XSolla & Niko Partners: MENA-3 Market Research

Market, audience & monetization insights.

General Market Characteristics

According to Niko Partners, there are over 400 million Arabic speakers worldwide.

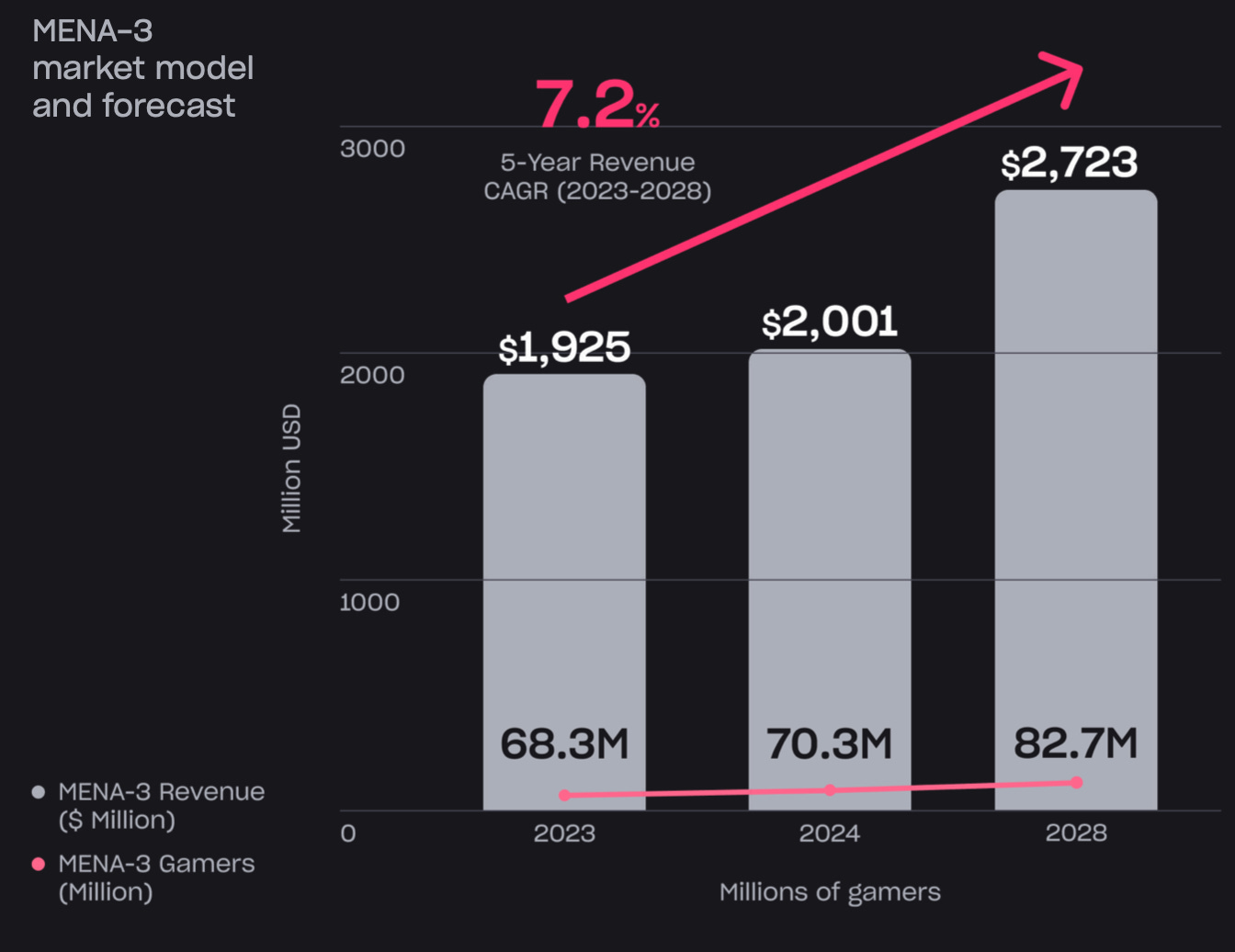

The study focuses on three key countries in the region (MENA-3) – UAE, Saudi Arabia, and Egypt. The total market size in 2024 is $2 billion (+4% YoY). By 2028, the market is expected to grow to $2.7 billion, with a CAGR of 7.2%.

