies; Monopoly GO! passed $1B in revenue; 83% of launched games are dying within 3 years.

Editorials:

Monopoly GO: $1 Billion Later

Reports of this week:

GfK & GSD: The UK gaming market in October 2023 experienced a significant decline

Roblox: Trends in Digital Fashion and Beauty in 2023

GSD: Game sales in Europe slightly decreased in October 2023

SuperScale: 83% of launched mobile games die within 3 years

BFI UK: 51.9% of all British game developers work in companies owned by foreign entities

StreamElements & Rainmaker.gg: The State of the Streaming Market in September and October 2023

Monopoly GO: $1 Billion Later

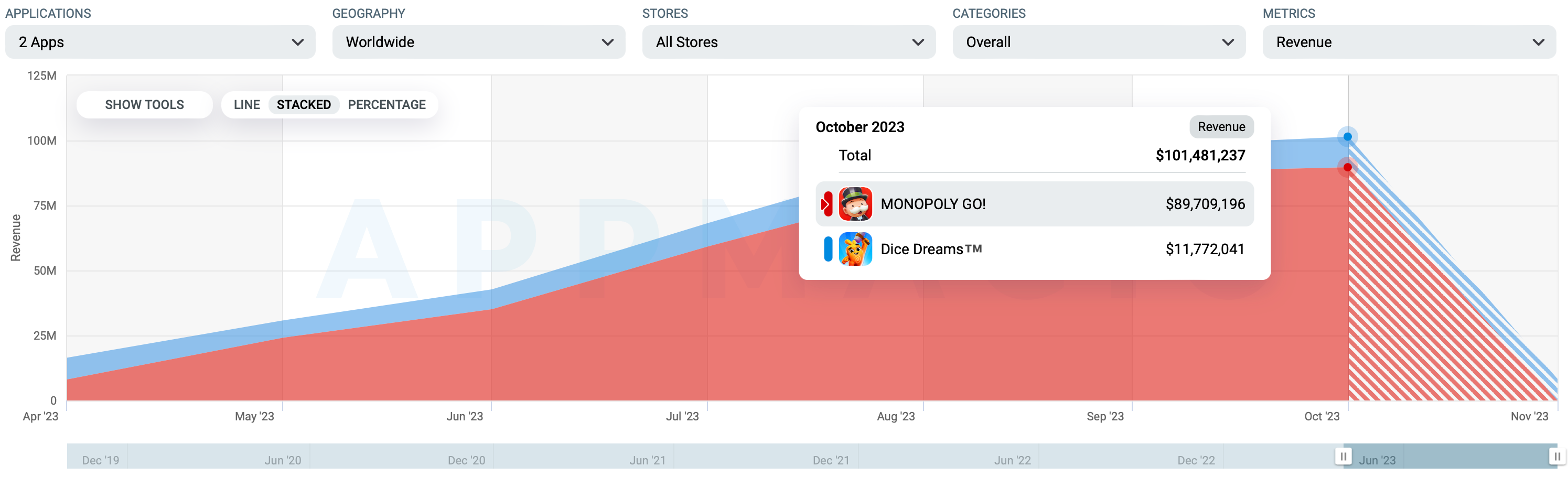

Scopely has announced that MONOPOLY GO! has generated over $1 billion and has become the largest mobile launch of 2023. Let's look at the data and compare it with Dice Dreams.

MONOPOLY GO! also reached the milestone of 100 million installations on Sunday.

Revenue and Downloads

AppMagic recorded $446 million in revenue after taxes and commissions. In this case, the analytical service accounted for 3/4 of the revenue, around $745 million Gross. In terms of downloads, there are 94 million users.

At data.ai, revenue figures are slightly more accurate - $513 million after taxes and commissions, roughly $855 million Gross.

The revenue growth trend for the game has significantly slowed down. Most likely, the game has passed the stage of rapid growth. Scopely reports that the project currently earns $200 million in monthly revenue.

Build games faster using Mudstack - The ultimate Digital Asset Management tool for game studios

Stop wasting money and make artist collaboration easier than ever with

Cloud storage

Integrated review & feedback

Version control

Try for free here -mudstack.com

70% of the project's total revenue comes from the United States, 5% from the United Kingdom, and 3% each from Germany, Australia, Canada, and France.

Downloads are distributed somewhat differently. The U.S. accounts for 32% of the total volume, followed by Italy (7%), Malaysia (5%), Italy (5%), and the United Kingdom (5%).

Scopely actively supports the game through the UA. On average, there are 1.3 free users per paying user.

In-game Users

D1 Retention on both platforms is around 50%; D7 is 21-24% (slightly higher on Google Play); D30 is 12-15%. Analytical services often miss with these metrics, so they should be treated with skepticism.

Men and women in the game are equally split - 50% each.

Players over 45 years old make up 45% of the entire audience. The combination of mechanics and a familiar IP worked well.

What about Dice Dreams?

Monopoly GO! is often compared to Dice Dreams. Let's see how both projects fare in comparison.

The total revenue of Dice Dreams is currently at $160 million (after deducting taxes and store commissions) - roughly $266 million Gross. The game's monthly revenue (after deducting taxes and commissions) is currently at $11.7 million - the project is growing quite actively. However, in terms of revenue volume, Dice Dreams is not a competitor to Monopoly GO!

The revenue distribution by countries for Dice Dreams and Monopoly GO! is similar. The majority is in the U.S., followed by the UK, Canada, and European countries.

Over its lifetime (Dice Dreams was launched in mid-2020), the game has been downloaded 30 million times. The game has much lower acquisition volumes compared to Monopoly GO!, although the k-factor (the ratio between paying and organic users) is similar.

In Dice Dreams, the audience aged 25 to 44 dominates, accounting for almost 56%. It can be assumed that this demographic is less engaged and tends to spend less compared to older players.

The games are very similar to each other, and despite a significant time advantage, Dice Dreams is far behind the competitors. Several factors played a role:

A perfect synergy between IP and mechanics in Monopoly GO! Users know what to expect from the game even before launch, and it lives up to expectations.

Scopely's marketing expertise and the ability to operate with significantly larger budgets than Superplay.

Stronger monetization. Revenue per Download (RpD) for Monopoly GO! is already higher than for Dice Dreams, even though the project is not yet a year old. Perhaps this is due to the different audiences that the projects have managed to capture.

Product quality - especially the feel of the dice and rewards - is higher in Monopoly GO! However, this is very subjective.

GfK & GSD: The UK gaming market in October 2023 experienced a significant decline

GSD & GfK reports only on the actual sales figures obtained directly from partners. Major publishers, such as Nintendo, do not share information on the sales of digital copies, for example.

Software Sales

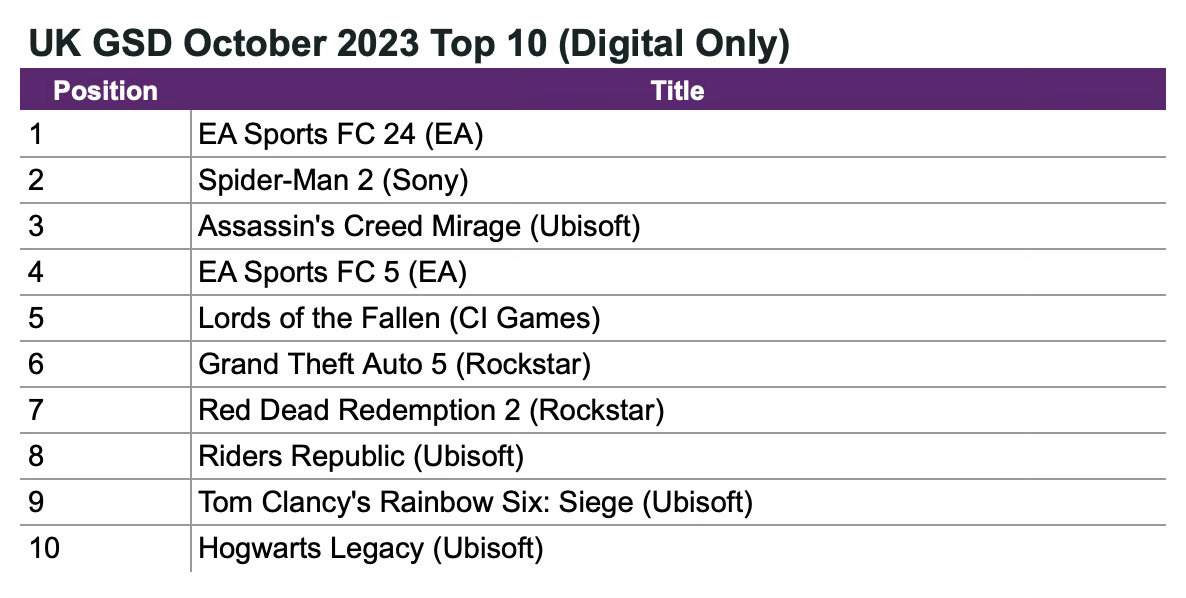

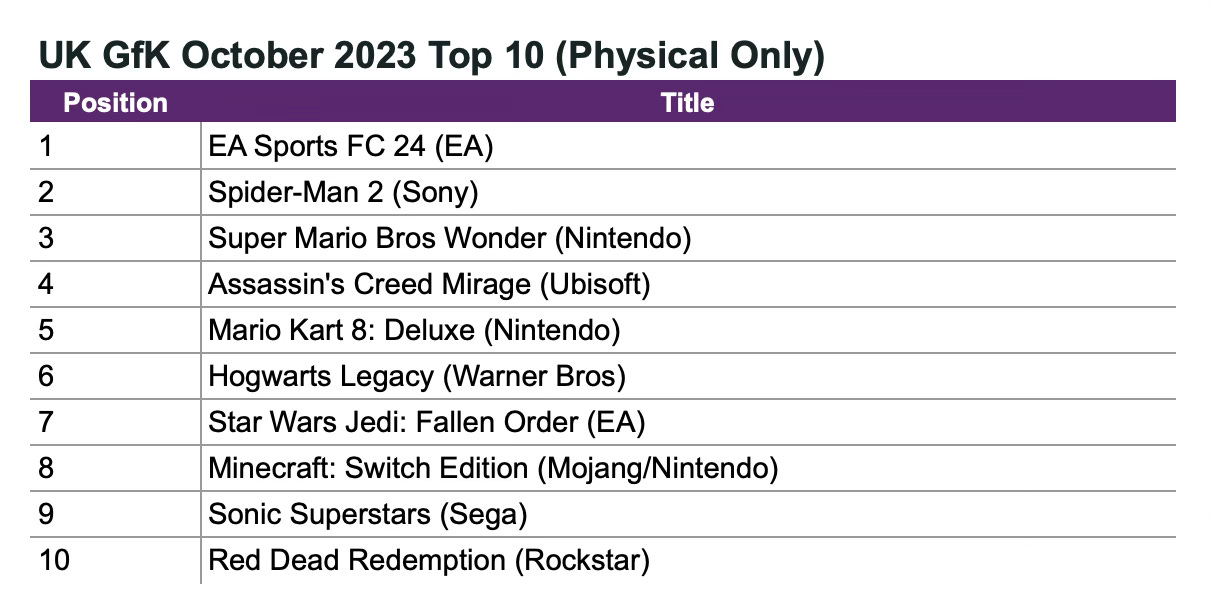

Digital sales in the UK fell by 24%, with 1.6 million digital copies sold. However, physical versions saw a slight increase of 8% to 1.08 million.

The sharp decline in sales is attributed to the fact that Call of Duty was released in October last year, while this year, a new installment in the series is set to launch in November.

EA Sports FC 24 launched 16% worse than FIFA 23.

Marvel’s Spider-Man 2 from Sony became the best-selling new game of the month. However, sales in the UK were 9% weaker than the first part but 94% better than Marvel’s Spider-Man: Miles Morales.

Compared to God of War Ragnarok, sales in the first two weeks of Marvel’s Spider-Man 2 were 2% higher. This is notable, considering that GoW: Ragnarok was available on PS4 and PS5.

Assassin’s Creed Mirage launched 58% worse than Assassin’s Creed Valhalla. First-month sales were nearly identical to the results of Assassin’s Creed Odyssey, released in 2018.

Hardware Sales

In October, 176 thousand gaming devices were sold in the UK, a 10% decrease from the previous month.