❗️The authors note that these three markets represent different aspects of the Middle East: Saudi Arabia is the regional leader; Egypt has a large population but weak payment metrics; the UAE has a small population but strong payment metrics.

Saudi Arabia is the revenue leader in the MENA region. In 2022, it surpassed $1 billion, and by 2027, it will reach $1.5 billion.

The number of players in the MENA-3 countries will reach 82.7 million by 2028. In 2024, there were 70.3 million players. As of last year, only 51% of the total population in these three countries played games, leaving significant room for growth.

UAE has the highest annual ARPU among the three countries – $84.6. The lowest is in Egypt – $3.5.

Audience in the MENA-3 Region

Over 60% of players in the MENA-3 countries are aged 18 to 35. In reality, the share of young players is even higher, as the study did not survey those under 18.

Saudi Arabia and the UAE boast almost 100% internet penetration. Even in Egypt, internet coverage exceeds 70%.

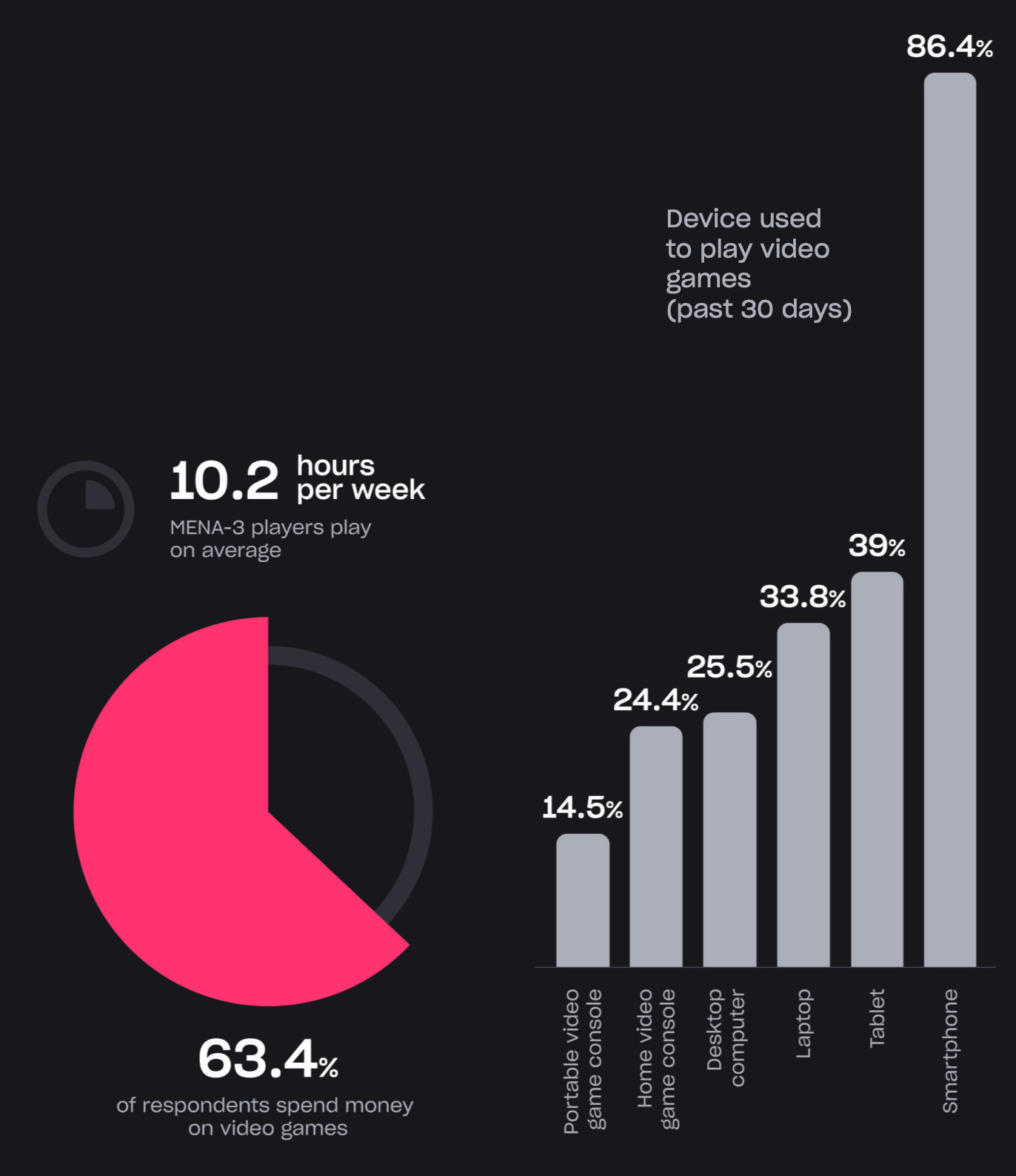

94% of players in MENA-3 countries play on mobile devices. 49% on PC, 34% on consoles. This is a major difference from other emerging markets, like India, where only 6-7% play on PC and consoles.

The share of female gamers in the MENA-3 countries is growing rapidly. It increased from 32% in 2022 to 38% in 2025.

The average monthly salary of a gamer in the MENA-3 countries is $2,166. Excluding Egypt, it’s $3,137. As disposable income grows, so will in-game spending.