Build games faster using Mudstack - The ultimate Digital Asset Management tool for game studios

Stop wasting money and make artist collaboration easier than ever with

Cloud storage

Integrated review & feedback

Version control

Try for free here -mudstack.com

PS5 sales decreased by 4% compared to the previous month; 56% of all sales were attributed to the EA Sports FC 24 bundle.

Xbox Series S|X sales plummeted by 33%. The previous month saw an increase in console sales due to Starfield.

Nintendo Switch performed well. In October, console sales grew by 15% thanks to the release of Super Mario Bros. Wonder.

PlayStation 5 accounted for 51% of all console sales in the country over the last six months. Nintendo Switch had 25%, and Microsoft consoles had 23%.

In October, almost 584 thousand accessories were sold, a 15% decrease compared to the previous year.

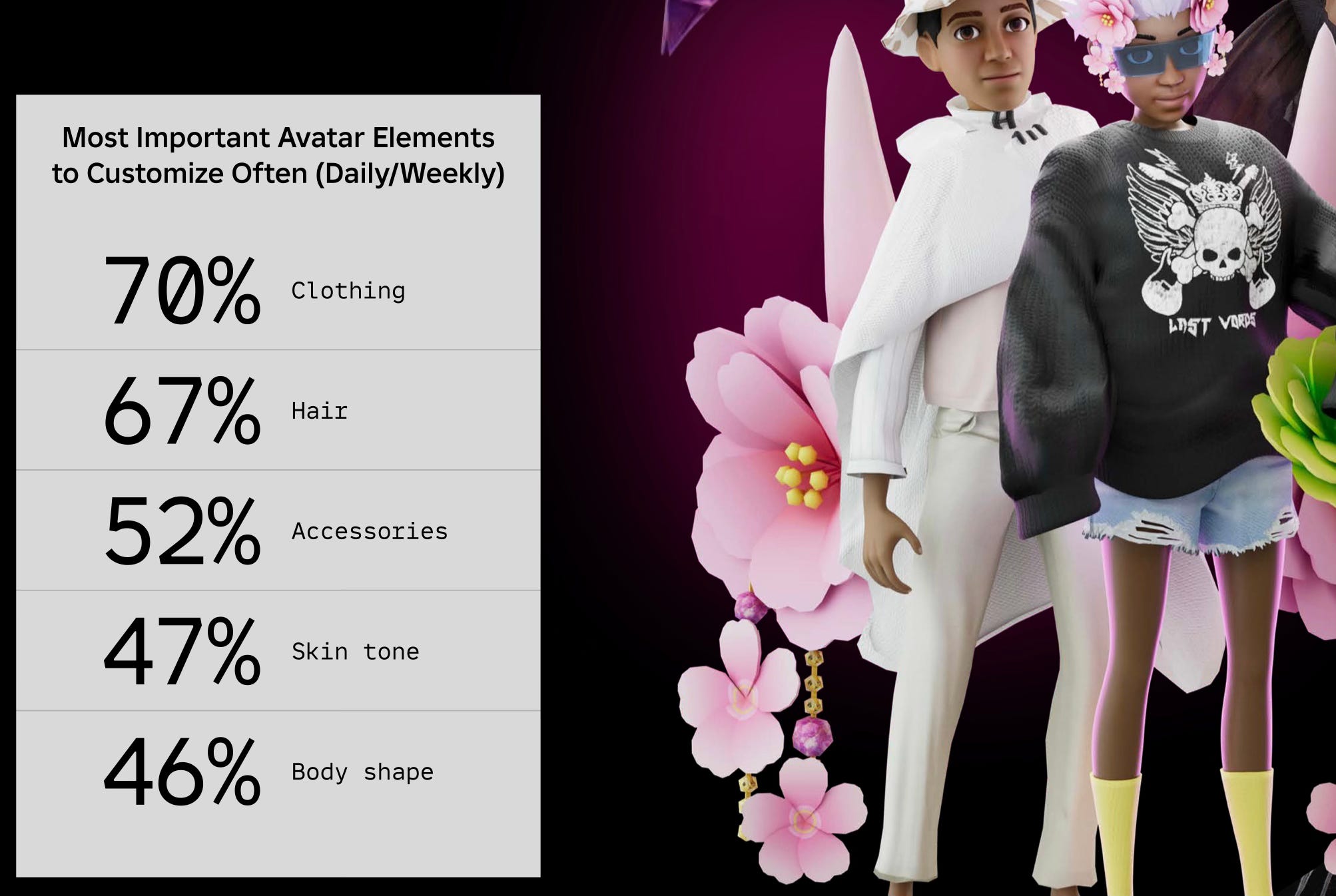

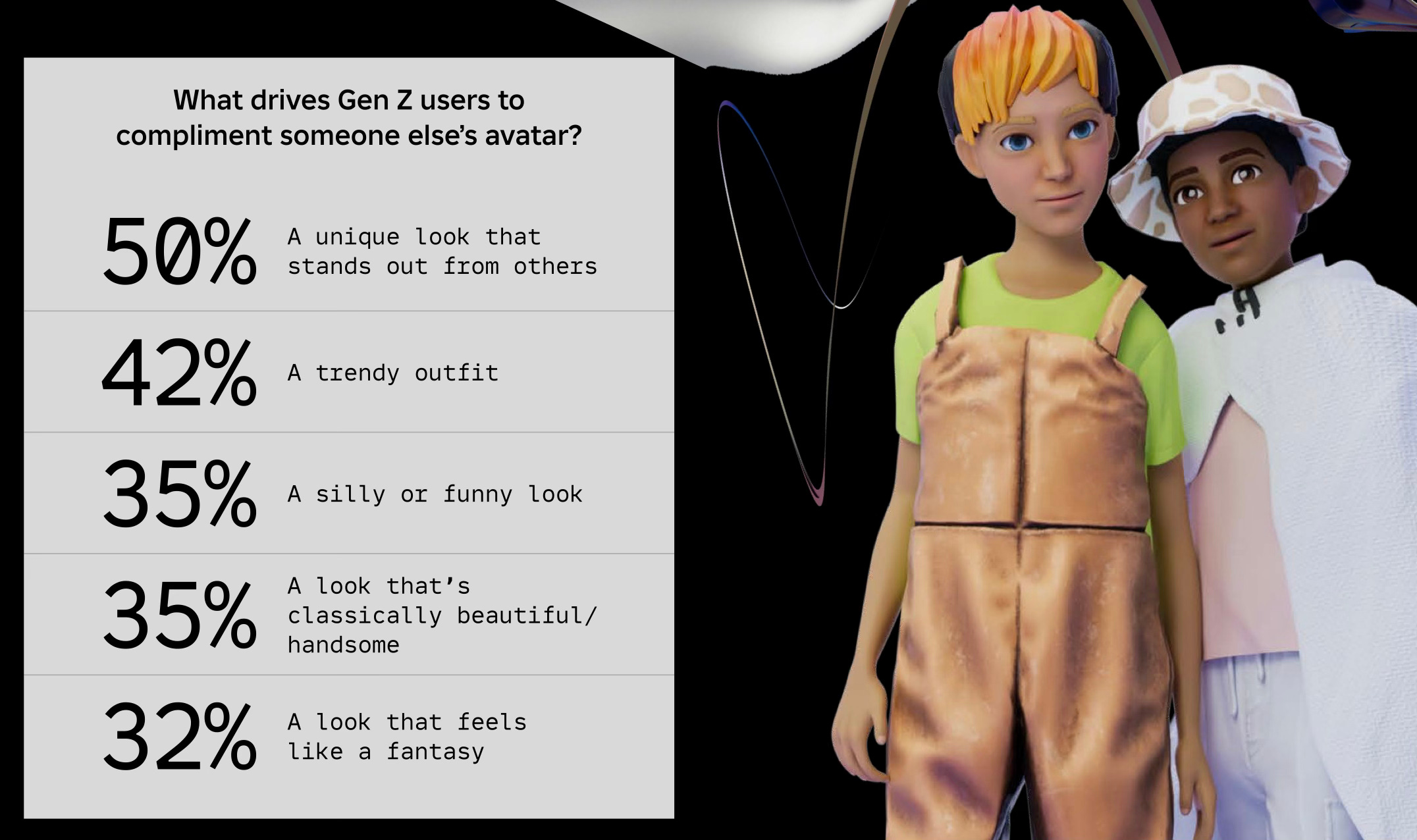

Roblox: Trends in Digital Fashion and Beauty in 2023

The report explores the behavior of Generation Z in the world of Roblox. Data on in-game behavior was collected from January 1st to September 30th. The survey involved 1545 individuals aged 14 to 26 living in the United States and the United Kingdom.

56% of Generation Z respondents stated that the appearance of their avatar is more important to them than their real-life appearance. Last year, this figure was 42%.

84% noted that digital fashion is something important to them. The majority believes that its importance has grown over the past year.

In 2023, users purchased 1.6 billion digital items for avatars. This is a 15% increase compared to the previous year. The number of avatar modifications increased by 38% to 165 billion times.

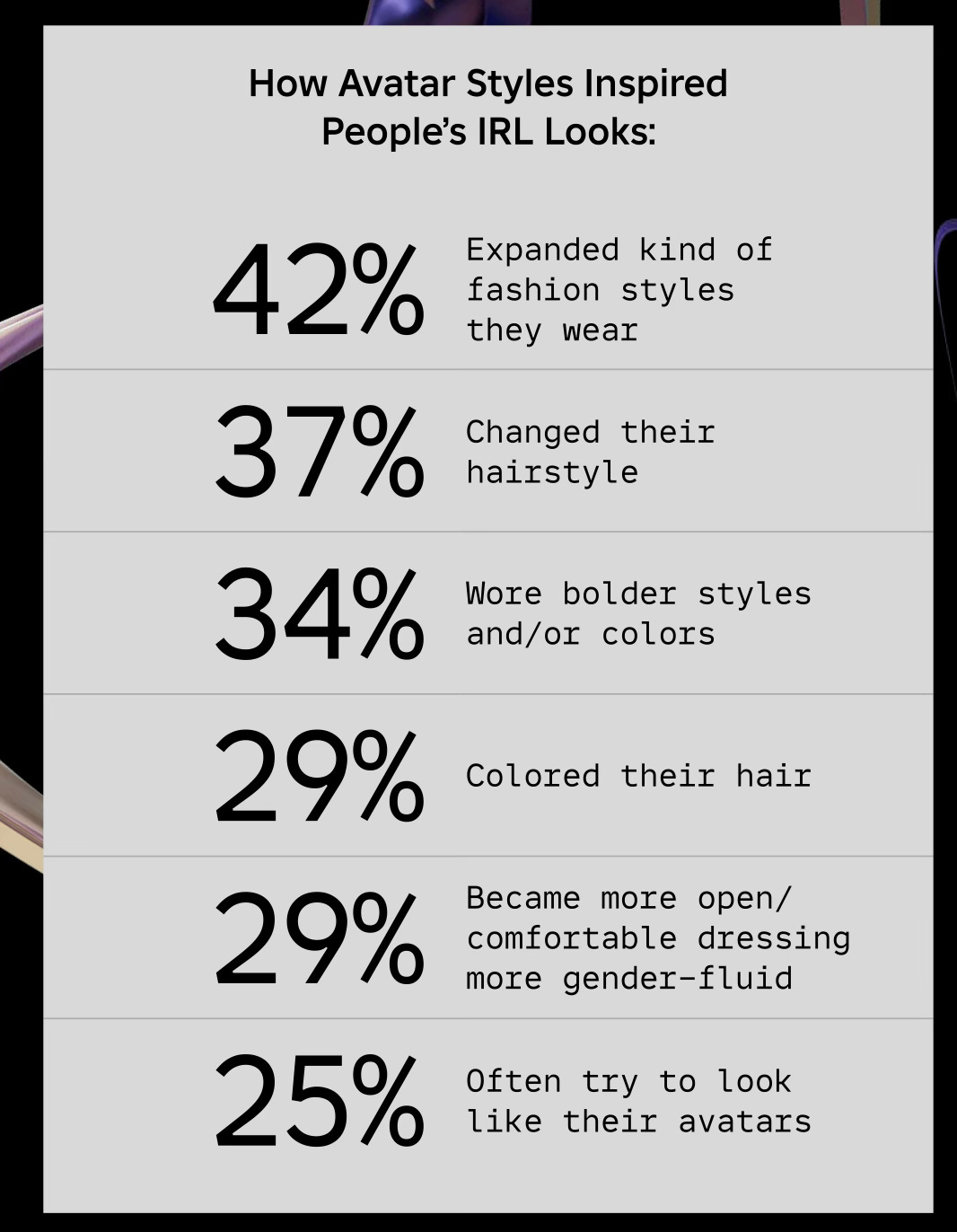

54% of Generation Z individuals mentioned that their real-life style is heavily inspired by the style of avatars in games.