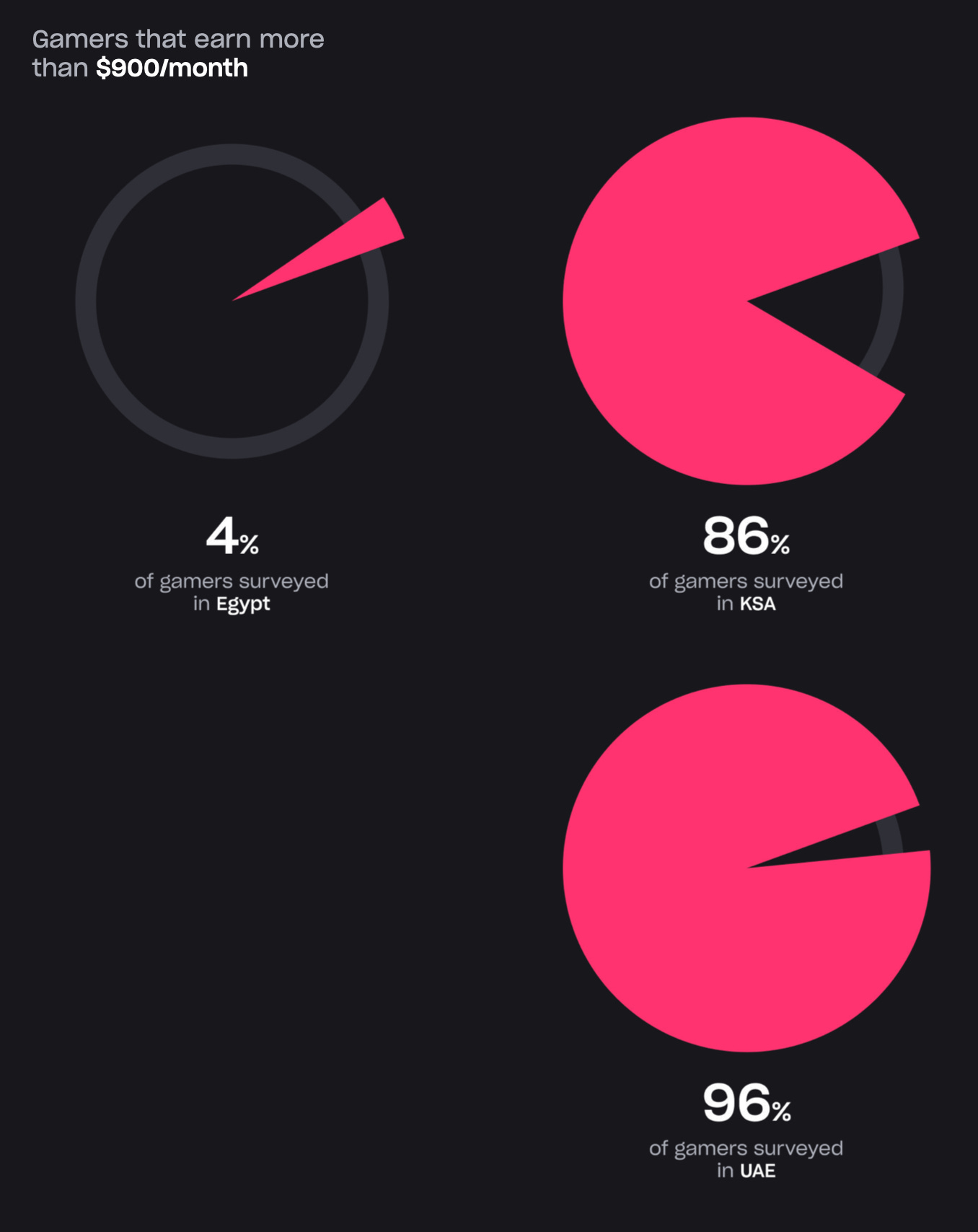

Only 4% of surveyed gamers in Egypt earn more than $900 per month. In Saudi Arabia, it’s 86%; in the UAE, 96%. Premium games and subscriptions perform best in the UAE and Saudi Arabia.

61% of surveyed players in the MENA-3 countries play on two or more platforms. 16% play on mobile, PC, and consoles.

56.5% of multi-device players regularly switch between platforms.

Players in the MENA-3 countries spend an average of 10.2 hours per week gaming. In Egypt, 31% of all players spend more than 13.25 hours per week gaming.

Consider subscribing to the GameDev Reports Premium tier to support the newsletter. Get access to the list of curated articles & archive of Gaming Reports that I’ve been collecting since 2020.

63.4% of all respondents have spent money on games.

Monetization of Players in MENA-3

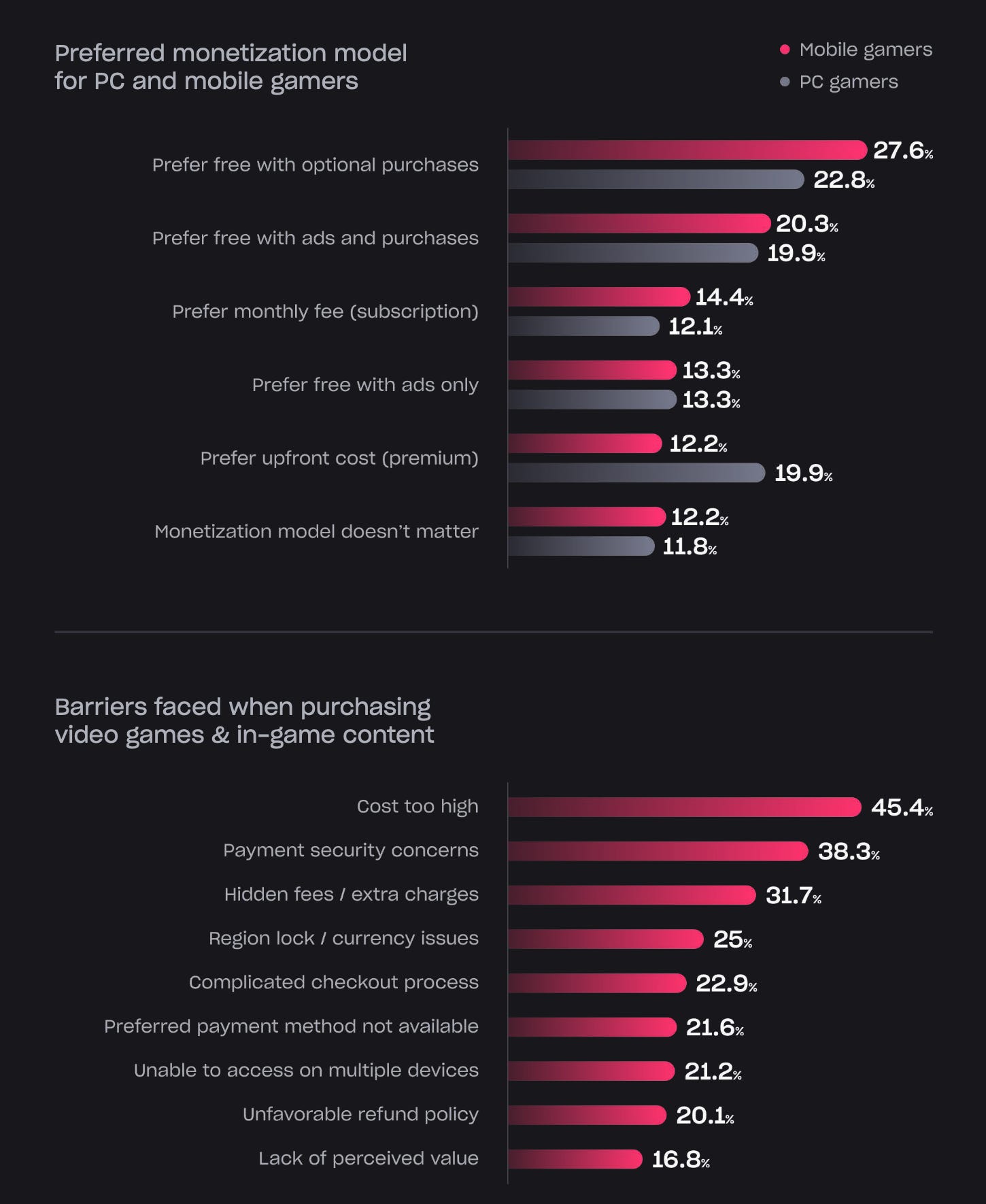

61% of mobile gamers in the selected countries and 56% of PC gamers prefer the F2P model with in-app purchases.

Saudi Arabia leads in premium games (26% of players prefer such games).