84% of respondents stated that the likelihood of purchasing a branded item in real life increases after they have tried on that item on their digital avatar.

Build games faster using Mudstack - The ultimate Digital Asset Management tool for game studios

Stop wasting money and make artist collaboration easier than ever with

Cloud storage

Integrated review & feedback

Version control

Try for free here -mudstack.com

52% of Generation Z individuals are willing to spend up to $10 per month on digital fashion items; 19% are willing to spend up to $20, and 18% are willing to spend from $50 to $100 each month.

Users note that people in metaverses are less prone to judgment. Therefore, they strive to make their avatars unique and express themselves. People are less concerned about what others will think of them.

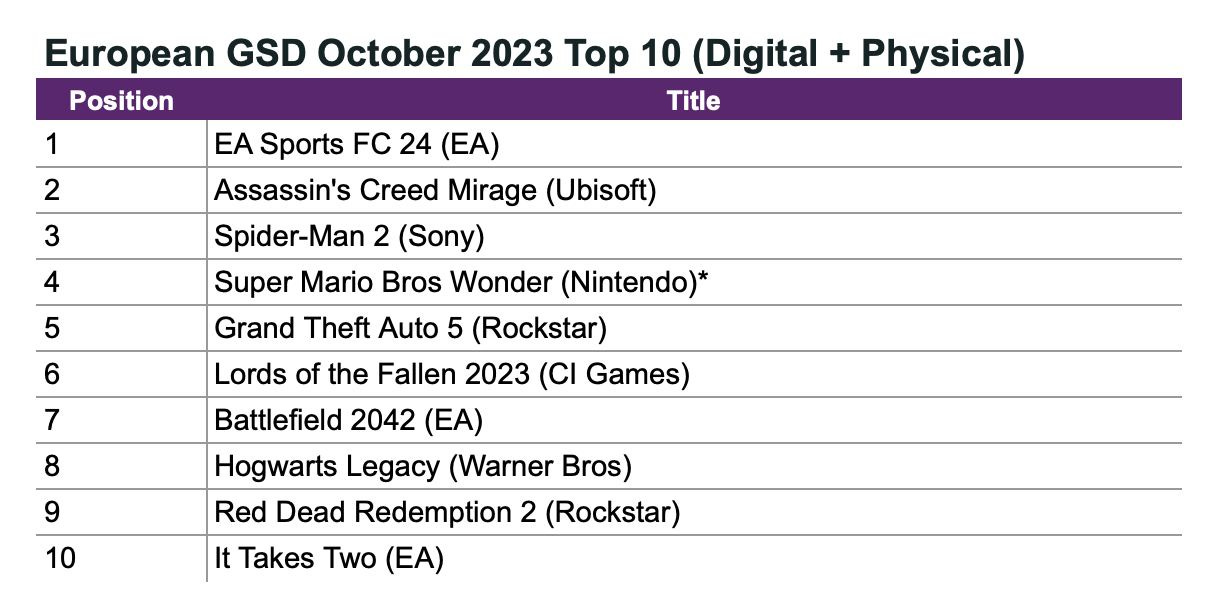

GSD: Game sales in Europe slightly decreased in October 2023

GSD reports only actual sales figures obtained directly from partners. Major publishers, for example, Nintendo, do not share information on digital copy sales.

Game Sales

By the end of October 2023, 10.21 million game copies were sold in Europe. This is 2.3% less than in October of the previous year. This is linked to the release of Call of Duty being moved to November this year.

EA Sports FC 24 became the best-selling game of the month by a significant margin. However, its sales are 10% lower than FIFA 23.

Assassin’s Creed Mirage managed to surpass Marvel’s Spider-Man 2 in sales, taking the second spot (though the game was on sale for 15 days longer). Meanwhile, sales of the new Assassin’s Creed installment are 49% worse than Assassin’s Creed Valhalla, but 22% better than AC: Odyssey, and 6% better than AC Origins.

Build games faster using Mudstack - The ultimate Digital Asset Management tool for game studios

Stop wasting money and make artist collaboration easier than ever with

Cloud storage

Integrated review & feedback

Version control

Try for free here -mudstack.com

In the first two weeks, Marvel’s Spider-Man 2 in Europe started 30% better than the first part and almost three times better than Marvel’s Spider-Man: Miles Morales.

Compared with God of War: Ragnarok, sales of Marvel’s Spider-Man 2 are 28% lower. But if you exclude copies for PS4, Marvel’s Spider-Man 2 sells 8% better after the first two weeks.

Hardware Sales

In total, 481 thousand consoles were sold in Europe in October. This is 16% more than in September.

PlayStation 5 - the best-selling console of October. Sales increased by 143% compared to the previous year and by 11% compared to the previous month.

Nintendo Switch - in second place; October sales dropped by 20% compared to the previous year. But they increased by 10% compared to September.

Xbox Series S|X is not doing well in Europe. Console sales in October plummeted by 52% compared to the previous year. And by 20% compared to September.

1.14 million accessories were sold in Europe in October. This is 3.6% less than last year.