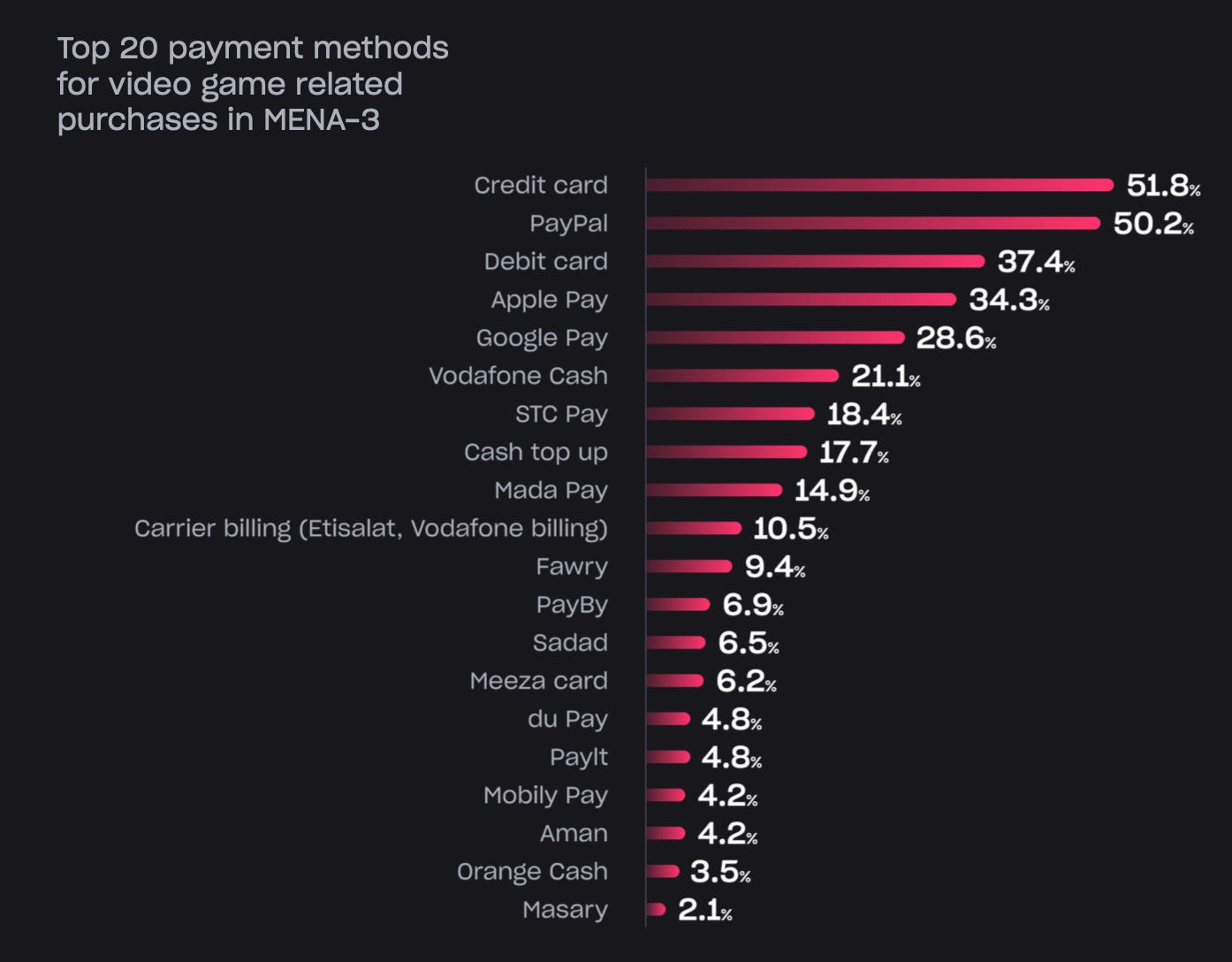

67% of the MENA region’s population lacks proper access to banking products or rarely uses them. For example, in Egypt, credit card penetration is only 2.8%. Even in Saudi Arabia and the UAE, the rates are low – 25.4% and 26.8%, respectively.

In Saudi Arabia, the Mada payment service is popular (93% penetration). PayPal (52%) is more popular than credit cards in Saudi Arabia. Only in the UAE does the payment infrastructure resemble that of the West.

53% of players in the MENA-3 countries have made purchases on game websites, bypassing standard payment methods. Egypt has the highest share, over 60%.

Reasons for such purchases vary. For some, it’s faster (40.7%); some get access to familiar payment methods (37%); some buy outside standard stores for extra rewards (35.9%) or discounts (34%).

Overall, the main motivation for purchases outside usual app stores in the MENA-3 countries is financial. 40% said they would buy items in webshops if prices were lower. Bonuses for purchases are also a key motivator.

When people in the MENA-3 region were asked what would make them start spending on games, 43.9% mentioned low prices. It’s difficult to determine how much discounting would actually benefit.