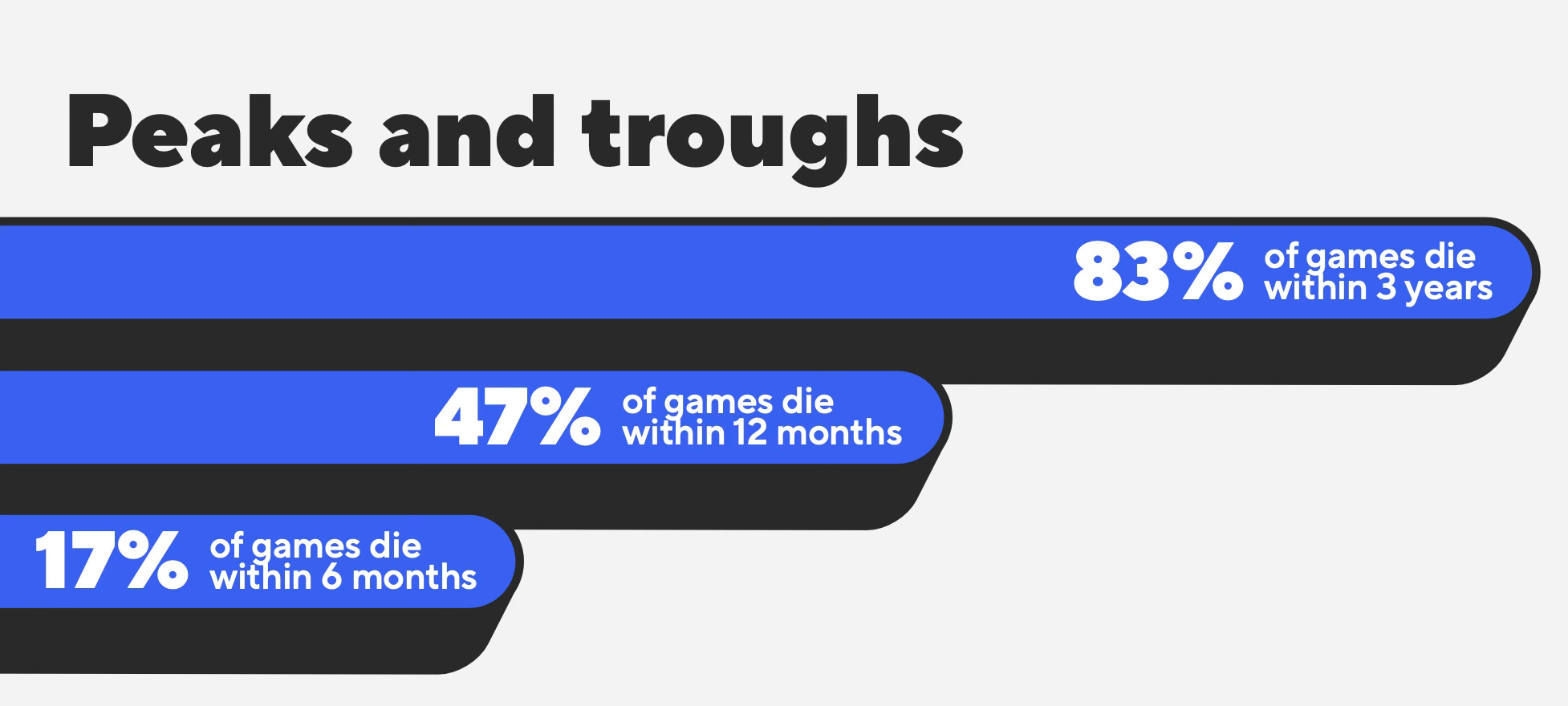

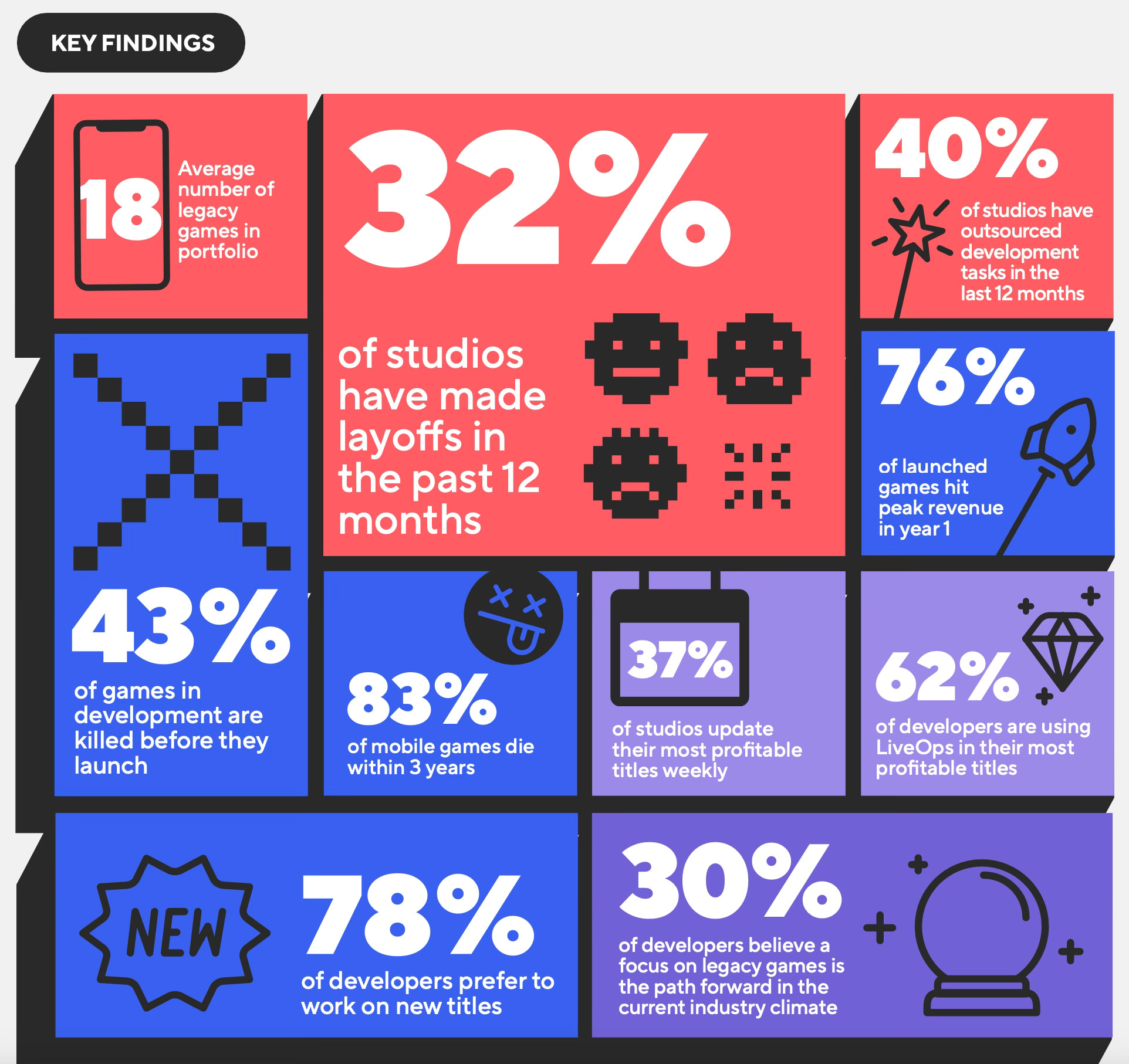

SuperScale: 83% of launched mobile games die within 3 years

The company published a report in which it surveyed 504 mobile developers from the USA and the UK. There is not much positivity in it.

Overall Picture

43% of games do not reach the release stage. 25% of those surveyed noted that the closure of an unreleased game significantly demotivates them.

83% of launched games close within 3 years. Only 5% are supported for more than 7 years. Most developers noted that they would prefer to work on new games.

In 76% of cases, the revenue peak occurs in the first year after release. In 4% - in the second.

38% of developers do not release regular updates for their games. This partially explains the above figures. Many developers simply do not know how to manage their games.

34% of developers believe that success lies in new releases; 30% are confident that success lies in managing current games. The remaining developers do not fully understand what to do in the current market situation.

Situation in Studios

32% of studios have conducted layoffs. Developers of puzzles and Match 3 games are the least affected.

The ultimate Digital Asset Management tool for game studios comes with artist-first version control

Let Mudstack handle the boring bits:

New versions are created automatically on save

A single view to see uncommitted changes

Commit and push with a single button

Don’t struggle with branching, locking and other developer workflows

Try for free here - mudstack.com

24% are on the verge of bankruptcy. Most of them work on hyper-casual projects.

29% have cut UA budgets.

40% of studios have become open to outsourcing development. For many, this is now a survival question.

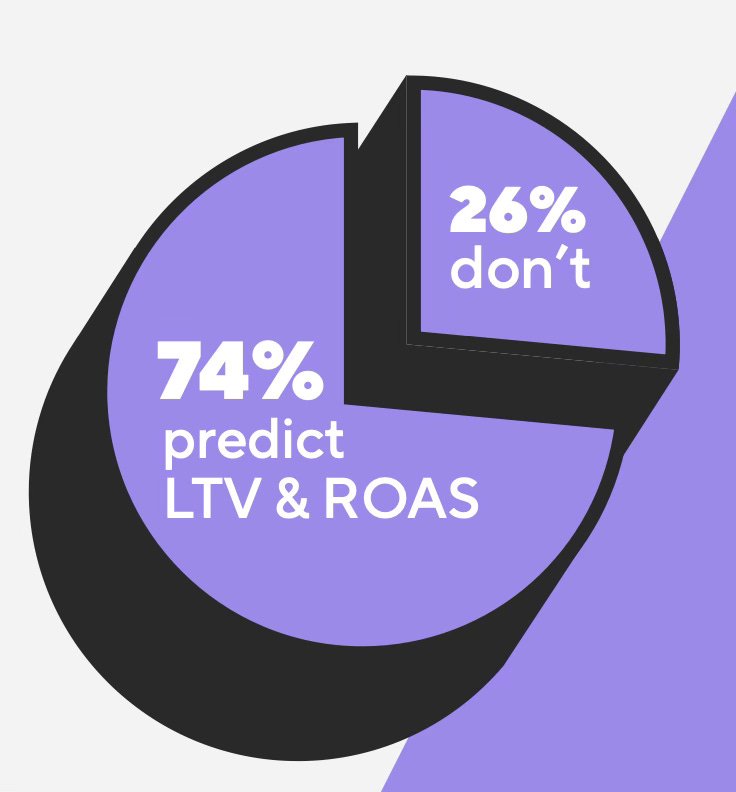

Monetization and UA

62% of developers actively use LiveOps in their major projects. 37% update games on a weekly basis; 48% on a monthly basis; 14% hold special events.

Google (54%); TikTok (39%); and Meta (31%) are the most successful advertising networks, according to developers.

26% of developers do not consider either LTV or ROAS (Return on Ad Spend). Another 32% only look at the horizon for six months. Only 5% try to predict what the ROAS will be beyond a year.

BFI UK: 51.9% of all British game developers work in companies owned by foreign entities

BFI UK studied the history of M&A transactions in the UK gaming market and assessed its impact on the industry. The figures are current as of the end of April 2023.

From 1993 to 2022, 118 transactions were completed, involving the acquisition of British studios. In 105 cases, the asset was a company, the majority of whose business is based in the UK.

49% of the transactions were carried out by companies headquartered in the USA; 15% were with HQs in China; 10% in Sweden.

The volume of transactions sharply increased from 2018 to 2021. During this period, 41 transactions occurred (39% of the number of "truly British" transactions).

In 2020 and 2021, the most money was spent (or earned - depending on the perspective), $2 billion and $2.7 billion, respectively. The largest deals were with Codemasters, Sumo Group, and Playdemic.

It’s time to kick Slack and Google Drive out of the game development pipeline.

Thanks for reading GameDev Reports — Sponsored by Mudstack! Subscribe for free to receive new posts and support my work.

Subscribed

Review and provide feedback directly in art files with Mudstack:

Request reviews by tagging other users directly in the file

Easily assign change requests and provide approvals on files

Mark up files with the built-in annotation tool

Try for free here - mudstack.com

The majority of buyers are actively involved in the gaming industry. Publishers accounted for 56% of all transactions.

Acquiring talented teams and strong IPs are the two main motivators for deals during this period, according to BFI UK.

Deals brought access to capital and marketing expertise. This is a positive outcome.

On the downside, studios lost autonomy (which may negatively impact innovation), and some revenue flowed out of the UK.

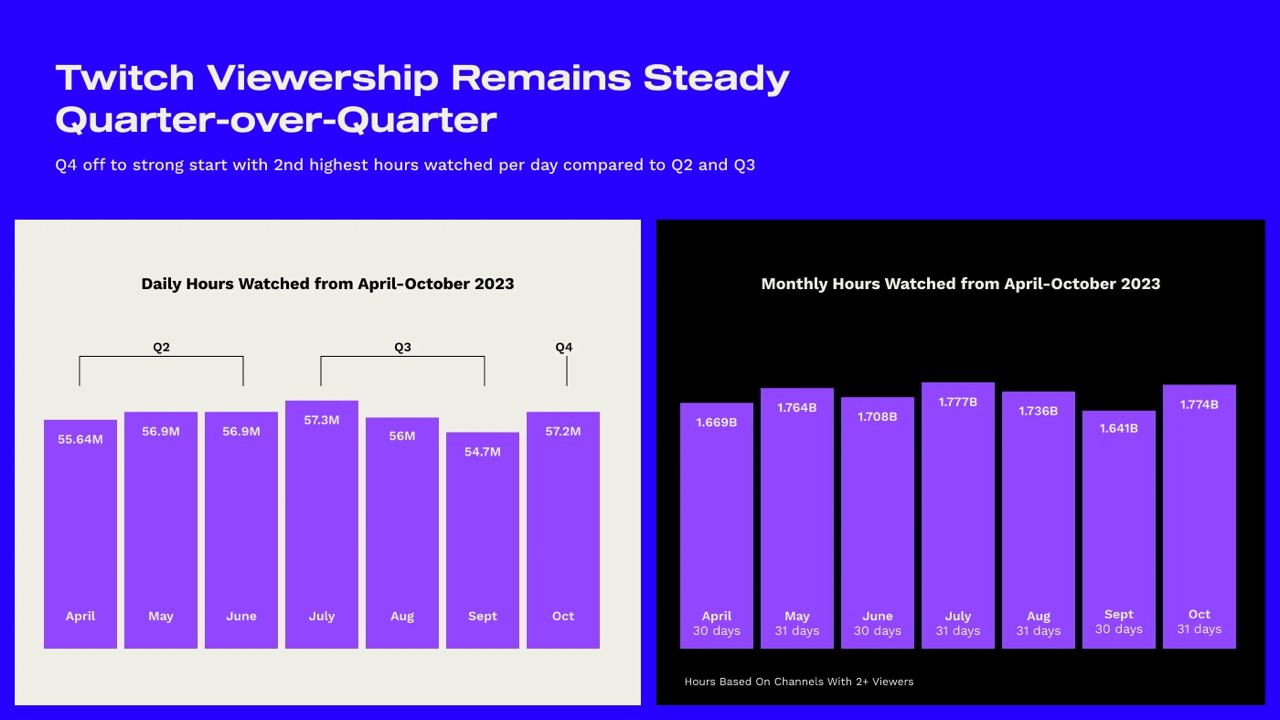

StreamElements & Rainmaker.gg: The State of the Streaming Market in September and October 2023

Twitch, in terms of hours watched, replicated its second-quarter results in the third quarter.

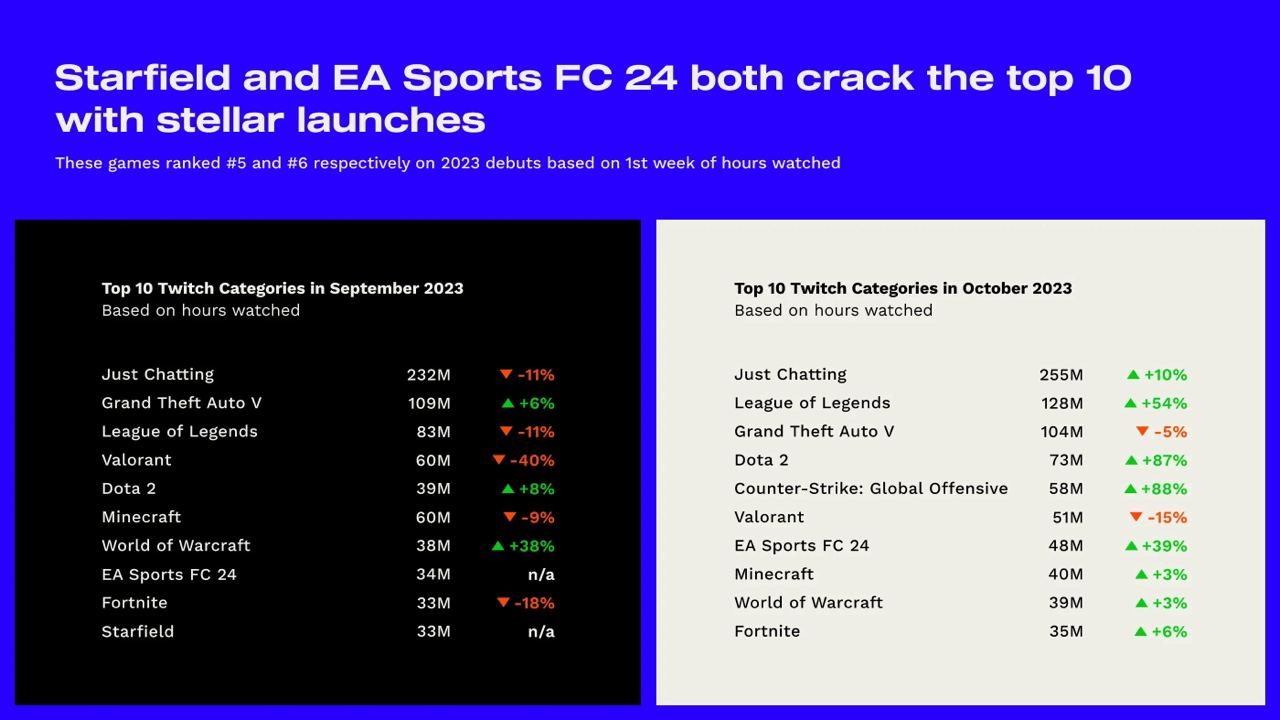

October became the second-highest month in terms of views this year, attributed to tournaments for League of Legends and DOTA 2, as well as the release of Counter-Strike 2.

Mudstack is the ultimate one-stop solution for digital artists

Easy collaboration on projects, no matter the location or timezone

Rapid iteration with the integrated review and feedback feature

Peace of mind knowing your files are secure

Try for free here - mudstack.com

EA Sports FC 24 and Starfield entered the top 10 in terms of hours watched in September and October.

Throughout 2023, despite the abundance of new releases, only 7 new projects made it into the top 10.

Traditional viewership leaders include League of Legends, Grand Theft Auto V, DOTA 2, and Valorant.